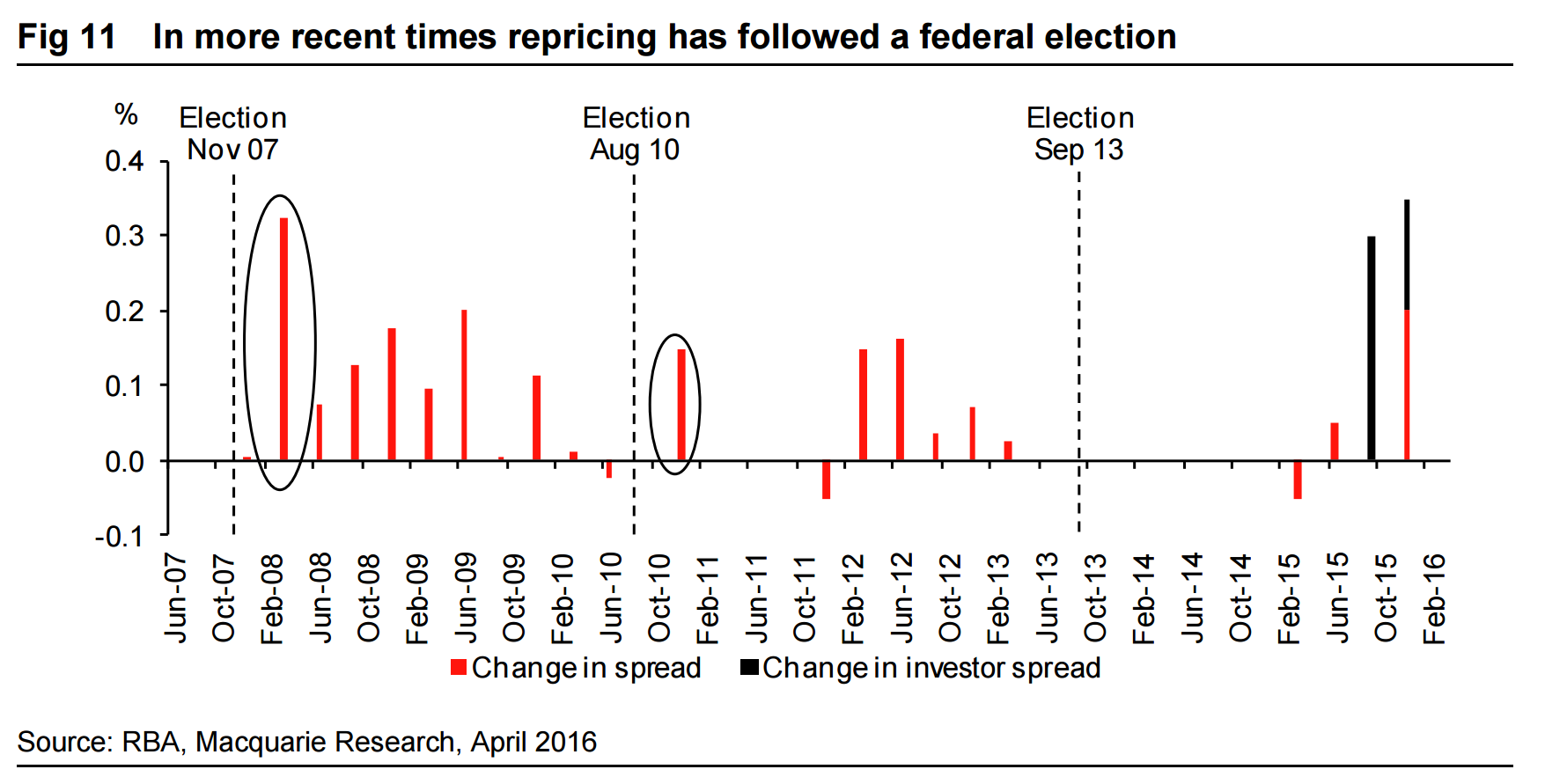

It is this chart from Macquarie:

We know bank margins are under pressure from funding costs and bad debt rises so they are going to pull the trigger on another out-of-cycle rate hike sooner rather than later and after the election looks a damn good prospect based upon recent history. Thus the RBA will need to ask itself post-election not only whether or not it thinks the economy needs a rate cut but whether it can endure a rate hike moving into what will be a difficult second half as:

- China’s boomlet fades;

- the US mulls a second rate hike;

- tradables have slowed on the dollar bounce,

- the capex triptych of cars, resi and mining combine, and

- consumers struggle with stalled and falling house prices.