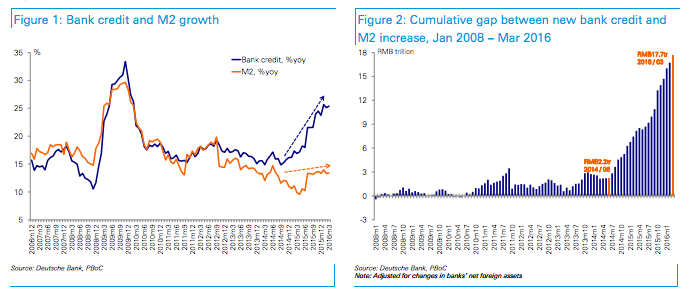

Bank credit growth and M2 growth used to track each other quite well in China. It is intuitive. In a simple world where banks’ main business is to channel deposits into loans, the two should correlate well. But this is no longer the case. Bank credit growth has picked up from 15% yoy in late 2014 to 25.4% by March 2016 (Figure 1). M2 growth moved up since mid 2015 after policy easing happened, but only to 13.5% by March. The gap has widened from 7.8% in June 2015 to 12% in March 2016.

Another way to look at this gap is in terms of RMB rather than yoy growth rate. Between Jul 2014 and Mar 2016, total bank credit in China increased by RMB41tr. After adjustment for the RMB1.7tr decline in banks’ total net foreign assets, it was RMB15.5tr higher than the RMB23.7tr increase of M2 during the same period. The gap reached an astonishing RMB15.5tr in cumulative term over this period. It is equivalent to 23% of China’s 2015 GDP (Figure 2).

The result of these clashing factors is exactly what we observe: On the one hand, the banking sector has been pushing out new lending aggressively, partly reflecting the government’s will to support growth, and partly driven by the needs to leverage up to offset narrowed profit margin and maintain returns. On the other side, many borrowers are reluctant to invest the credit from banks into the real economy. Rather, they try to seek financial investment opportunities. With real returns coming down and the amount of financial assets chasing those returns going up, it should not be surprising if they turn to financial leverage to boost returns.

As FTAlphaville observes from Anne Stevenson-Yang:

This means the same slow grind we have seen since mid-2014: lower incomes, lower spending, sagging incomes, and an acceleration of capital flight. This pattern can continue until there is a significant depreciation of the currency. At that point, re-rating of assets will make China’s market de facto irrelevant to the investment world.

This may be bad news for the intellectually exhausted, but there is unlikely to be a single moment when China falls apart.

In short, China’s glide slope to lower growth is it’s hard landing.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.