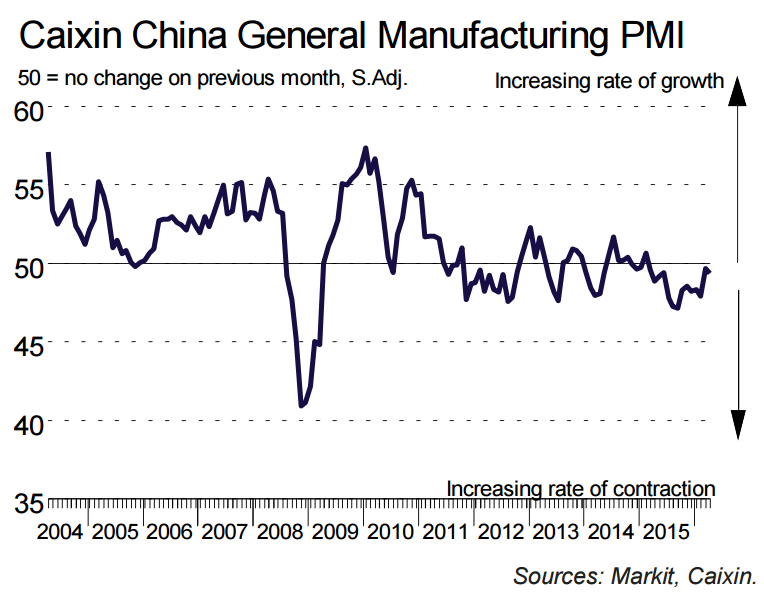

Some recovery we’ve got going in China! The Caixin PMI is out and bupbow:

Operating conditions across China’s manufacturing sector continued to deteriorate in April, albeit marginally. Output was little-changed from the previous month, as total new orders stagnated and new export work fell for the fifth month in a row. Relatively weak market conditions and muted client demand contributed to a further solid decline in staff numbers. Companies also displayed cautious inventory policies in April, with stocks of finished goods and inputs both falling at faster rates. Prices data indicated that inflationary pressures intensified across the sector in April, with input costs rising at the quickest pace since January 2013, which in turn underpinned the quickest rise in output charges since October 2011. Adjusted for seasonal factors, the Purchasing Managers’ Index™ (PMI™) – a composite indicator designed to provide a single-figure snapshot of operating conditions in the manufacturing economy – remained below the neutral 50.0 value at 49.4 in April. This was down from a reading of 49.7 in March, and pointed to a further deterioration in the health of the sector, albeit marginal. Operating conditions have now worsened in each of the past 14 months.

After a slight increase in March, production at Chinese manufacturers was broadly unchanged in April. According to panellists, relatively weak market conditions and softer client demand led firms to be cautious towards their production schedules. Furthermore, new order books stagnated in April, following a slight expansion in the previous month. Latest data indicated that weaker foreign demand continued to weigh on overall new orders, with new export work falling for the fifth month running. Subdued market conditions led some firms to implement down-sizing policies in April, while others chose not to replace voluntary leavers. As a result, overall employment declined again, with the rate of job shedding only fractionally slower than February’s post-global financial crisis record. Meanwhile, backlogs of work rose only slightly. Stagnant new orders contributed to a renewed fall in purchasing activity in April. Lower buying activity and relatively muted client demand underpinned the fastest fall in stocks of purchases for 12 months. Meanwhile, cautious inventory policies were also evident with regard to stocks of finished goods, which declined at the quickest pace since the start of 2009. Despite reduced input buying, supplier performance deteriorated in April and at the fastest rate since May 2011. Some respondents noted that stock shortages at vendors had lengthened lead times. Average input costs faced by Chinese goods producers rose for the second month running in April. Moreover, the rate of inflation accelerated to the fastest since January 2013. A number of monitored firms mentioned that greater raw material costs had put upward pressure on cost burdens. Companies generally passed on increased input prices in the form of higher charges for their goods. The rate of charge inflation also quickened since March, and was the most marked since October 2011.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.