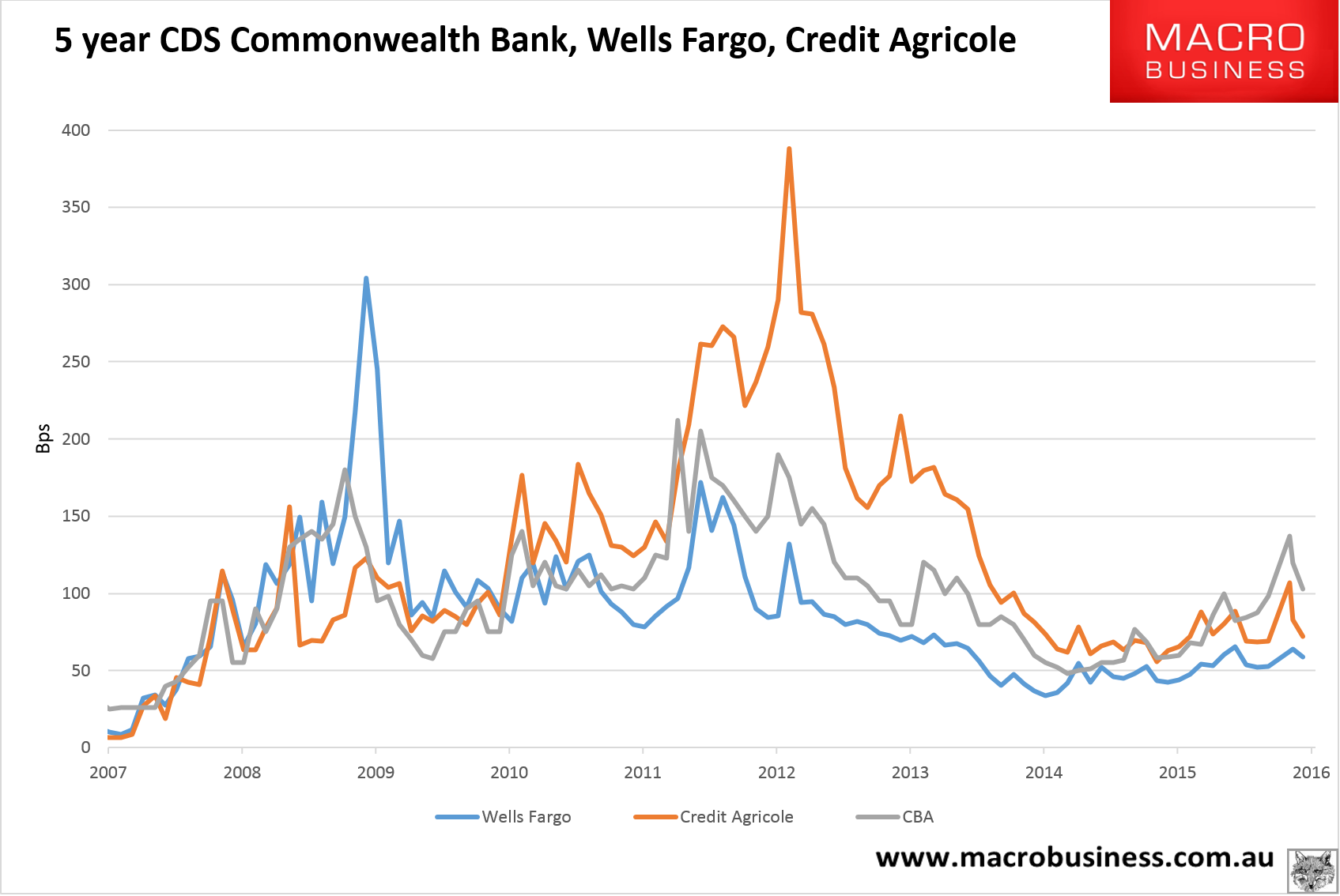

The latest figures for Australia’s bank fund cost rocket are that we’ve seen virtually no movement in a week with CBA CDS still stuck at 103bps yesterday:

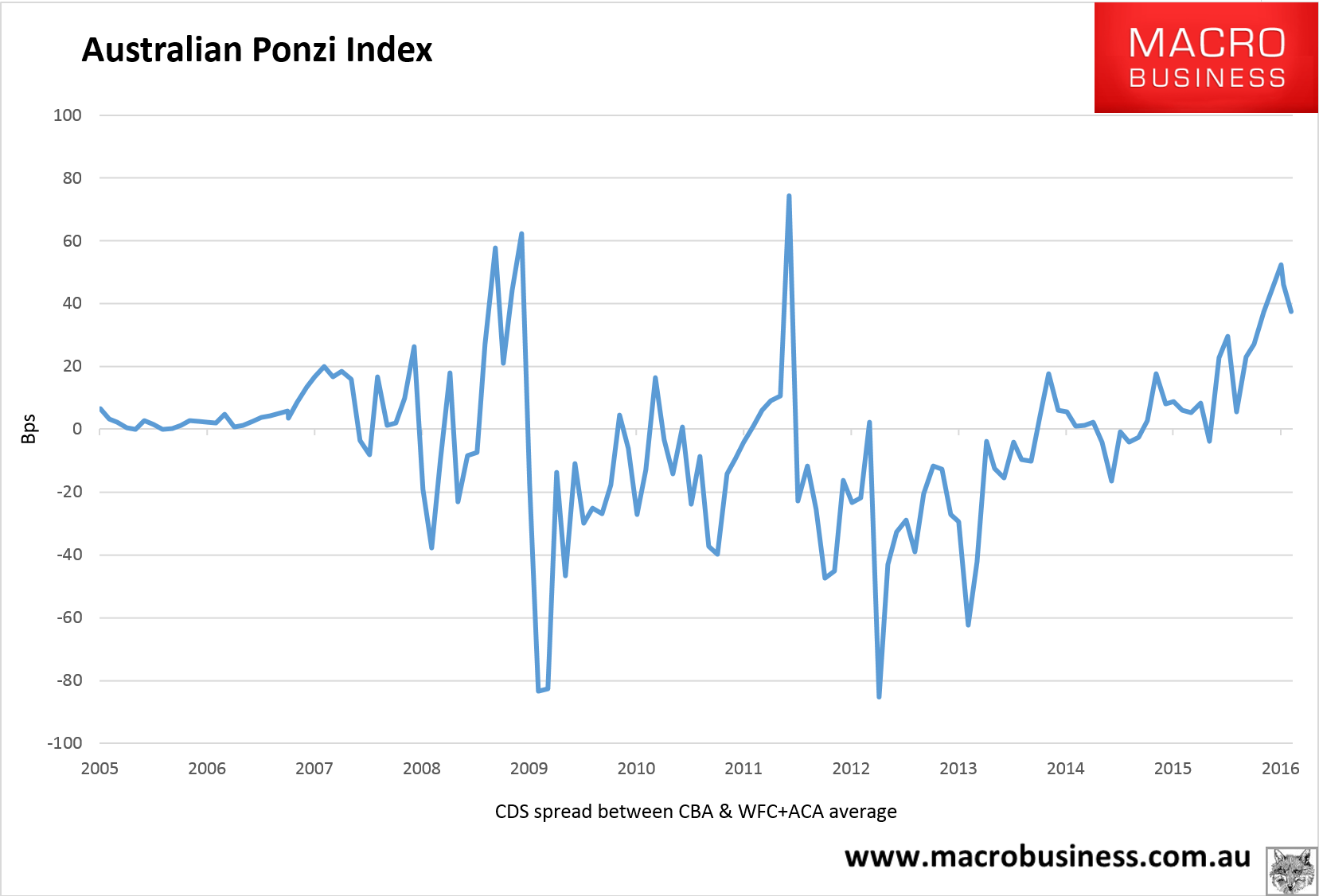

There’s been little movement in our US and European proxies, either, so the Ponzi Index is also unchanged:

Advertisement

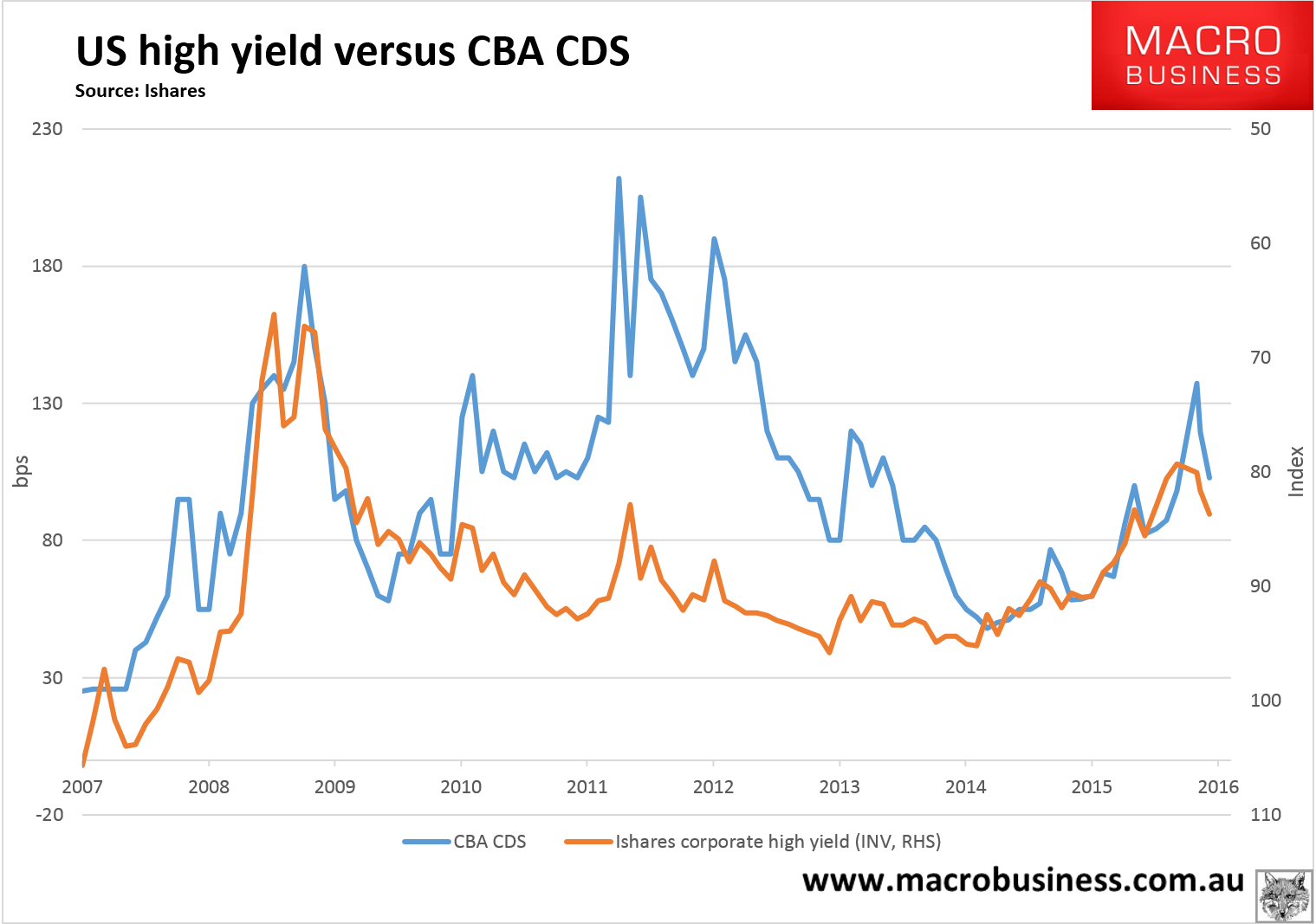

In looking at what might be ahead for the rocket in the near term, I’ve charted the CBA CDS versus the US high yield bond index, which has been an excellent barometer of global credit stress given its huge exposure to US shale, the key sector in the oil component of the Mining GFC:

I expect that the HY index spreads will continue to tighten as oil rises past $50. When the US rig count bottoms then that’ll be it for the rally is my guess so we may yet have a few weeks left of improving CDS spreads for Aussie banks.

Advertisement

After that we should see oil roll over again (perhaps after some consolidation) and expect spreads to widen again. If I were a bank looking for funding I’d take this window right now.

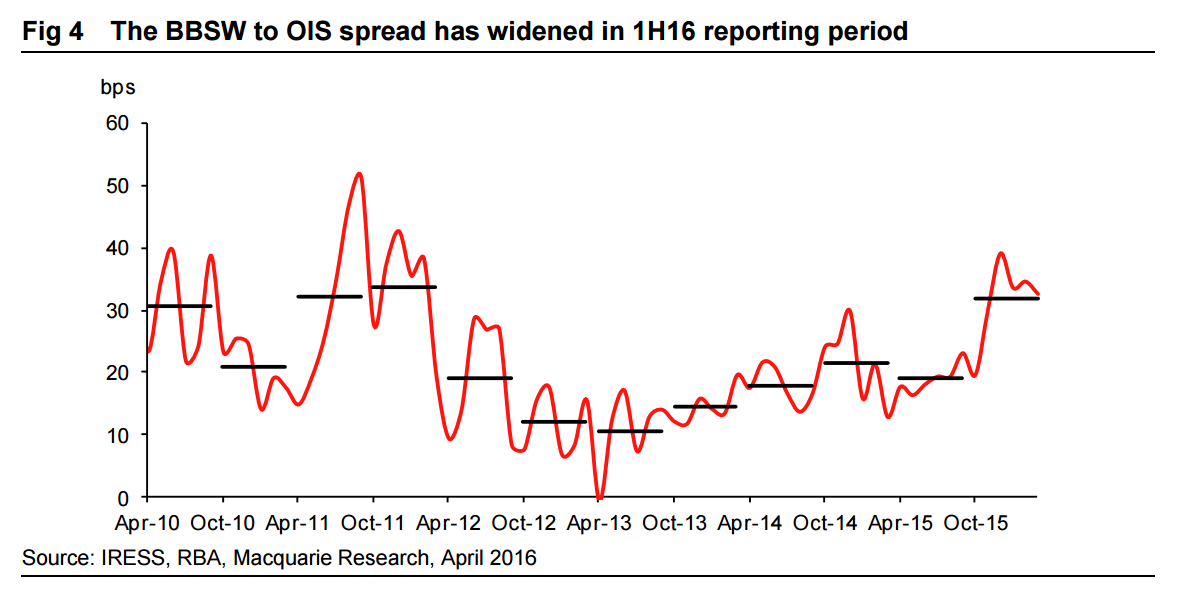

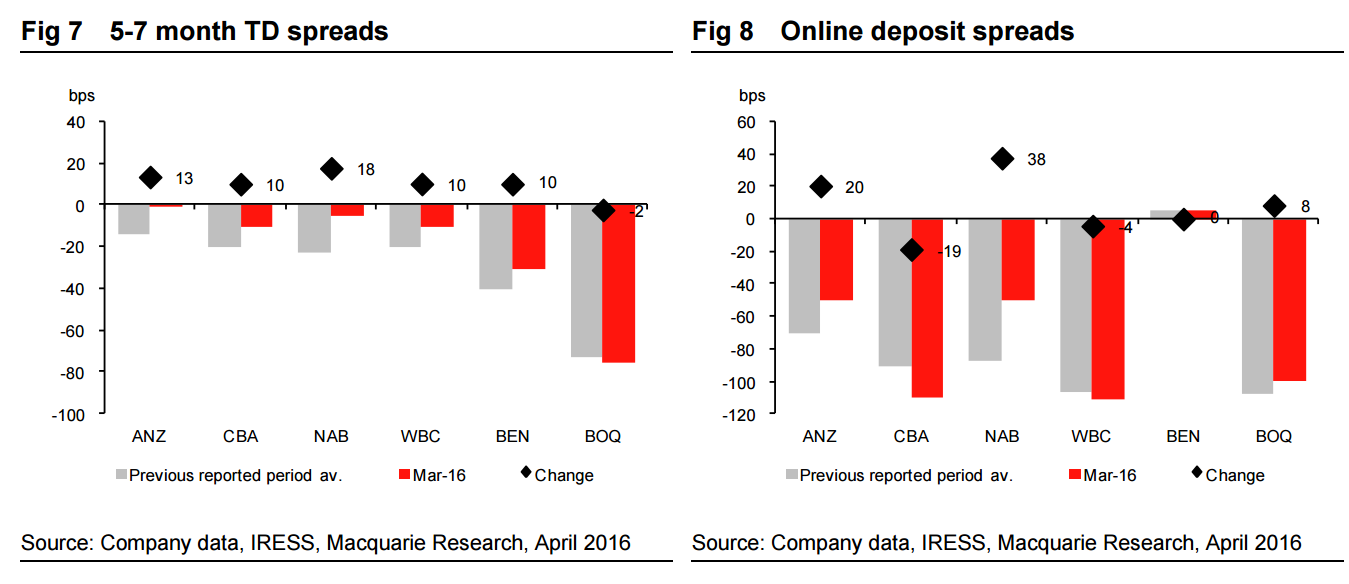

Turning to next week’s bank results, Macquarie sees funding spreads as the key:

In our view, margins remain a key issue for the sector in 2016 with tighter funding conditions increasing margin pressure. Going forward we expect the NSFR rules to be a likely drag on earnings and we would expect to see an increase in deposit competition given the current banks funding gap. While further potential repricing initiatives will go some way in offsetting these negative pressures, timing is uncertain. We note that banks generally avoided repricing ahead of the elections and to that extent we expect any repricing may be delayed until after the federal election. We discuss the factors influencing the margin in further detail below.

Widening BBSW-OIS spread indicative of tightening funding costs – The BBSW to OIS spread has widened ~10bps since the start of 1H16 with the spread currently at 33bps (at 31st March). While we expect the banks to offset some of these pressures through selective business lending repricing as well as deposit repricing, we believe a wider BBSW-OIS spread in 1H16 could take ~3bps off banks’ margins.

Lack of deposit competition unlikely to last. As our deposit pricing data highlights, TD spreads continued to tighten, with each of the majors seeing improvements in spreads relative to the average of their previous reporting periods (based on 5-7 month TD spreads). While this is clearly positive for 1H16 margin trends, the funding gap continued to widen in the environment of relatively strong credit growth. Given funding is increasingly becoming a focus of regulation, we believe it is only a matter of time before one of the majors breaks ranks and this would force the hand of the sector

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.