From the AFR on the weekend:

Saul Eslake, one of the nation’s most respected economists, said he saw no compelling need for a budget day interest rate cut after this week’s shock inflation data, saying the Reserve Bank should maintain its ability to react against two main threats facing the economy.

The first is a hard economic landing in China that significantly curbs national income and further erodes the Commonwealth’s budget position. The second is the danger of what would be the first credit rating downgrade in almost three decades.

…”If Australia’s credit rating gets downgraded – and at least one agency has warned of that – and that led to the [commercial] banks’ credit rating being downgraded and paying more for wholesale funding, the RBA might well want to offset that by cutting their cash rate.”

“…the inflation data does not in any way indicate there is a greater need to cut rates,” he said. “It doesn’t tell you anything about the state of demand.

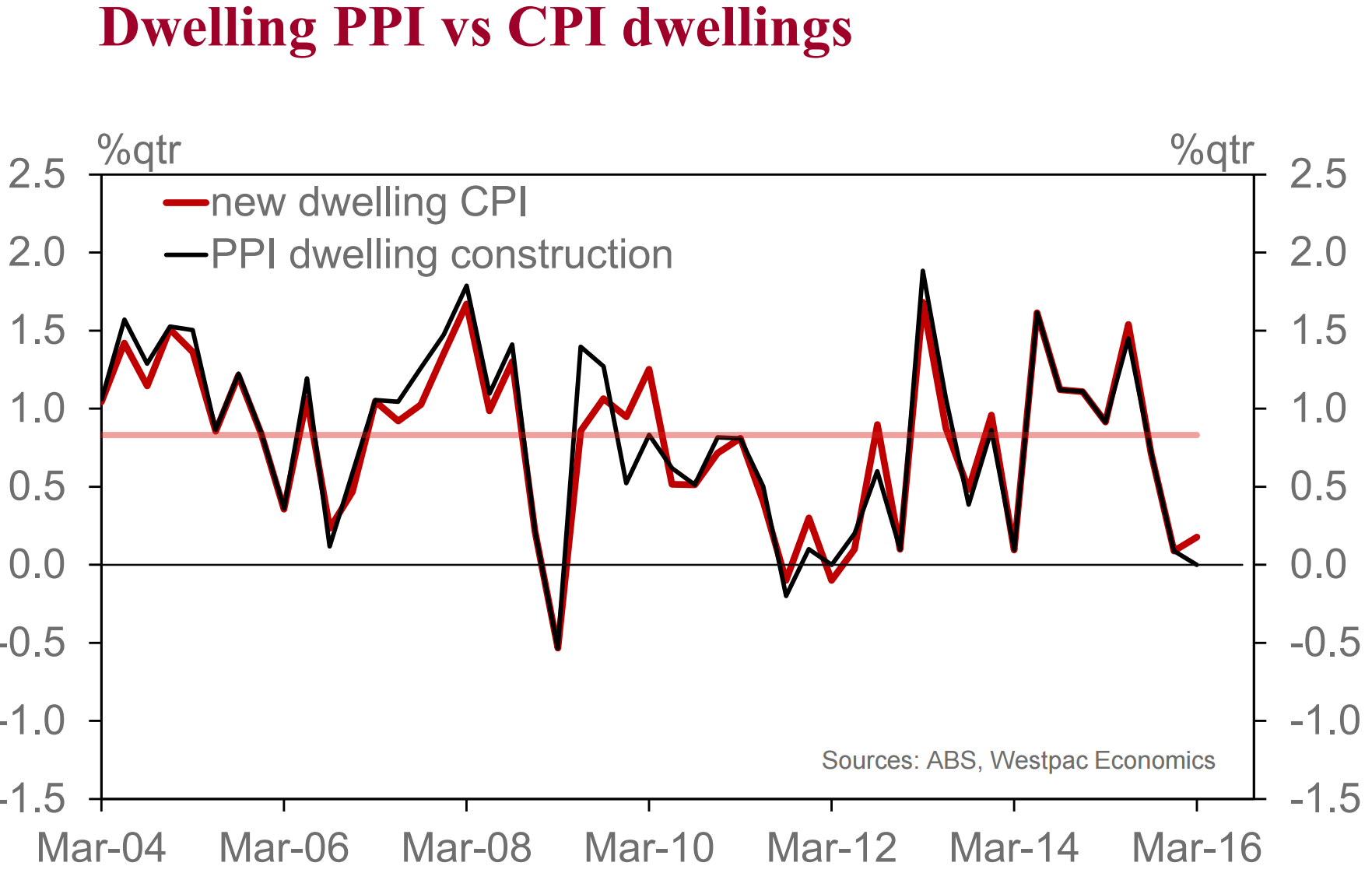

Can’t say I agree. The inflation data is telling us something about demand, it’s not just about oil and veggies. Check out the building PPI during a residential construction boom (charts from Westpac):

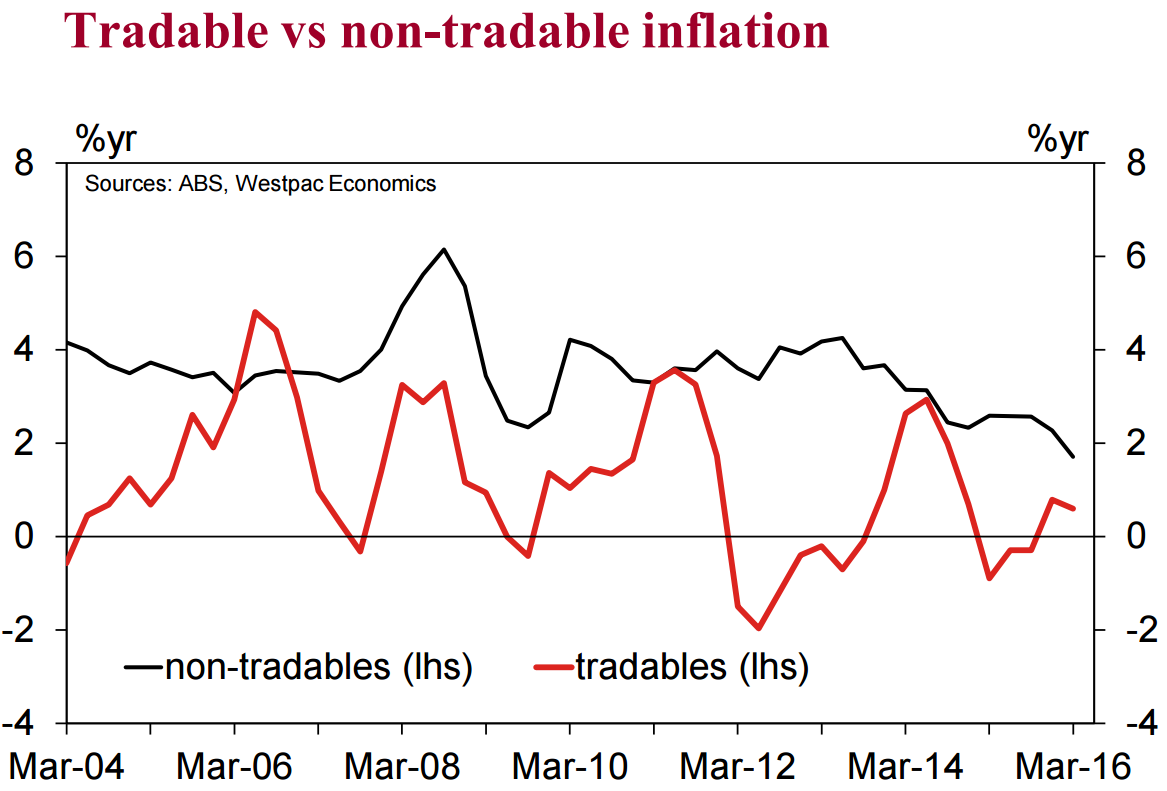

That’s weak! Wider non-tradable inflation (which is basically the services monster) is also falling fast and is already deeper than the GFC:

I agree that there is a risk that the weak inflation data is a bogus signal, which is why I see the RBA holding off next week and waiting for further confirmation of economic weakness before acting, but what does not make much sense is allowing the economy to weaken now in defense of being able to support it later.

Moreover, the sovereign downgrade is widely thought likely to cost banks 10-20bps on funding costs, though, as I’ve said before, if it occurs mid-crisis it will be more. So Saul is right that something needs to be kept in reserve for that but 50bps in cuts ought to be enough. And by the way, Saul, China is already in a “hard landing”, more or less.

The basic problem with this thinking is that it continues the “bubble management” approach of supporting household debt when we ought to be getting out in front of the crisis by deliberately adjusting the economy towards tradable-based growth via a lower dollar. You can’t fatten that pig on market day unless you want the reckoning to be all the greater when it comes.

As the RBA’s magazine empties out you can expect a lot more hand-wringing over every bullet kept in reserve.