The Aussie bond market is afire following yesterday’s RBA cut as yields rampage towards record lows across the curve:

The two year has actually broken to its lowest since May last year and is only 8bps from all time lows. They’re almost certainly going to get taken out in my view as doves take flight in the market. Deutsche is typical:

Today’s decision is about how the RBA views its mandate

By easing – and in particular citing “very subdued growth in labour costs and very low cost pressures elsewhere in the world, [which] point to a lower outlook for inflation than previously forecast” – the RBA has decided to take a narrower interpretation of the “two to three per cent, on average, over the cycle” inflation target than we had anticipated. That has a number of implications for the likely future course of monetary policy, given the long lags between changes in monetary policy and changes in unit labour costs (the major determinant of inflation). Assuming, of course, that monetary policy in Australia can even impact local labour costs.

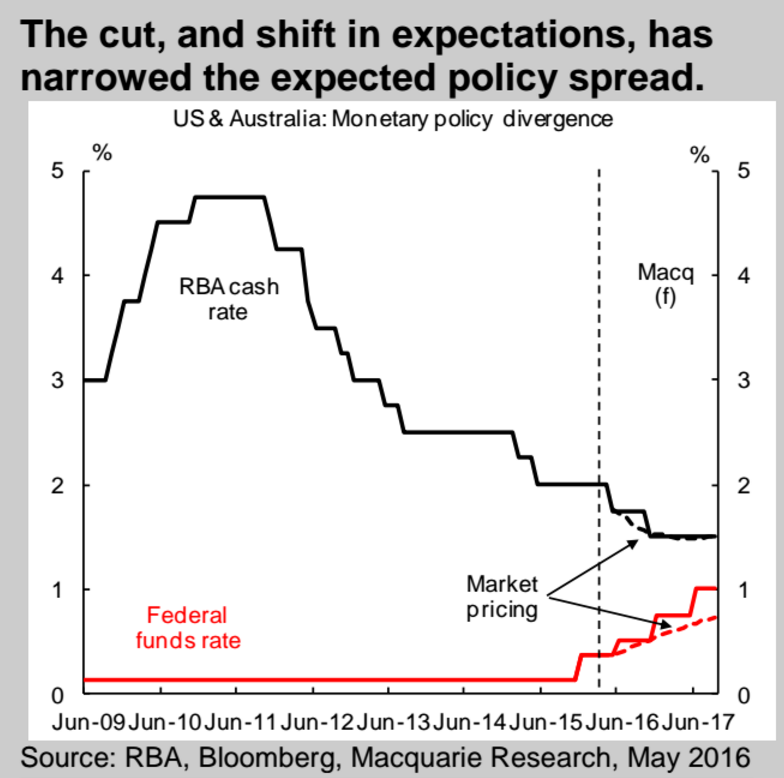

The exchange rate will need to ‘lift’ inflation, hence 1.25% cash by mid-2017

Specifically, the RBA will need to rely quite heavily on a lower exchange rate to lift inflation. Given it takes a relatively large exchange rate move to have a relatively small impact on inflation, returning inflation to the band over the next few years is likely to ultimately require the market to conclude the cash rate is heading toward (indeed below) Fed Funds. We don’t expect the RBA to be of this view at the moment, but given the 50bps of easing in 2015 had no noticeable impact in lifting wages growth or consumer price inflation it is hard to see a cumulative 50bps of easing this time as ‘doing the job’. As a result we expect the RBA to ease by another 50bps (after today’s 25bp), bringing the cash rate to 1.25% on a one year horizon as inflation ‘fails to lift’. We will nominate 25bps in August 2016, then a pause, followed by 25bps in May 2017. Additional easing beyond that point could well be required depending on the actions of other central banks. We expect core inflation, despite that, to be below 2% come mid 2017. Monetary easing won’t be completely ineffective over the next 12 months, however. We would expect another step up in household sector leverage; a rise in house prices; some additional (relative to a baseline) apartment & housing construction; a reduction in the global purchasing power of Australians but some stimulus as the AUD falls; and a little more GDP and employment growth (both, borrowed from the future).

Advertisement

Macquarie has more:

We remain of the view that the RBA has more work to do. But at present we are not inclined to forecast an automatic follow-on rate cut in August. Our current forecast is for a further 25bp rate cut in November. Market expectations had not fully incorporated a cut at the May meeting. We would expect that a degree of further easing will be priced in from here. That should work to put downward pressure on the A$, which we currently forecast to reach US$0.74 by June, and US$0.69 by end-16.

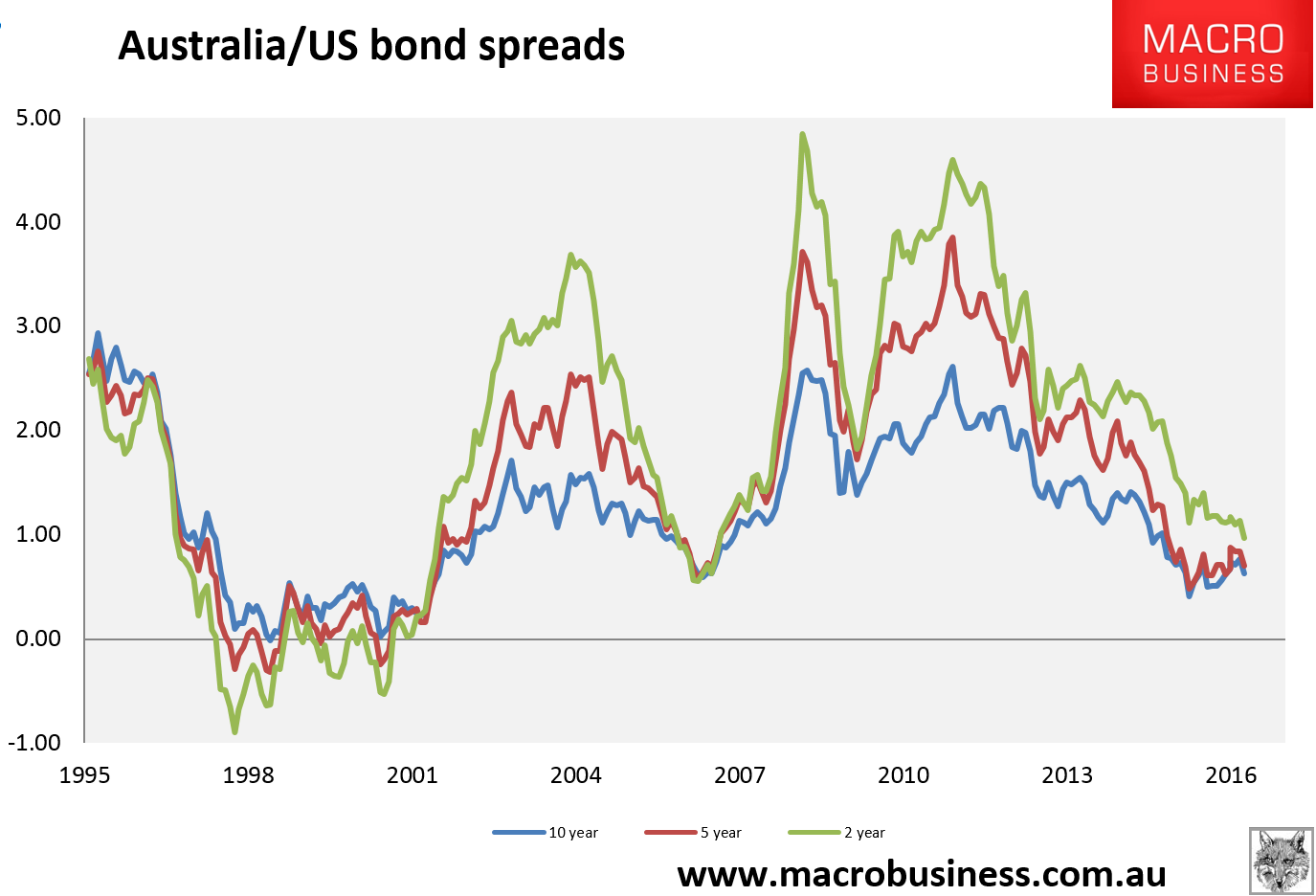

The Australian/US 2 year bond spread is now 109bps the slimmest it’s been since the GFC. The last time it reached 50bps (see Macquarie’s chart) the dollar was at 60 cents:

Advertisement

I’m skeptical that the Fed will get past one more hike. A third is an absolute hawkish outlier. Thus the RBA will have more to do to get the dollar to 60 cents. A 1.25% cash rate might do it. 1% will so long as the business cycle holds. But we still think we’re going all the way to Aussie ZIRP, our guess is 75bps given the need to fund the current account deficit.

The question now for bond investors enjoying the good times is when and whether to get out before any tipping point that reverses Aussie yields higher in a current account deficit adjustment and panic. Not yet!

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.