Fresh from welcoming back crooked Chinese at the Bank of Melbourne, Westpac is now throwing open its doors to specufestors, from Domainfax:

Westpac, the country’s biggest lender to landlords, is lowering the size of the deposits it will require from property investors, partially reversing last year’s crackdown.

After a sharp slowdown in lending to property investors, Westpac and St George, which it owns, this month told mortgage brokers the maximum loan-to-valuation ratio (LVR) for new mortgages for property investors would rise to 90 per cent, up from 80 per cent.

The change means property investors need a deposit of 10 per cent of a property’s value, compared with 20 per cent previously.

It comes as banks are offering more competitive interest rates to property investors in an attempt to boost growth now that this segment of the market is growing well below the Australian Prudential Regulation Authority’s 10 per cent a year speed limit.

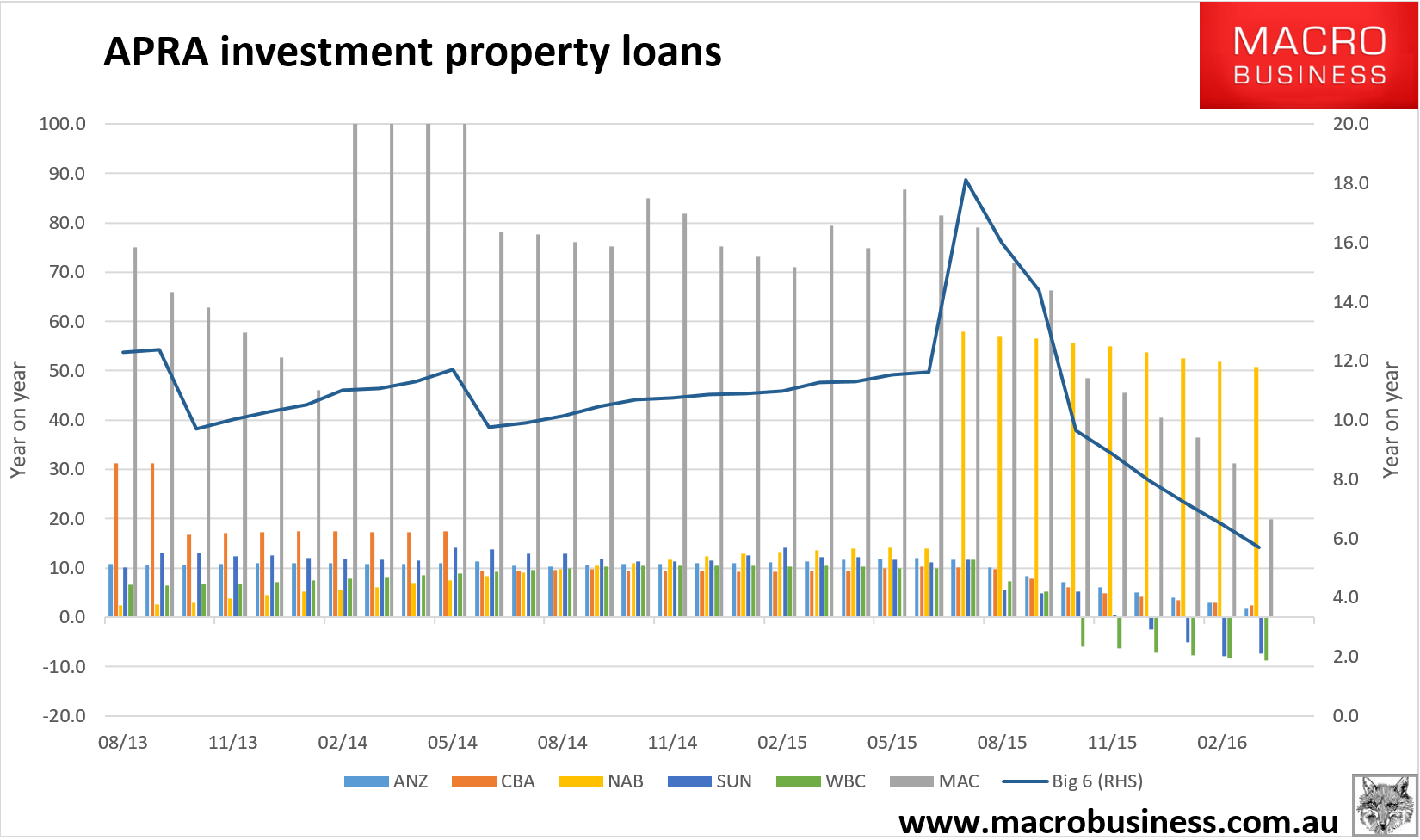

Lending growth is indeed well below the APRA 10% limit with big six bank growth down to 5.7% year on year:

WBC is at -8.8% but that is largely because of portfolio adjustments:

| ANZ | CBA | MQG | NAB | WBC | BOQ | BEN | SUN | |

| Mar-16 | 82270 | 128065 | 9220 | 96825 | 135712 | 11981 | 11370 | 11322 |

| Feb-16 | 82469 | 127835 | 9221 | 96531 | 135351 | 11919 | 11243 | 11332 |

| Jan-16 | 82656 | 127872 | 9257 | 96114 | 135471 | 11680 | 11229 | 11414 |

| Dec-15 | 82766 | 128018 | 9269 | 95749 | 135279 | 11470 | 11258 | 11475 |

| Nov-15 | 82722 | 127957 | 9311 | 95278 | 135372 | 11295 | 11280 | 11595 |

| Oct-15 | 82718 | 128396 | 9253 | 94384 | 134938 | 11166 | 11292 | 11701 |

| Sep-15 | 82911 | 129616 | 9264 | 94019 | 149687 | 11062 | 11266 | 11800 |

| Aug-15 | 83426 | 130791 | 9230 | 93404 | 151359 | 11056 | 11232 | 11856 |

| Jul-15 | 83930 | 130419 | 9242 | 93209 | 156296 | 10833 | 11168 | 12510 |

| Jun-15 | 83508 | 129719 | 9017 | 66637 | 152499 | 11110 | 11128 | 12397 |

| May-15 | 82482 | 127904 | 8802 | 65759 | 150869 | 10658 | 11147 | 12335 |

| Apr-15 | 81665 | 126268 | 7856 | 65017 | 149755 | 10671 | 11110 | 12288 |

| Mar-15 | 80824 | 125088 | 7688 | 64229 | 148784 | 10645 | 11061 | 12214 |

This should not be viewed as an opportunity by the banks. Rather, it should be viewed by APRA as a chance to lower the limit immediately before the banks charge back in. The cap has proven very effective at 6% without crashing anything. Banks are already cutting apart their owner-occupier lending standards and if they now reverse investor mortgage tightening as interest rates are cut then it’ll be off to the races again for another round of chase the bubble.

Move NOW APRA.