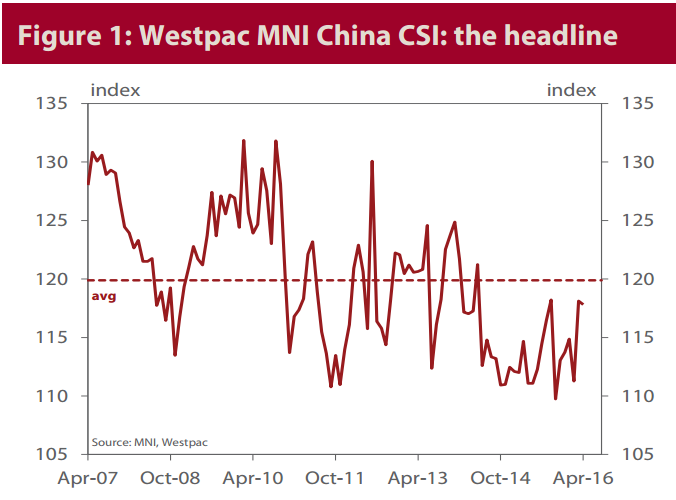

• The Westpac MNI China Consumer Sentiment Indicator edged 0.3pts lower to 117.8 in April from 118.1 in March. Sentiment has held on to most of last month’s 6.1% surge but remains 1.7% below the index’s long run average of 120.

• The Chinese consumer continues to show promising signs of improvement. The first few months of 2016 have registered a solid lift in sentiment coupled with increasingly positive readings on housing and spending related questions. There are still weaknesses – the anticipated recovery in business conditions remains elusive and consumers’ job loss concerns remain elevated – and it remains to be seen how well the improved mood is sustained but prospects for a lift in Chinese consumer-related demand now look somewhat better than they did at the start of the year.

• Among the CSI components, assessments of current conditions and the 5yr outlook improved but expectations for the next 12mths were pared back. The ‘business conditions, next 5yrs’ component posted the largest gain, up 2.3%, but continues to track a choppy path month to month and remains the weakest component overall. ‘Family finances vs a year ago’ posted a more promising 1.1% rise, the component hitting a 2yr high. The biggest drags in April were from: ‘business conditions, next 12mths’, down 2.9% but off a 2½yr high in March; and ‘family finances, next 12mths’, down 1.8%. The ‘time to buy a major household item’ component was unchanged.

• Despite the improvement in ‘finances vs a year ago’ current business conditions were seen as a touch softer than in March, the ‘business conditions vs a year ago’ index down 0.9% (note that this index is not part of the headline composite but is highly correlated with the PMIs & official IP). The index remains much weaker than indexes tracking consumers’ expectations for business conditions over the next 12mths and next 5yrs.

• Employment concerns are another notable weak spot. The employment indicator improved 1.1% in April, building on a 4.7% gain in March but at 95.1, it remains below its level in November and 9.3% below its long run average. Household expectations for inflation fell sharply in April while expectations for interest rates were largely unchanged. • Consumer attitudes towards real estate remained relatively positive. Although the housing composite dipped 0.2% in the month it remains 3.1% above its long run average. Assessments of ‘time to buy’ rose 1.4% to a new 2yr high. House price expectations softened though, pulling back 3.3% from a 5½yr high in March. The proportion nominating real estate as the ‘wisest place for savings’ lifted to a 15mth high but the proportion nominating house purchase as a ‘motivation for saving’ pulled back.

• Purchasing plans and perceived buying conditions both showed notably strong gains in April. Expenditure plans for shopping surged 6.5% to the second highest level in two years. All detailed indicators recorded solid gains. Assessed buying conditions for cars were particularly strong – the indicator up 5.5% to a record high since the question was added in 2012.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.