From Westpac:

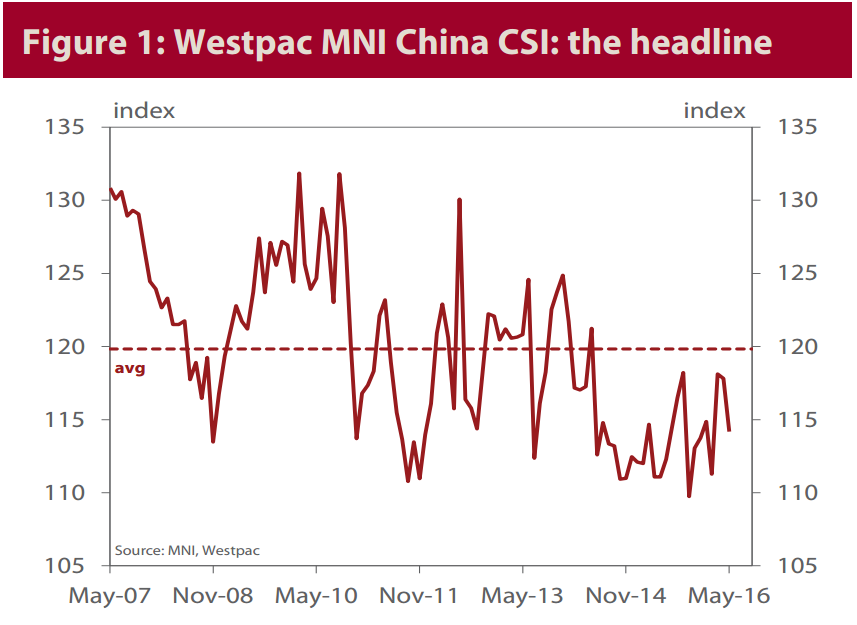

The Westpac MNI China Consumer Sentiment Indicator fell 3.1% to 114.2 in May from 117.8 in April.

Chinese consumers appear less convinced about prospects for improvement in the year ahead with family finances still under pressure and the hoped for business recovery continuing to disappoint.

All components deteriorated in May. Assessments of ‘family finances vs a year ago’ posted the biggest fall, down 5.5%, but that was closely followed by ‘time to buy a major household item’, down 4.2%. Consumers’ near term expectations were pared back: ‘business conditions, next 12mths’ down 3.0% and ‘family finances next 12mths’ down 2.8%. The medium term outlook was more firmly anchored with ‘business conditions, next 5yrs’ down just 0.5%. Despite the broad based pull-back, all components remain above their levels of a year ago.

Consumer assessments of current business conditions were slightly softer, the ‘business conditions vs a year ago’ index down 0.2% (note that this index is not part of the headline composite but is highly correlated with the PMIs & official IP). The pull-back in near term expectations likely reflects continued disappointment around the recovery in business conditions which has been only very tentative to date.

The employment indicator improved 1.7% in May and has now posted a solid 7.7% rally since its low in February. Despite this, sentiment around jobs remains considerably more down beat than the rest of the survey with the indicator still 7.8% below its long run average.

Household expectations for inflation fell 0.6% in May while expectations for interest rates declined 1.7%.

Consumer attitudes towards real estate softened but remained positive overall. The housing composite fell 1.3% but is still 1.7% above its long run average. Assessments of ‘time to buy’ fell 3.8% but were coming from a 2yr high. Likewise house price expectations declined 2.2% but are still comfortably above the long run average. Views around savings showed the proportion nominating real estate as the ‘wisest place for savings’ was down slightly but a higher proportion nominated house purchase as the primary ‘motivation for saving’.

Purchasing plans and perceived buying conditions were also softer in May. Expenditure plans for shopping and spending on entertainment remained at above average levels but expected spend on ‘dining out’ fell to a below average level. Assessed buying conditions were down across the board – readings for IT products and communications devices were notably firmer and reads for major durable items were weaker.

While the consumer mood overall is still more positive than late last year, and deeper concerns about employment prospects have eased a touch, the pull-back in sentiment in May marks a significant loss of confidence. That and the more ‘risk averse’ tone apparent across much of the survey detail suggests Chinese consumers are taking a more cautious approach to spending and financial decisions.