Chris Weston, Chief Market Strategist at IG Markets

It was deemed the action of least regret, and the RBA chose to get ahead of the curve instead of waiting for another quarter of subdued inflation data. Clearly, we will see a further explanation of this cut reflected in Friday’s Statement on Monetary Policy, but the RBA, sensing a period of inflation outside of their target range, has acted in-line with their inflation-targeting mandate. The RBA believes this will not cause a sudden spike in housing activity and this would have been a key consideration. Importantly, one bank has already said they will pass the full cut on.

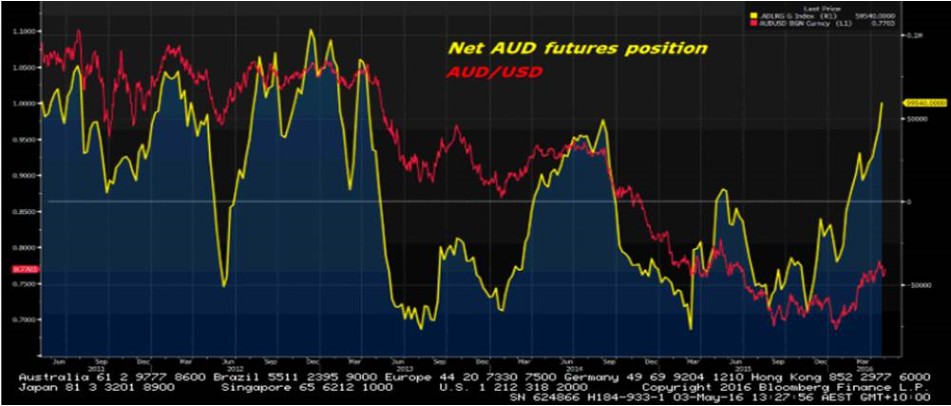

We went into the meeting knowing that institutional leveraged funds were holding the largest net long position since Q1 2013 (see Bloomberg chart below). Retail traders have certainly been more sanguine and IG’s clients had a much cleaner reflection of market pricing, going into the RBA meeting with 52% of open positions net long. Certainly, short positions have been building since the poor Q1 CPI and again this has been mirrored in the implied probability of a cut, which just prior to Q1 CPI stood at 15%. The fact that the hedge fund community were running such a long position could have been another consideration for the Reserve Bank. Cut rates, back up and give credibility to the commitment to its gentle jawboning and ultimately take away a key factor for holding AUD longs.

(Source Bloomberg)

The reaction in the AUD has been swift and aggressive with AUD/USD dropping from $0.7708 to a low (so far) of $0.7555. The 1.3% downside move has still been over shadowed by the 2.03% drop after Q1 CPI, but moves in AUD/JPY even more aggressive, which is what you would expect given it has been smashed of late. Traders have piled into Australian bonds, with two-year bond yields falling 13 basis points.

The question now is whether the RBA will back this with a further cut this year. Certainly, the statement leaves the door open to further easing, although it is not sufficiently dovish enough to feel they are going to cut below 1.5% anytime soon. How many central banks currently have the ‘door ajar’ now for further moves?! As it stands, the market is pricing in further easing over the coming year and this may be enough to push AUD/USD into the March and April lows of $0.7500 and onto $0.7450 (the 38.2% retracement of 14.8% rally seen between January and April). Long EUR/AUD looks like a better trade right now, given the USD is so out favour and I would be holding for a move into $1.5350 area.