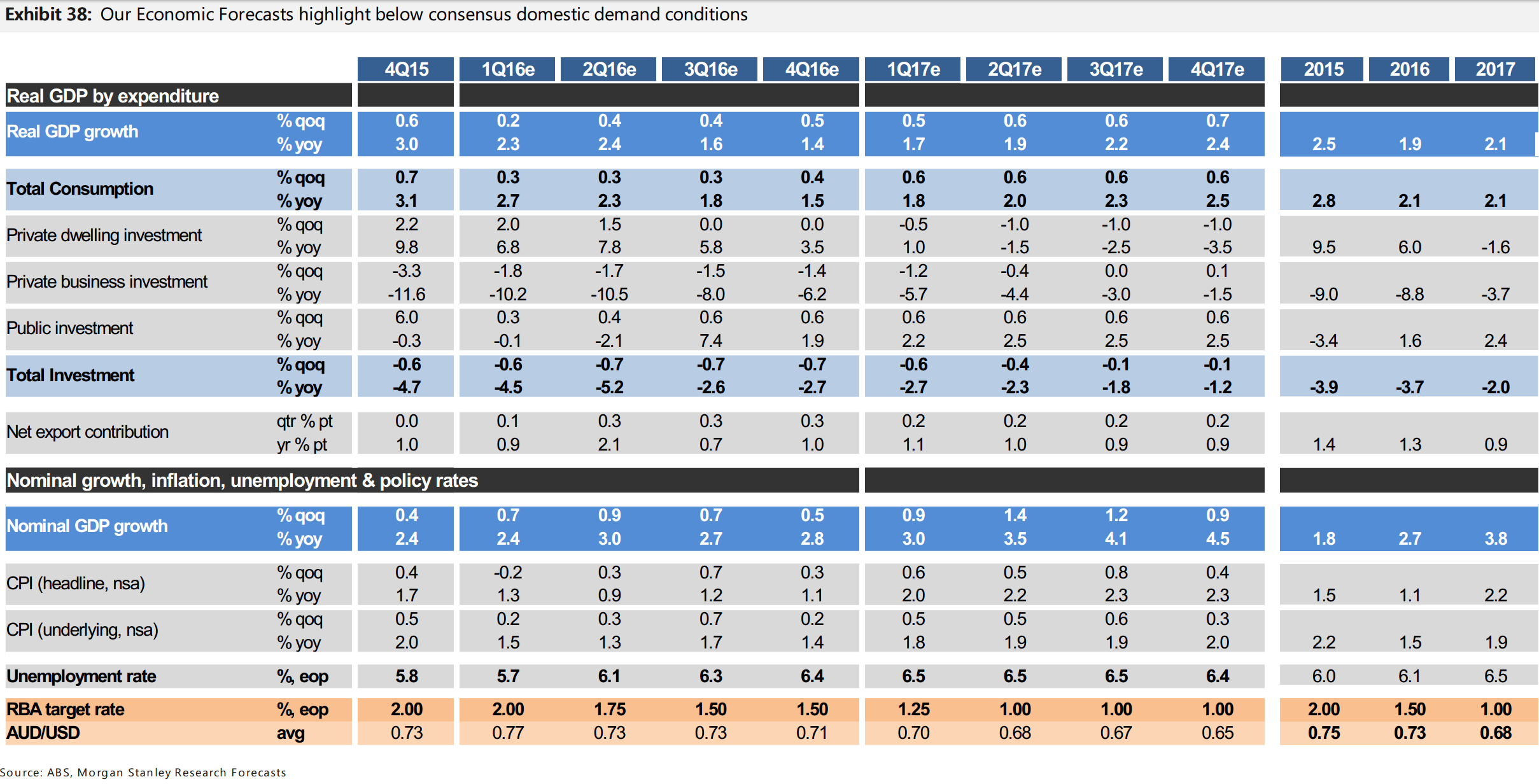

With our new forecast of a 1% trough in the official cash rate in 1H17, we believe the implications for key domestic and rate sensitives ectors are on balance negative, given the diminishing positive impact from monetary policy and the deteriorating backdrop that is driving the move.

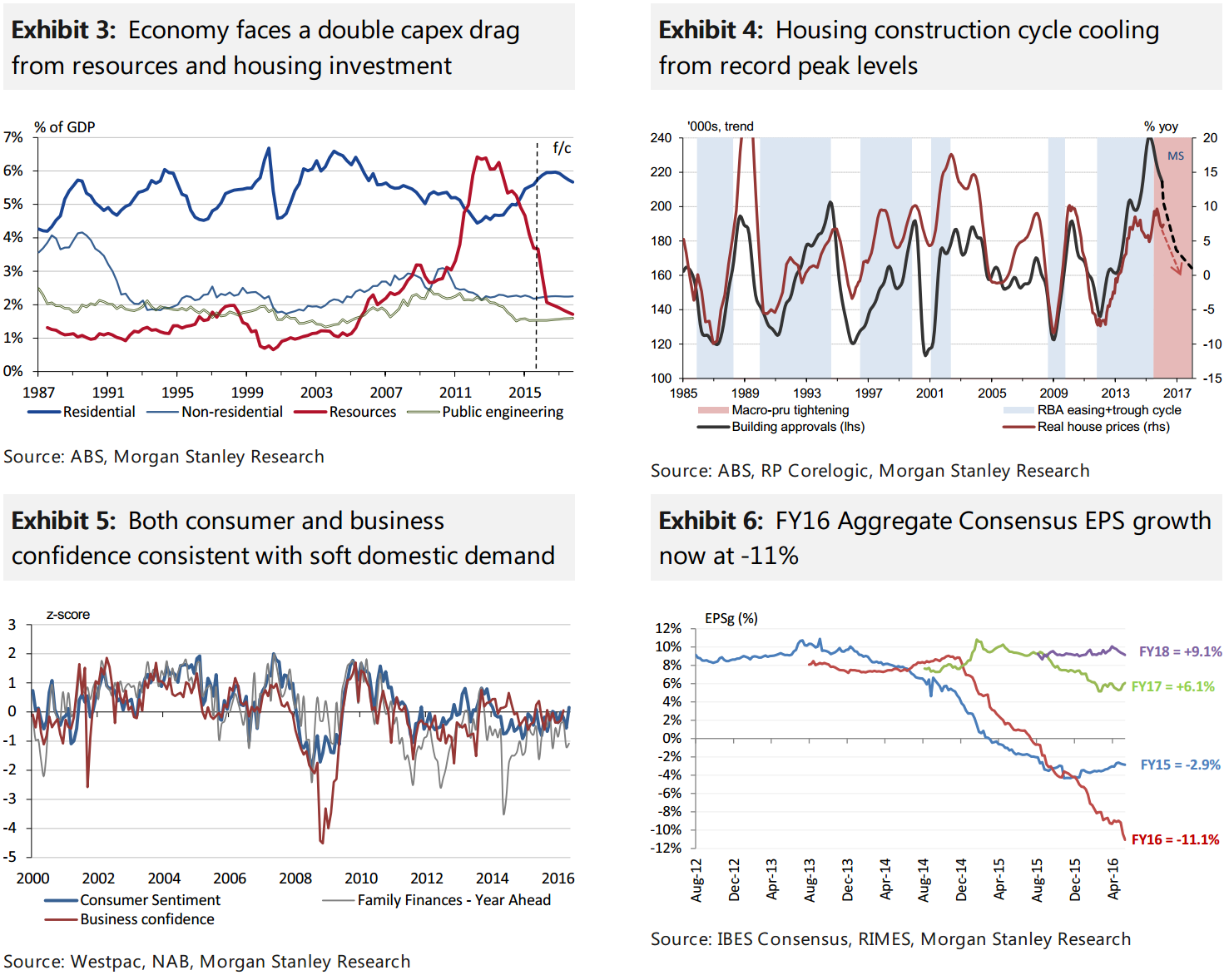

Cash rate trough to 1%: We now forecast the RBA to cut the cash rate to a trough of 1.00% this cycle. Continued conservatism around infrastructure stimulus combined with housing activity peaking, the economy is left dependent on a weaker AUD (Morgan Stanley forecasts AUD/USD 0.65 by 4Q17). Risks to net services export growth and an even more disinflationary outlook support our call for a deeper easing cycle.

More a tool of containment: This depth of trough cash ratein prior cycles would have been seen as super-stimulatory. However, like other DMs, Australia has passed the inflection point of outsized positive impacts from easier monetary policy. The next move lower in rates, in our view, will have an objective of risk containment, and will be unlikely to turn market earnings momentum in the short term.

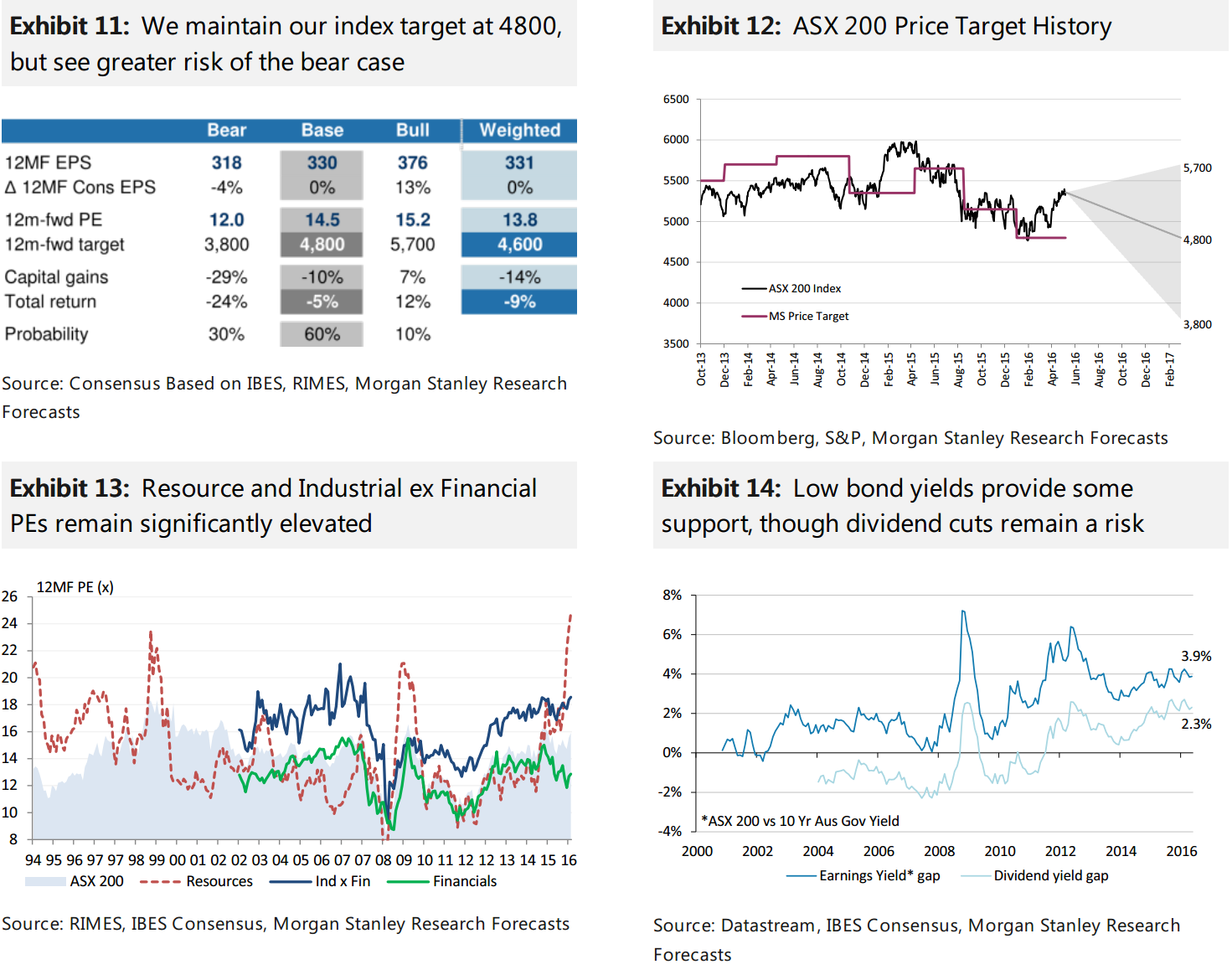

ASX 200 – de-rating buffered but no rally: We retain our 12-month Index target of 4,800 (10% downside), which implies a market multiple of 14.5x– a little above the long-run average. We acknowledge a buffer to de-rating risks whilst cash rates continue to fall. That said, should the move in rates fail to turn the earnings cycle– pricing of recession risk, further falls in EPS, and ultimately a de-rating lead us to cut our bear case scenario value 5%, to 3,800 (-29%).

Key sectors affected: We look at the key domestic-facing sectors in Banks, Financial Services, Consumer, Builders and Defensives. For Domestic Cyclicals, we believe the causal links driving the lower policy rates in most cases outweigh the stimulatory benefits typically seen and paid for in prior easing cycles. For Defensives, there will be continued valuation support to remain expensive, so we look for relative value where possible.The one compelling theme that should endure is the Global Earners trade, where we retain near double-benchmark exposure.

Model portfolio: We retain key themes of lower beta, active tracking error and a size bias away from the mega caps. The one pervasive theme that captures both the lower domestic growth expectations and also anticipated AUD weakness is Foreign Earners. Here we add WFD and COH at the expense of LLC and VCX .We also add GNC (funded out of cash), broaden our EW in Resources to include EVN,and take TLS to Neutral (from UW).

Exactly right. Stall speed, add any kind of external shock and it’s recession. The allocation to offshore earners is good but I still think selling the rallies is the way to go given I expect an external shock that’ll smack stocks. Then buy ’em again when it comes.

Well done to MS for figuring it out first. The spirit of Gerard Minack lives!

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.