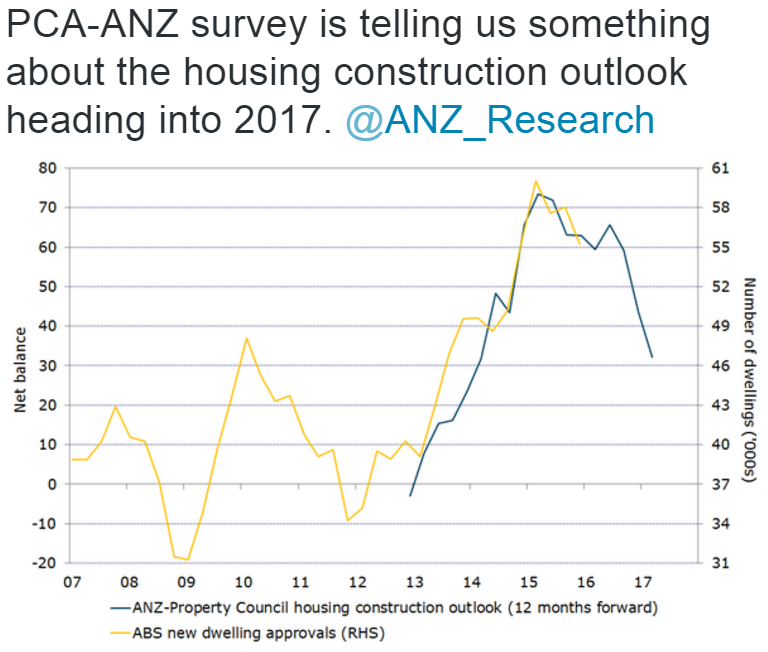

I recently published this chart from the ANZ suggesting that the downside to the resi boom is steep:

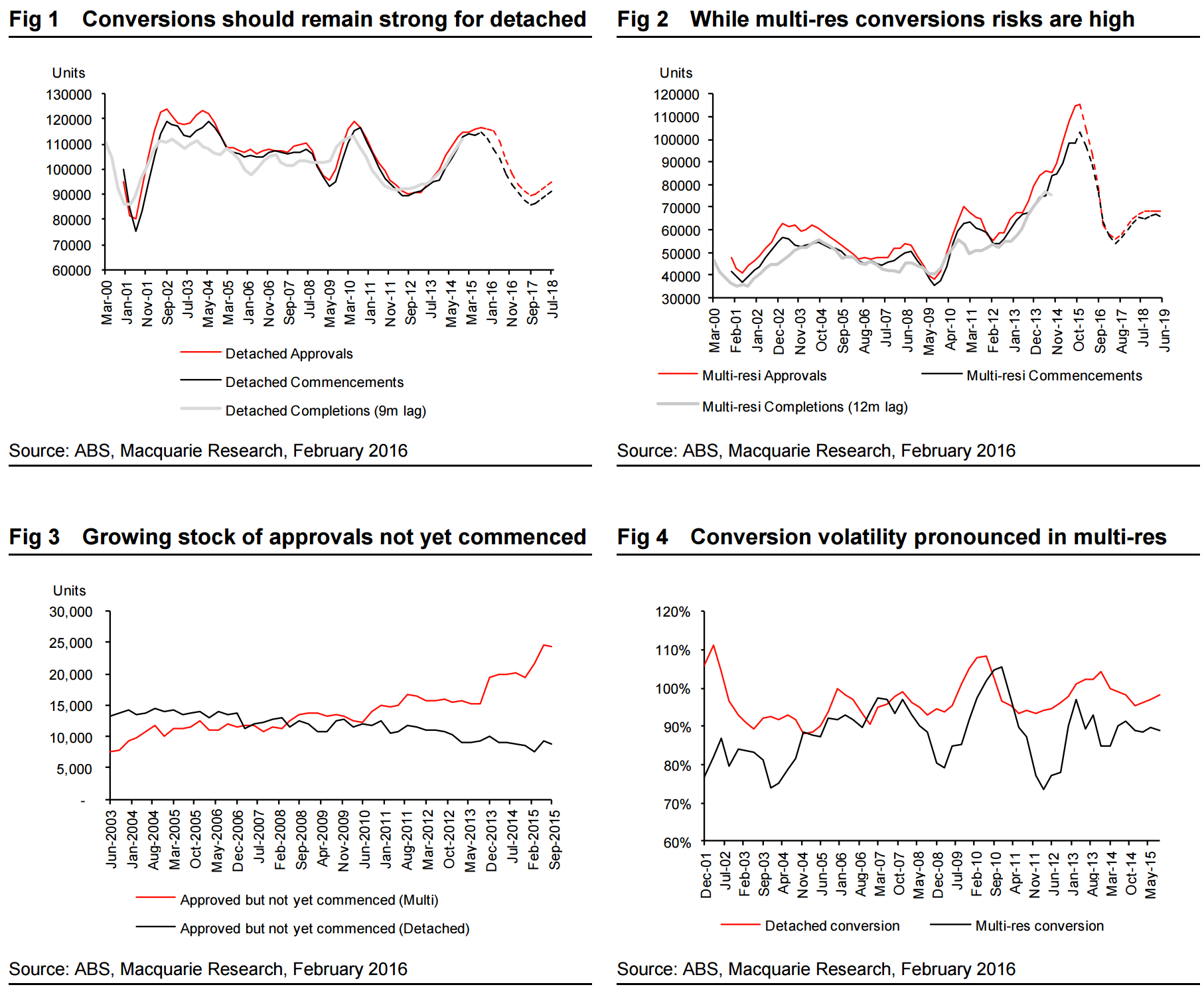

According to Macquarie it is is even steeper largely owing to conversion risk (banks tightening, fleeing Chinese etc):

Conversion of approvals to completions to be watched closely. Our key area of focus remains on conversion, particularly multi-residential which is currently tracking at 89%. As multi-residential approvals are now 49.7% of total approvals on a rolling 12-month basis, any pullback in multi conversions will have a significant impact on completions (See charts overleaf).

In the context of Australian building material activity having peaked, we maintain our caution on the space and prefer US housing exposure.

Advertisement

The resi boom added roughly 0.5% to GDP last year and a lot of jobs. Its demise will combine with the market volatility, the mining capex cliff, car assembly cliff, as well as an unsettling election in the second half of 2016 to add some dyspepsia to Australia’s “rebalancing”.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.