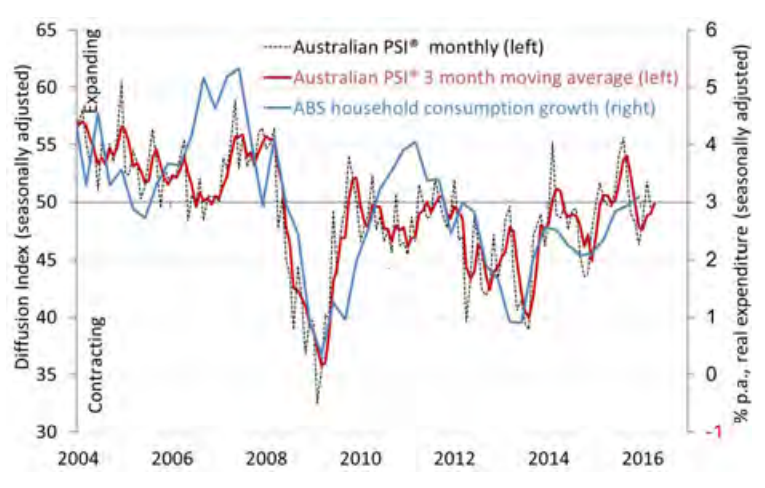

The Australian Industry Group Australian Performance of Services Index (Australian PSI® ) increased slightly by 0.2 points to 49.7 points in April, indicating continuing stable conditions for the services sector (results above 50 points indicate expansion, with higher numbers indicating a stronger rate of expansion).

• Of the five of activity sub-indexes in the Australian PSI® , only new orders (51.9 points) and deliveries (51.5 points) expanded in April. Sales remained largely stable (49.7 points) while stocks deteriorated further (45.9 points) and employment fell again (48.1 points) in April. The expansion in new orders and deliveries is a positive indicator for conditions ahead, yet employment conditions remain weak.

• Five of the nine services sub-sectors in the Australian PSI® were stable or expanded in April (three month moving averages). The strongest subsectors in April were finance & insurance (60.7 points) and health & community services (54.2 points). Retail trade improved from last month’s contraction and expanded (52.8 points) while transport & storage services improved from contraction to stable (49.3 points), as did property and business services (49.5 points). Wholesale trade (45.4 points), communication services (45.7 points) and personal and recreational services (45.5 points) went from expansion to contraction in April.

• The Australian PSI® results for April suggest a balancing of growth toward business and goods distribution services, with generally stable conditions in household services. The results also indicate that the large services sector is still facing very mixed conditions.

• The input costs (62.5 points) and wages (57.8 points) sub-indexes of the Australian PSI® remained in expansion in April while selling prices stabilised from contraction (49.9 points). This indicates that margin pressures continue for services businesses.

• Respondents also noted softer economic conditions (particularly in some regional areas), uncertainty around the upcoming Federal budget and election, growth due to infrastructure programs in eastern states and some adverse effects from the strengthening dollar.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.