Angus Nicholson for Chris Weston, Chief Market Strategist at IG Markets

Oil price is likely to lead equities in lead up to Doha meeting

Asian markets were lifted after China’s Caixin services PMI followed Friday’s manufacturing PMI higher. The Japanese yen continued to trade at its lowest levels since 2014, but considering the drop in the currency the Nikkei only suffered a minor loss. The ASX looked to be bouncing strongly off the 4900 level it reached earlier in the session, with energy and materials stocks helping drive the index higher.

Oil

The oil market is beginning to look very interesting again. WTI Oil gained more than 2% as the private API survey of crude oil inventories showed a weekly decline of 4.3 million barrels, which if a similar figure to be shown in this evening’s Department of Energy release would be the first weekly decline seen since the week ending 5 February. Such a release could provide a further boost to the oil price.

But we look set to see high volatility in the spot price as different countries make announcements in the lead up to the 17 April oil producers meeting. Saudi Arabia’s claims on Friday pushed the price down, while Kuwait’s announcement overnight pushed it up again. This sort of volatility looks set to increase as countries use these public statements as tactical positioning ahead of the meeting. The sharply negative turn in Saudi Arabia’s comments recently does make a deal seem unlikely, but it is possible they have tactically decided to do this to encourage better terms for themselves and still plan to see some sort of deal agreed. In any case, there does seem more upside potential in the oil price for a successful deal than downside if it fails.

My personal preference is to wait till oil at least drops below US$35 before going long, whether that be in the spot price, high-yield debt, emerging market indices, or the NOK and CAD.

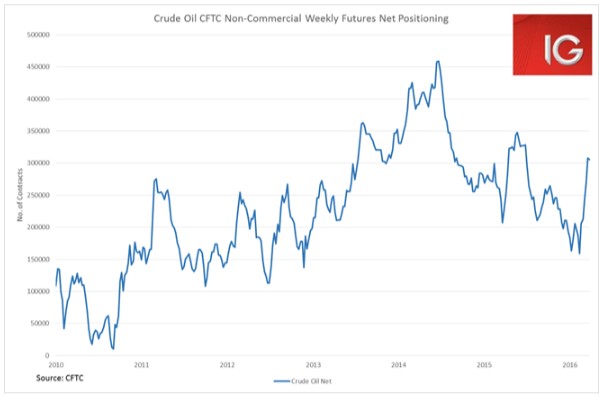

The net positioning in CFTC futures contracts in WTI oil are at their highest level since July 2015, showing that investors are extremely bullish with oil in the sub-US$40.

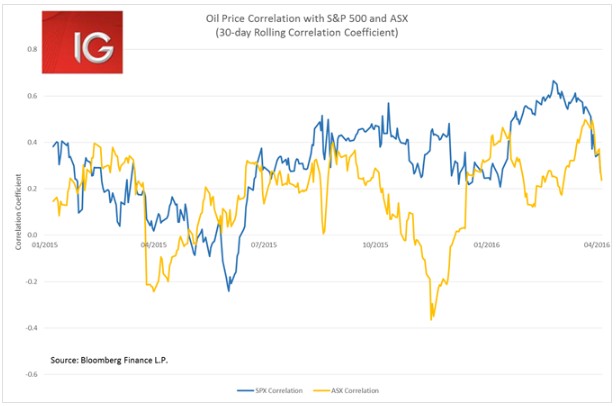

The oil price has pulled back from the US$40 level two weeks ago. Normally, this would be a great concern for equity markets, which have been highly correlated with the oil price throughout 2016. But since, 21 March the correlation between equities and the oil price has been falling sharply. Although if Oil starts to drop below the US$35 level and the VIX starts to climb, it seems this correlation will inevitably begin to increase again.

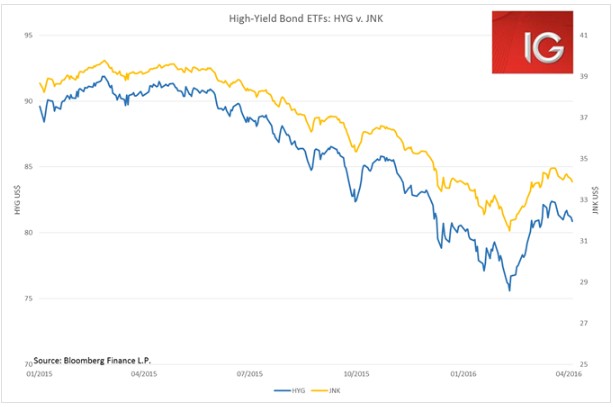

A number of people in the market have been pointing to the widening of credit spreads as foreshadowing a major pullback in the equity markets again. The two major high-yield debt ETFs, the iShares iBoxx High Yield ETF (HYG) and the SPDR Barclays High Yield ETF (JNK), have both begun to weaken since 21 March.

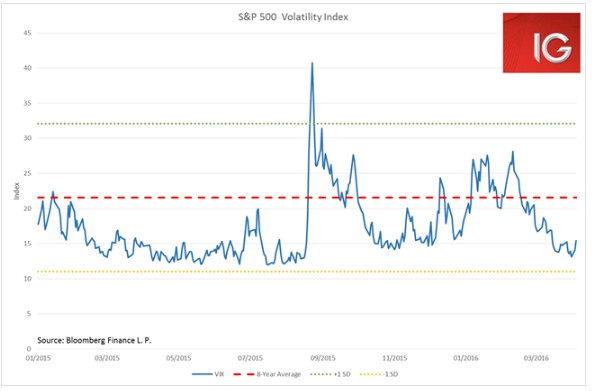

Particularly, when one considers the S&P 500 VIX index is trading close to a full standard deviation below its long-term average of late. It is understandable that many in the markets are starting to get a little concerned about the near-term outlook. Unusually low volatility and steadily widening credit spreads rarely bodes well for the short term outlook.

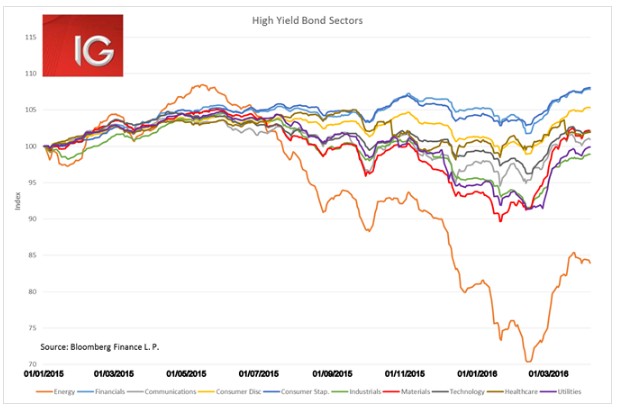

But when you look at the sectoral breakdown of the high-yield bond market, widening credit spreads are largely being driven by the weakness in the oil price, and to a lesser extent concern about the US healthcare space.