Chris Weston, Chief Market Strategist at IG Markets

Let’s look ahead today to the bank reporting season given it will move markets.

Key dates and important financial metrics

WBC: Reports on Monday, 2 May. The market is looking for 1H16 cash earnings of A$4.071 billion (+7.7% from 1H15), 1H dividend of 94c (+1c from 1H15 and a pay-out ratio of 77%), Common equity Tier 1 (CET1 ratio) of 10.4% and net interest margins of 2.14% (+9bp). Analysts are looking for bad and doubtful debts (BDD) to increase relative to gross loans and acceptances (GLA), with the BDD/GLA ratio increasing 6 basis points (bp) to 18bp.

ANZ: Reports on Tuesday, 3 May. The market is looking for 1H16 cash earnings of A$3.582 million (-2.6% from 1H15), 1H dividend of 84c (from 86c in 1H15). Common equity Tier 1 (CET1 ratio) of 9.6%, net interest margins at 2.06% (+2bp 1H15). Analysts are looking for bad and doubtful debts (BDD) to increase relative to gross loans and acceptances (GLA), with the BDD/GLA ratio increasing 14 basis points to 33bp.

NAB: Reports on Thursday, 5 May. The market is looking for 1H16 cash earnings of A$3.35 billion (+8.6% from 1H15), 1h dividend of 99c (unchanged from 1H15 and a pay-out ratio of 78%), Common equity Tier 1 (CET1 ratio) of 9.7% and net interest margin -3bp to 1.8%. Analysts are looking for bad and doubtful debts (BDD) to improve relative to gross loans and acceptances (GLA), with the BDD/GLA ratio falling 2 basis points to 14bp.

The trading backdrop for Australian banks

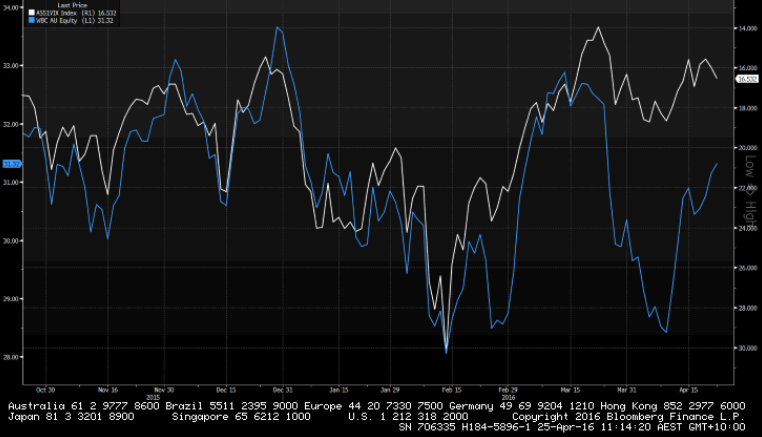

Undoubtedly the key attraction that is promoting buyers in the banks is volatility and if one can looks at the ASX or US volatility index there is a strong inverse correlation between low volatility and bank share price appreciation. Naturally this a reflection of the very compelling yield on offer, so when markets are trending progressively higher and implied volatility is low traders and investors will be chase yield and effectively look to be paid to be in a position.

(Blue line – WBC, white line – ASX volatility index)

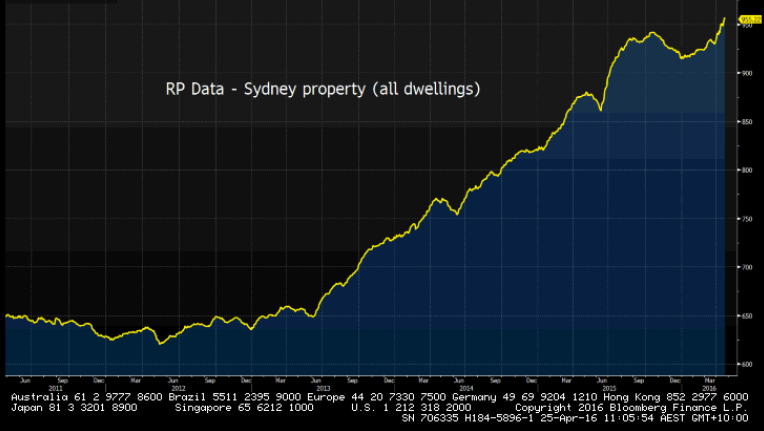

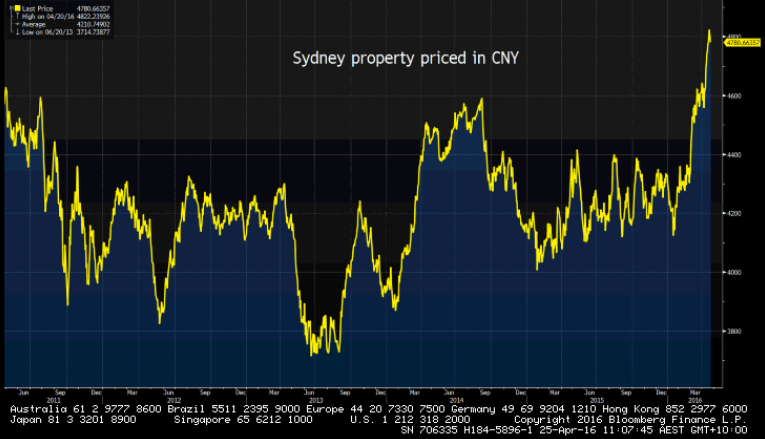

Sentiment around Australia’s housing market is always a key input, however while there has been much talk of cooling prices national auction clearance rates at pushing towards 70%, with Sydney and Melbourne rates still strong. The RP data-Riskmark Sydney property index (all dwellings) has increased 4.4% this year and is close to the all-time highs. The chart on the right shows how Chinese investors have been faring!

Key themes to focus on:

- Margins – Recent loan re-pricing should assist, but there has been fierce competition, amid an increase in funding costs.

- Capital position – The recent changes by APRA (Australian Prudential Regulation Authority) to banks capital position has seen a raft of equity raising. Despite this there is still a need to raise more than A$10 billion over the next two years to be ‘unquestionable strong’.

- Bad debts – It’s hard to believe we are going to see a sharp deterioration in retail and business divisions, but there is a belief that we may see a change in momentum.

- Markets and Trading income – Analyst expect ANZ to perform well here, but given how tough conditions were in 2H15 its likely we should see improvement here

- Total lending (volumes)

- Commentary from CEO’s around growth, the housing market and the sustainability of dividends.

Preferred position (utilising a combination of trend, price action, select fundamentals and earnings pedigree) – WBC

WBC will set the scene on Monday and the market will tend to look for signs of trends in the result that can be extrapolated into the other banks earnings. WBC tend to have the best pedigree at earnings having beaten the streets consensus estimates in six of the last eight on EPS (earnings-per-share) and four in revenue. WBC also should detail the strongest capital position and a more compelling credit risk profile, while its earnings growth is strong and only modestly behind NAB’s expected earnings growth of 8.6%. WBC should also have the highest net interest margins too.

On a technical basis all three banks look strong and are trending higher, with the five-, ten- and 20-day moving averages aligned and heading higher. Price is also above the five-day average, which shows real strength in the move and last week the bulls drove prices higher on any pullbacks. A positive short-term bias is held on the financial sector in general, but given my fundamental preference for WBC I would target a move into the March highs of $33.40 and potentially higher depending on volatility (watch the VIX) and obviously the actually earnings quality. A move below $30.14 (the 38.2% retracement of the March to April sell-off) would be a level I would exit the trade.