I recently went to see the movie The Big Short. I suggest you do the same.

I wrote a book on the US sub-prime meltdown and I’ve seen the many other movies on the topic but The Big Short was still fascinating and fresh even for an expert in the area.

The Big Short can be roughly divided into four big themes: how modern finance became so clever that it became stupid; the madness of crowds; the psychology of investing (bullish and bearish) and the ability of a broken system to perpetuate itself. For a taste, here is the movie trailer:

As the trailer makes clear, the movie follows the journey of a bunch of disparate outsider investors (hedgies mostly) who figure out, and stumble upon, the US housing bubble at its very core, in Wall St. The movie does an excellent job of unpacking the process of securitisation, which was at the heart of the mess, and how it delivered all of those dodgy mortgages. The easiest way for me to explain that to you is to quote myself from The Great Crash of 2008, co-authored with Ross Garnaut:

Securitisation is a practice through which an illiquid but income-producing asset, such as a mortgage, is converted into a security that is more easily traded by investors. Our story of how shadow banking evolved starts here.

…Wall Street investment banks began to tap into the booming secondary mortgage market in the early 1980s, but the traders faced a problem. They could not replicate the Fannie Mae and Freddie Mac business model because conservative investors demanded securities with AAA ratings, like those provided by the GSEs. To get around this, traders devised ingenious new methods to enhance the credit ratings of their mortgage bonds. The investment banks formed structured investment vehicles (SIVs). These were subsidiaries that had no claim on the parent balance sheet and existed beyond regulatory restrictions on leverage. The SIV borrowed to buy mortgages in the secondary market and pool them. The combined cash flows were then separated into segments or ‘tranches’. Each tranche sliced a variety of different mortgages to create different levels of risk. The lowest-risk tranches were given AAA ratings and the investment banks offered to sell these to the same set of conservative investors that liked Fannie Mae and Freddie Mac bonds: superannuation funds, governments and foreign government entities.

…The investment banks that defined shadow banking and the traditional banks that used the system’s methods had all successfully intensified the use of their capital and avoided Basel I. But eventually, all of the banks involved in ABS faced a new problem. The securitisation process shifts and repackages risk. It does not eliminate it. Therefore, when risk was shifted to create a low-risk tranche, it always left behind the securities of the residual tranche with commensurately higher risk. Because the banks were unable to sell all of these low-rated, high risk securities to investors, they wallowed on the balance sheets of the SIVs, or on their own balance sheets.

…With the early twenty-first century boom underway, interest rates at historic lows, and the rating agencies enjoying bigger roles, investment and traditional banks involved in ABS realised that they could also now use securitisation to make money from the residual high-risk tranches. These were bundled into new pools, sometimes with other securities, and then chopped up into new tranches. The top level of these new tranches had the first right to cash flows from the underlying securities, so it was assumed that unless all of the underlying mortgage backed securities went bust at once, the investment was still very safe. Known as collateralised debt obligations (CDOs), these new securities were again granted AAA investment ratings and were sold around the world to conservative investors.

Of course, this process also left Wall Street banks holding the commensurately higher-risk tranches that they were unable to sell. ‘No problem’, they said. ‘We’ll securitise those too.’ And so they did, pooling the low rated, high-risk, residual CDOs and again obtaining AAA ratings for the top tranche cut from the pools, which they then sold. These became known as CDO2 . Extraordinarily, another round of securitisation was worked upon the residual high-risk tranches of CDO2 and produced CDO3 .

In the end, during the subprime mortgage boom, investors were being offered AAA-rated shares in the top tranche of a pool of residual high-risk CDO2 tranches that had been cut from a pool of residual high-risk CDO tranches that had been cut from a pool of residual high-risk MBS tranches that were themselves underpinned by America’s highest-risk mortgages and other loans!

And the rest is history. When the underlying income stream of these Byzantine financial structures was eventually disrupted by a correcting US housing bubble then, owing to the built up leverage at every step of the process, the entire edifice imploded and a regulation asset market accident metastasised into a limitless banking calamity. Nobody in it saw it coming because they were all to busy creaming it.

In considering the lessons for Australia there is no direct correlation today despite our own housing bubble, though there was in 2006, as shadow banking melted up here too. The parallel I wish draw today is an analogy, the similarity between the pre-GFC structure of leverage upon leverage in the US and that of the entire Australian economy today.

As readers will recall, MB has a simple working model for the Australian economy. As an economy Australia earns income largely through selling dirt to the world. We then take that income and leverage it up in global markets before dumping the borrowed dough into property speculation which pumps up spending. When that process is threatened in any way the Federal Government balance sheet steps in with guarantees.

The entire economy is, therefore, analogous to a securitisation in which a perceived stable and boring income stream is leveraged up to make it much more exciting for bankers to make money to blow on whores nice houses in Mosman.

That would be OK. Indeed could produce terrific prosperity. But there is another hidden step here that makes it altogether more risky. The underlying income stream from the sales of dirt may look like a low margin, highly safe bore, but is not what it appears. It is, in fact, a highly concentrated and already leveraged income stream flowing from China. Specifically, it is the fruits of a Chinese building boom that, as one reader put is yesterday, is greatest since the Egyptian Pharoes, and is itself built on enormous and unsustainable debt.

Thus the Australian economy is not a simple securitisation. It is a securitisation of a securitisation. Leverage built upon leverage. That is, a collateralised debt obligation or CDO. And everyone with a stake in the property market is effectively holding a high risk tranche in that sovereign CDO.

At this point we can draw a second similarity to the themes of The Big Short: the madness of crowds. If you were describe the above to a friend or colleague, superior or, for that matter, bank regulator or ratings agency, you are likely to be met with a blank stare and invitation to grab your coat.

So, when one looking for vulnerabilities in this system, one should not ask anyone on the inside; forget government, regulators, banks, ratings agencies or, in Australia’s case especially, media, which is now holding an huge tranche in the economic structure as if to a piece flotsam in the deep ocean. To find these vulnerabilities and opportunities you need to look at the outsiders, the nutters as it were, for only they can tell you what you really need to know. They, themselves, constantly face the risk of solipsism in their isolation, so you have to careful which nutters you choose. Those dedicated to reason and not ideology are probably the ones you’re after.

MB is one of those, of course, so where do we see the vulnerability in the great Australian CDO? What is The Big Australian Short?

To answer that let’s turn to our third theme from The Big Short. Virtually alone in the Australian public market, the MB community has correctly described well in advance the truly monumental bear market that is transpiring in both nation’s terms of trade and its broken mining sector. Indeed while everyone else is busy defending their tranche in the sovereign CDO, the MB community has been making hay on mining and currency shorts. The psychology that has guided this success is one of clear thinking reason. If it makes no sense for an economy like China’s to continue down a certain path then it will stop. If a market is oversupplied then its prices are going to fall.

In the words of the bears of The Big Short, the biggest returns are always found when you identify a truth that nobody else wants to admit.

So, now that that mining truth is out in the open (though not yet over, don’t kid yourself!) what comes next for our sovereign CDO? Does the disrupted income stream flow up to into the higher tranches of leverage and pull them down too? The answer to that still lies in China.

The constant refrain from those who did not see the mining crash coming is China is now successfully “rebalancing” from excessive, credit-charged investment-led growth dominated by state run firms (that is, building heaps of stuff) to consumption-led, lower credit and higher productivity capital-allocation by markets, which will steadily happen without disruption.

So far that has kind of happened without being convincing. The two leading investment drivers – housing construction and manufacturing – are in contraction. The services sectors meanwhile have kept on keeping on. But even this modicum of rebalancing has resulted in much slower net GDP growth and the near annihilation of global mining and associated emerging markets. Not only that, Chinese credit continues to rise at breakneck speed as yesterday’s state run monsters refuse to die, instead borrowing anew to renew older loans and productivity continues to plunge.

At MB we have coined a phrase for this stage of the process. China has engineered neither a soft landing, nor landing for itself to date. Rather it is engaged in managing a “glide slope” to lower growth in which it deploys fiscal and monetary levers to stabilise things when the “rebalancing” gets a little too swift.

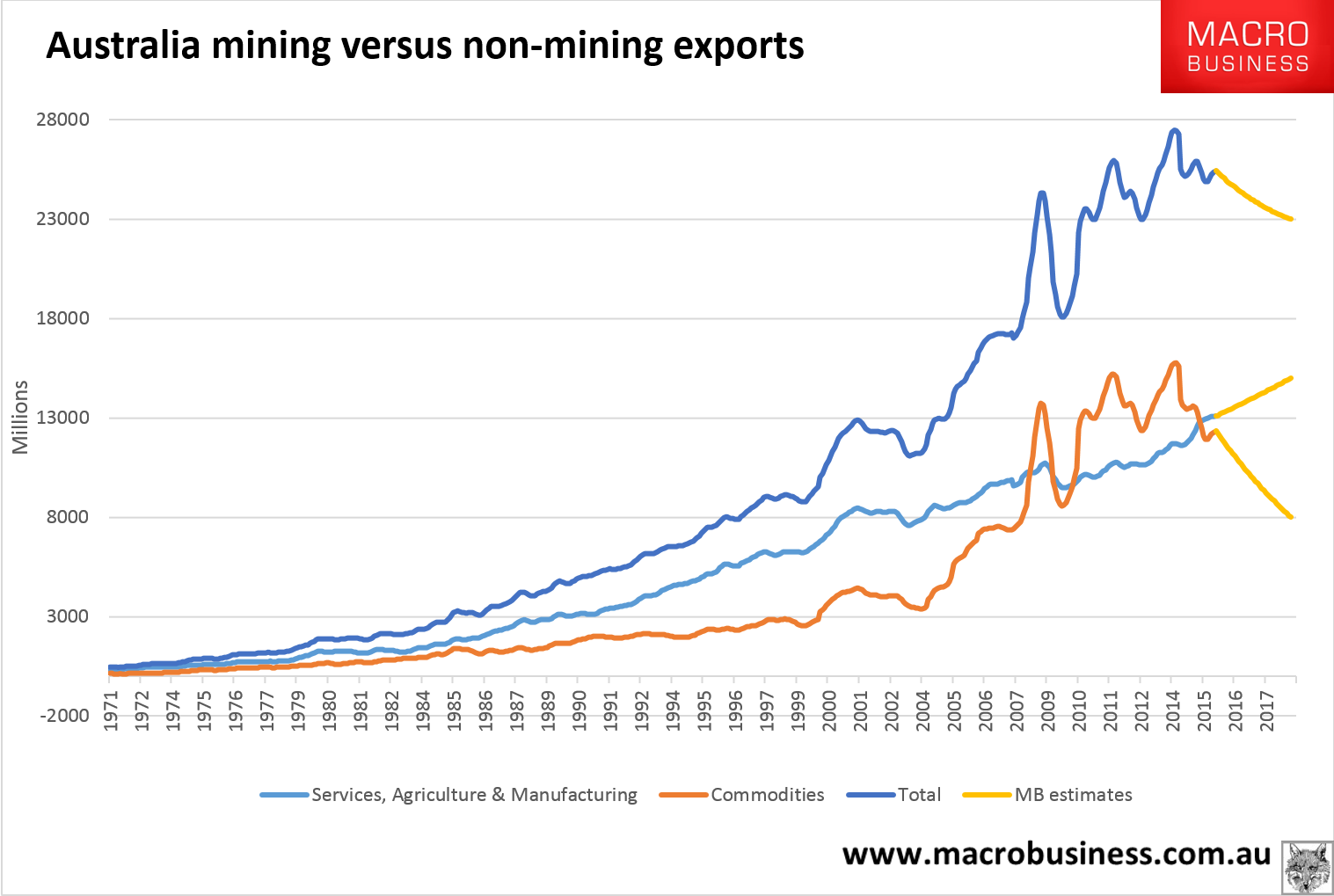

It is perhaps possible through an act of truly spectacular economic management that China could keep this up for another decade as growth steadily halves from its current rate. If that is the case then the Australian sovereign CDO faces a lost decade as its formerly booming dirt income drains away, but at least at a pace that enables alternative growing income streams to back-fill the gap. Australia is not, after all, just a securitisation product, it is a nation with its own currency which is falling and inducing new growth export industries. So, here is MB’s best effort as describing how that “glide slope” scenario would play out:

Returning to our sovereign CDO, the “glide slope” outcome sees assets get cheaper as no net export growth puts a lid on foreign borrowing (assuming authorities do not let the current account deficit blow out which is likely given it is already stretching). Asset deflations would have greater hope of being real (via inflation) than nominal (via price falls).

But we’ll need more than just a little luck because while growth crawls along at stall speed, any external shock that hits the global business cycle will potentially hammer Australia. The Big Australian Short will be our standards of living and the play will simply be to either leave or have your capital do so.

The second possible scenario for Chinese rebalancing and the Australian sovereign CDO is less comforting. It is this outcome that has the world’s hedge funds lining up to short the Chinese currency. What they see, that nobody else wants to accept, is that the Chinese rebalancing is caught between Scylla and Charybdis. The problem is that China’s rebalancing is about releasing market forces into its economy so that capital can shift from unproductive investment to new and more dynamic industries. But market forces may need to do this via a recession. Indeed there may be no other way to shake out such enormous excess capacity and restore productivity. Thus every time China allows the process to move forward, capital wants to flee the country to higher growth and/or safer opportunities. But that threatens a bust and so authorities pull back with more glide slope measures and currency controls. Of course that only makes the original debt and falling productivity problem worse.

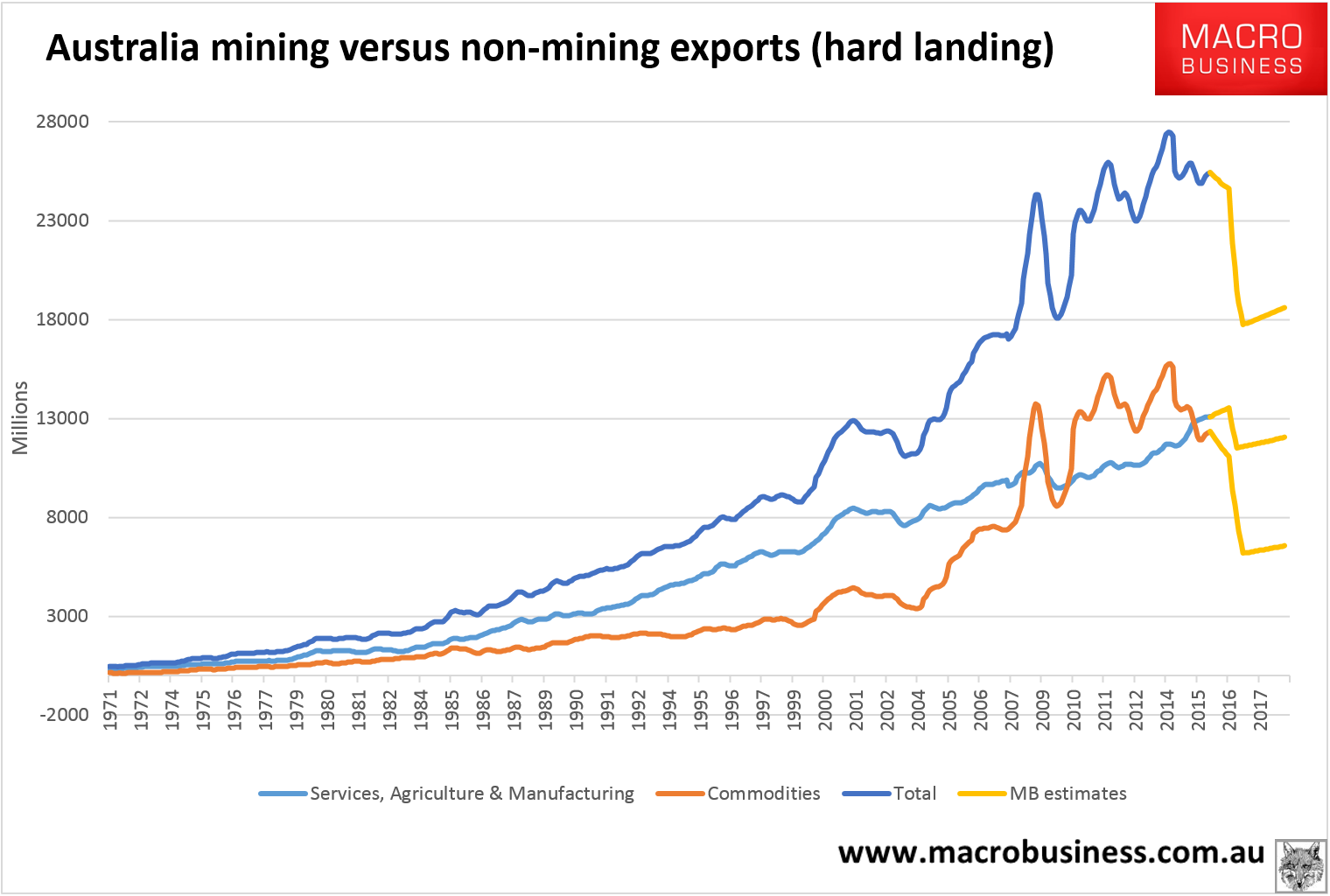

The hedgies are betting that in the end the Chinese Communist Party will have no choice but to let the process run. Otherwise it simply withdraws and faces the long stagnation of other failed Communist states and other middle income trapped development experiments. If they are right then China will very likely enter a “hard landing”. And that hits the income streams underpinning the Australian CDO very hard, before only rebounding slowly:

This is a reversion to the pre-boom trend line in Australian export growth with the consequence that the sovereign CDO comes apart as the income stream can no longer support the upper tranches of debt. The property bubble, banks, government budgets and household debt all get rationalised in a big hurry as markets force the upper tranches to contract to the receding income.

So, where does MB sit on these two outcomes? Actually somewhere between the two. I have championed the “glide slope” until now. In part because I was simply describing what was happening. The principle reason I still do not fully subscribe to the hard landing scenario is because China probably still does have the resources to support its transition, not least because it still owns its own banks so can avoid any “sudden stop” credit crunch when the rebalancing spews out enough bad loans. But, the transition is clearly going to be very troublesome and I expect Chinese growth to slow much faster than most folks are willing to accept.

Thus it still means that the income stream underpinning the Australian sovereign CDO diminishes much more quickly than it can be replenished and the upper tranches are forced to retrench. The beauty of The Big Australian Short in either case is that it remains the same. Get your money out of the country or, at least, out of anything priced in its currency.

And that brings me to my final observation about the themes of The Big Short, the resilience of the system and its ability to survive. To illustrate this, let me point out a moment in the movie with which Australians have a largely unknown intimacy. The critical point that turns the suspicious US hedgies from intrigued speculators to active shorters is a trip to a national securitisation conference in early 2007 where they meet many of the loan officers and other players who are pimping the sub-prime mortgages inflating the bubble. The hedgies are staggered by the reckless stupidity of all involved.

That event was run by the American Securitisation Forum which at that point in time it was chaired by none other than the current Chairman of the Australian Investment and Securities Commission (ASIC) Greg Medcraft, a co-founder of the august body. Let’s hope he learned some valuable lessons.

Letting that pass, the more important parallel about the endurance of a toxic system is not that Australian mortgage lending is as bad as it was in the US, it is not. However the ideological myopia and system hugging actors that produced the US sub-prime CDO meltdown are a near complete simulacra for Australian economic managers that have for decades refused to budge from the worldview that has created the Australian sovereign CDO.

See the movie.