More remarkably, Macquarie has the audacity to allege that “the AFR’s claims about Macquarie having a privileged position as a ‘government-backed bank’…are incorrect”. “Macquarie has not received, and does not receive ‘government backing’,” a spokesperson said.

The RBA has given Macquarie a $5 billion emergency line of credit to draw down on during a crisis when nobody else will lend to it at a subsidised cost of just 0.4 per cent above the cash rate.

From Chris Joye today:

That must rank as one of the most misleading statements I have ever heard from a bank.

Macquarie’s $43 billion in customer deposits are explicitly government-guaranteed for free. The taxpayer-owned Reserve Bank of Australia has given Macquarie a $5 billion emergency line of credit to draw down on during a crisis when nobody else will lend to it at a subsidised cost of just 0.4 per cent above the cash rate.

Rating agencies lift Macquarie Bank’s run-of-the-mill “BBB+” credit rating two notches higher to a strong “A”, which lowers its cost of funding, on the assumption Macquarie (and the four majors) are “too big to fail” and will receive “extraordinary government support” if something goes wrong. Finally, Macquarie raised more government-guaranteed deposits and bonds than any other Australian bank in the early stages of the crisis – some $25 billion of taxpayer-insured money by April 2009.

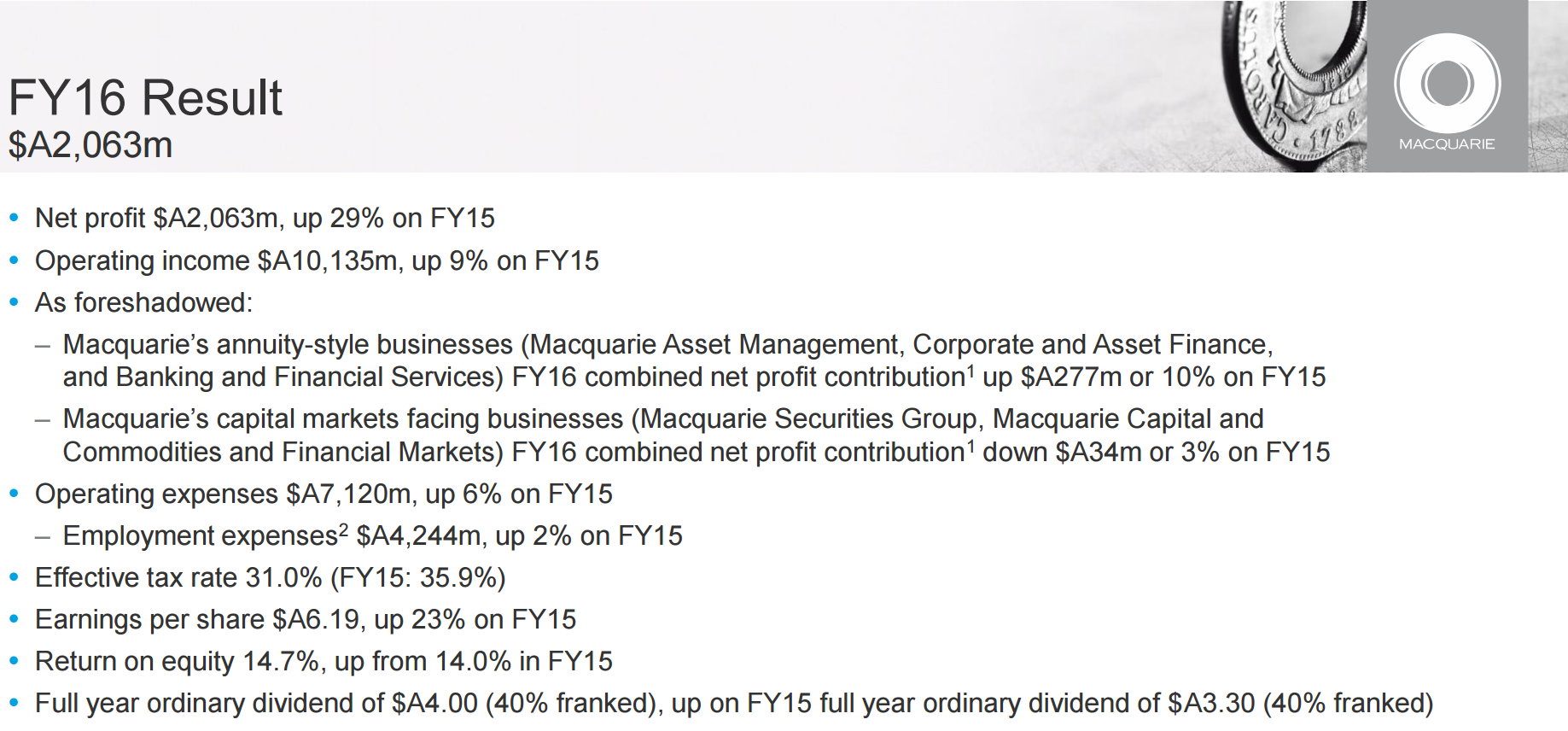

Turning to today’s profit announcement let’s see what Macquarie has been doing with this tax-payer largess:

Advertisement

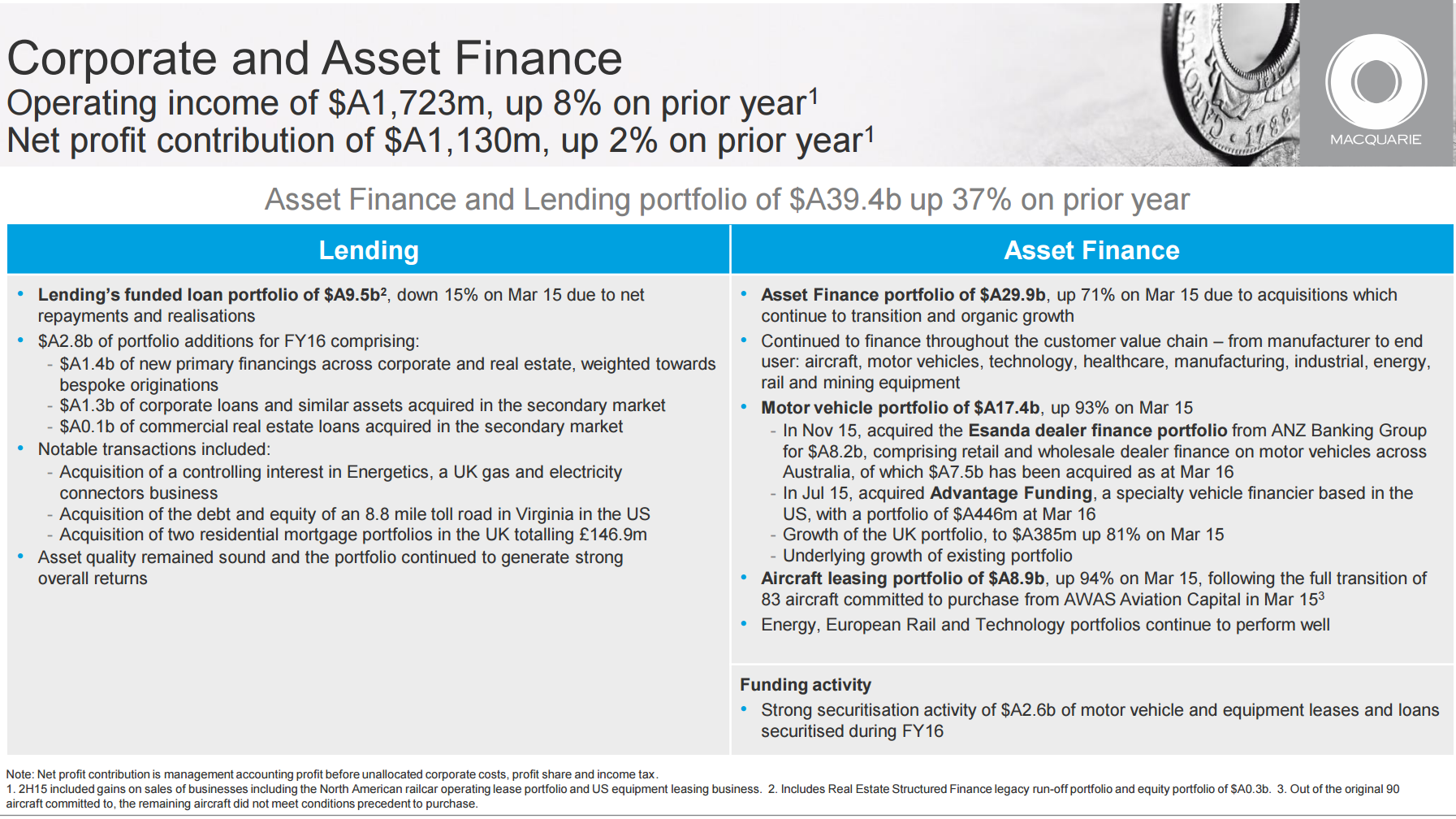

And of that, here is the CAF segment within which is buried Mr Brazil’s little hedge fund:

Advertisement

MQG’s junk trading business is believed to generate about half the profit of CAF, its second largest division. You can’t say that that’s a quarter of net profits because there are some complications with accounting for its head office but it’s big and large enough to drive up its Pillar III loan arrears (which MQG did not update today) to 5x as large as those of the other majors.

MQG is down today perhaps in part owing to its flattening profit trajectory but also surely owing to rising regulatory risk.