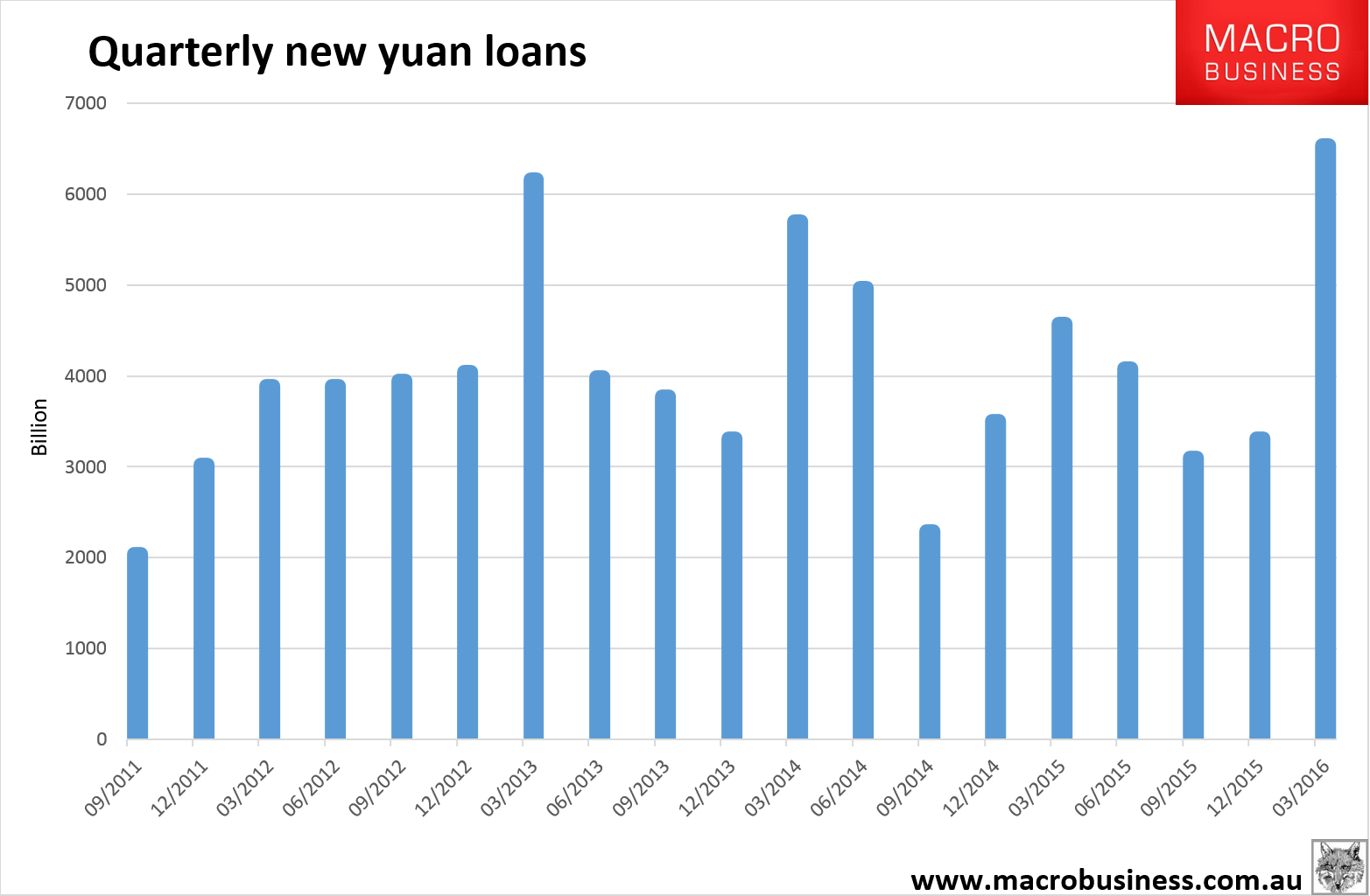

The response to the crisis of 2014/2015 appears to be greater than the response to the financial crisis of 2008/9. Between November 2008 and November 2009 total domestic credit expanded from 36.3Trn RMB to 48.4Trn RMB, a change of 12.1Trn or ~34.4% of 2009 GDP. Between February 2015 and February 2016 domestic credit has grown from 111.2Trn RMB to 139.2Trn, a swing of 27.9Trn, or ~40.4% of GDP.

The evidence for this can also be found in the money supply growth figures and the growth in the assets and liabilities on the balance sheets of Chinese banks. M2 money supply growth has recovered from trough levels witnessed in mid-2015. However, it is M1 money supply growth – the measure of the more liquid component of the money supply – that has really taken off. Meanwhile, we have seen a surge in the growth of Chinese domestic banks’ assets and liabilities since the start of 2015.

Which brings us to the topic of the moment – accelerating credit formation growth and widening credit spreads. The explanations fall into the same categories they always fall into: Chinese policy is simple-minded and focused only on averting the immediate disaster; Chinese policy making is dysfunctional; Chinese policymakers have a plan… but that plan has not revealed itself to you yet. The incremental ~$1 trillion of credit pumped into the system since January looks, for all the world, like an enormous overreaction. However, it is just possible that Chinese policymakers – after getting so much right for the last 30 years – truly are crazy like a fox.

Whoa! It’s not as big as it looks, however, given China’s marginal return on each new yuan of debt issued has collapsed over the same period. That’s why we’ve seen growth keep falling throughout much of the credit “surge” as much of the liquidity chases asset markets around the country like a cluster of under-7 footballers, first shares, then bonds, then property now commodities. .

I still see this as another round of “glide slope” management much like 2012/13 not 2009:

Advertisement

I remain of the view that we’ll get a solid 2016 out of it but that it will fade through the second half.

That rather begs the question what comes next? Will we get another another can kick next year? It’s a reasonable prospect. My own time frame for the Chinese growth glide slope is for it to be kept firm through much of 2017 as we approach the 29th National Congress of the Communist Party of China when a bunch of Politburo seats will be vacated and Xi Jinping will have the opportunity to rid himself of the last of Hu Jintao’s lackies. Once he’s stacked the Committee I’d expect to see structural reform re-accelerate.

This is exactly what drove the 2012/13 stimulus round as Xi used better economic conditions to consolidate his power.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.