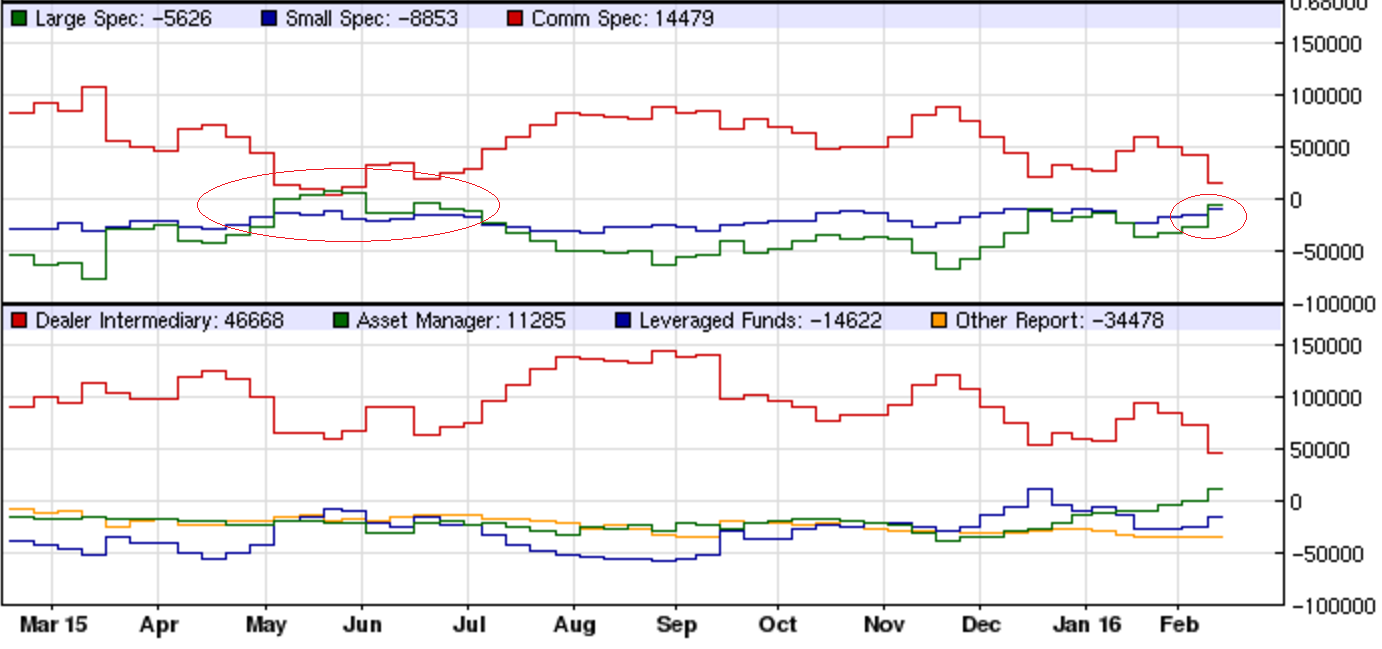

With compliments from the RBA and FOMC comes last week’s CFTC Commitment of Traders Report:

Aussie dollar shorts were blasted out of the market and sit at their lowest since mid-last year as rate hike odds collapsed in the US and flattened out in Australia after Captain Glenn fell further behind the curve in Friday’s speech.

Let’s take some time to revisit the developing context to determine whether the market move is meaningful for the MB outlook of further falls in the currency.

Advertisement

Regular readers will recall that MB has a “five drivers” model for the Aussie:

interest rate differentials;

global and Australian growth (more recently this has become nuanced for the Aussie to be more about Chinese growth best captured in the terms of trade);

investor sentiment and technicals; and

the US dollar.

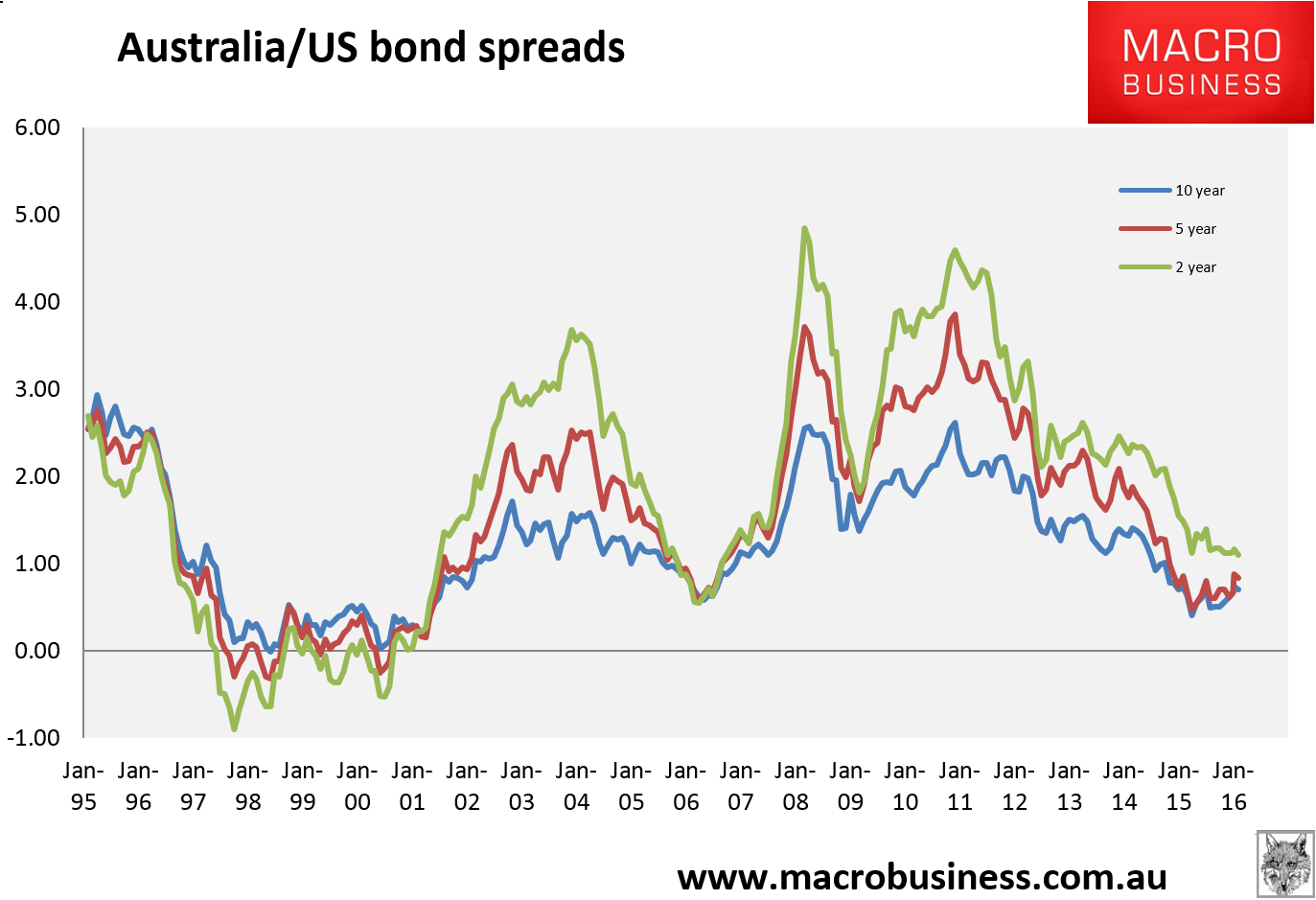

The first has been causing consternation in markets in recent weeks as several nations and a number of markets have shifted into negative interest rates. But, as I argued last week, even in these jurisdictions what matters most for the carry trade is not the level of rates, positive or negative, it is the spread between them and whether or not that offers an uplift for speculators. Australian yield spreads to the US have risen in recent months but remain in a downtrend:

Advertisement

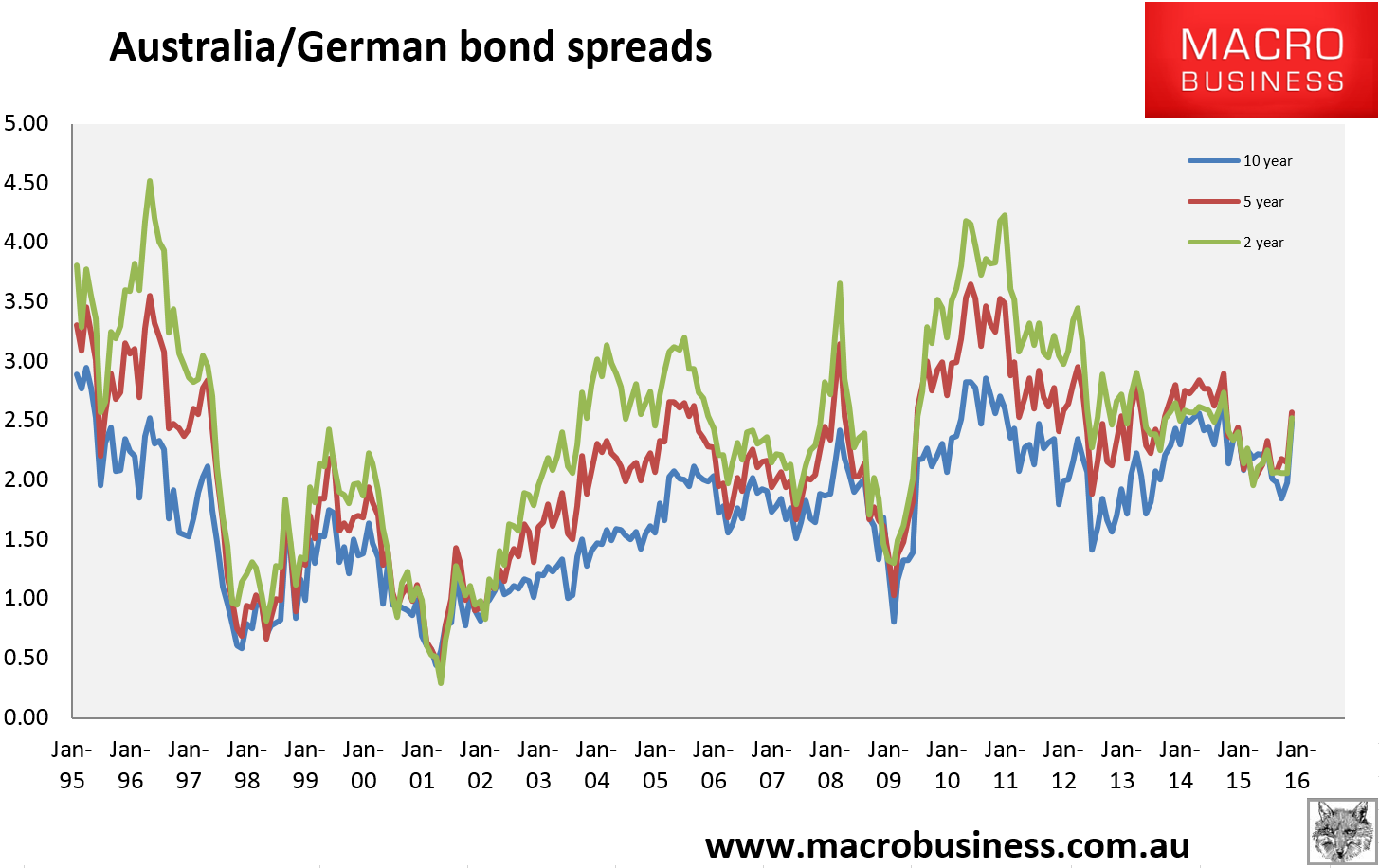

Same for Germany :

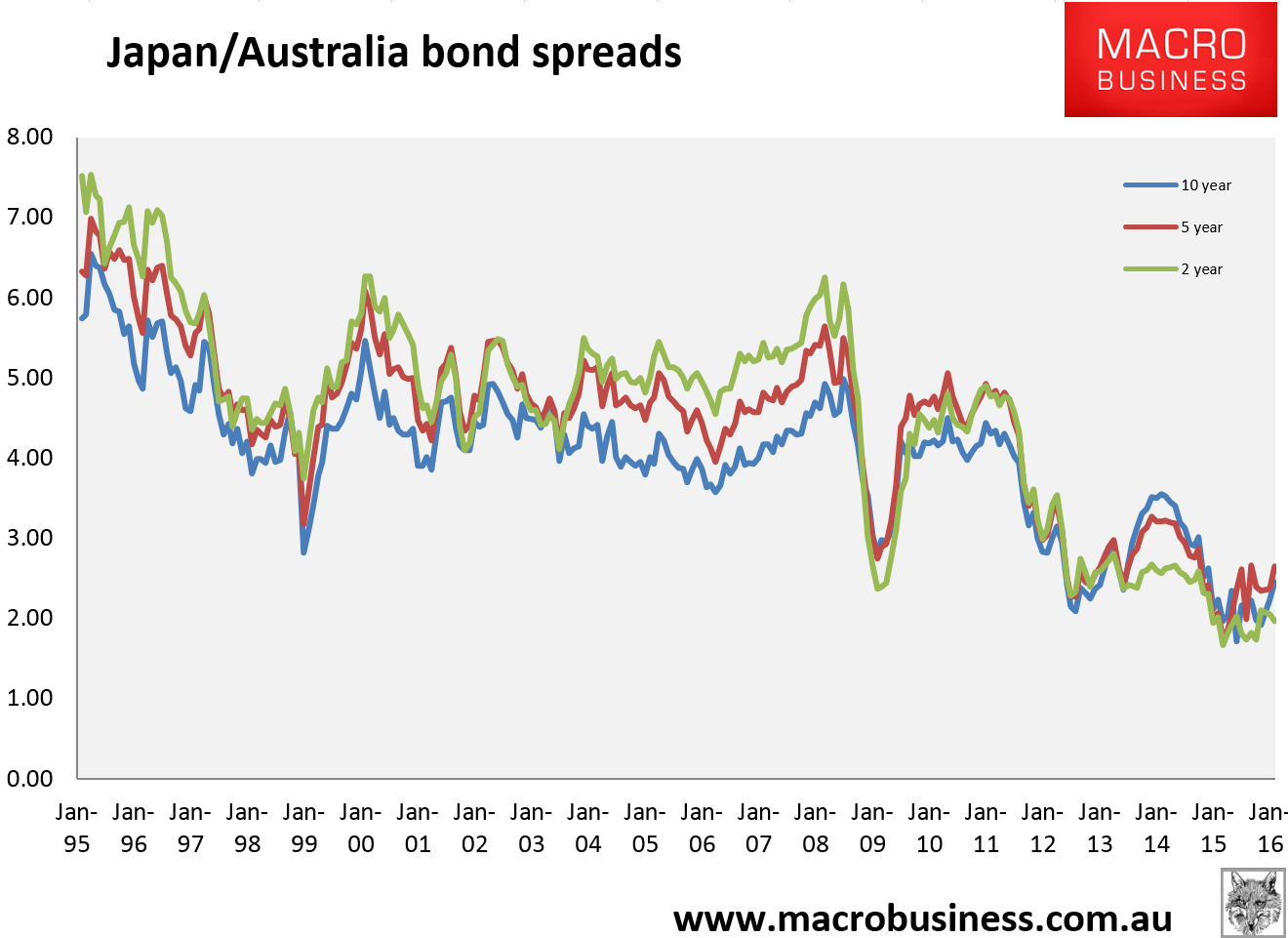

And Japan:

As well, there is greater reason to expect further interest rate reductions in Australia than there is in any of these currencies. Australia has a good 150bps left to cut should the economy require it whereas it is difficult to see negative rates falling anywhere near that much given the gloomy response that markets have given it so far. Indeed, we may actually see a recoil from negative interest rate policy in favour of greater quantitative easing given the former seems to have backfired badly in Japan with a rising currency and falling stock markets, the opposite of the intended outcome. One does not need to imagine a disaster in Australia to see its spreads to other currencies contract meaningfully into the future.

Advertisement

That brings us to the prospects for global and Australian growth, neither of which is getting any better. We can expect the following:

China to keep slowing and the yuan to keep falling one way or another;

global growth to keep slowing toward and perhaps through the 2% growth threshold below which is widely considered a global recession;

US growth to lumber on but slow on its energy-led credit crisis and stocks bear market;

emerging market growth is slow fast with widespread recessions.

This is the continuation of the Mining GFC and in this environment Australia ought also to slow to the point of needing further rate cuts as:

Advertisement

the mining, car industry and residential construction capex cliffs merge;

relative fiscal tightness;

consumers slow on falling stock markets (though house prices appear sticky for now)

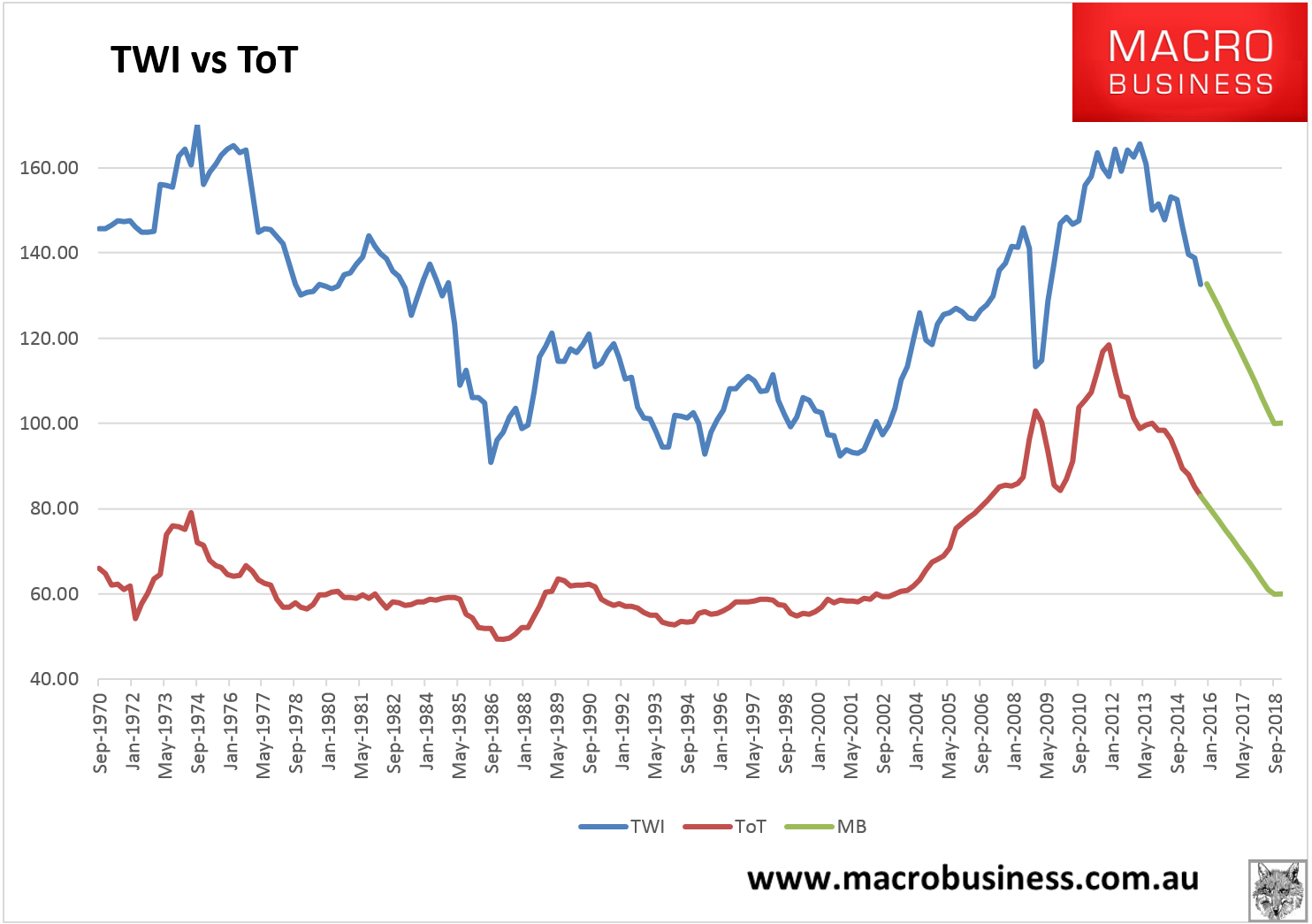

the ongoing income shock from the falling terms of trade (ToT, TWI is the real exchange rate) resumes as the bulk commodities collapse continues all of this year:

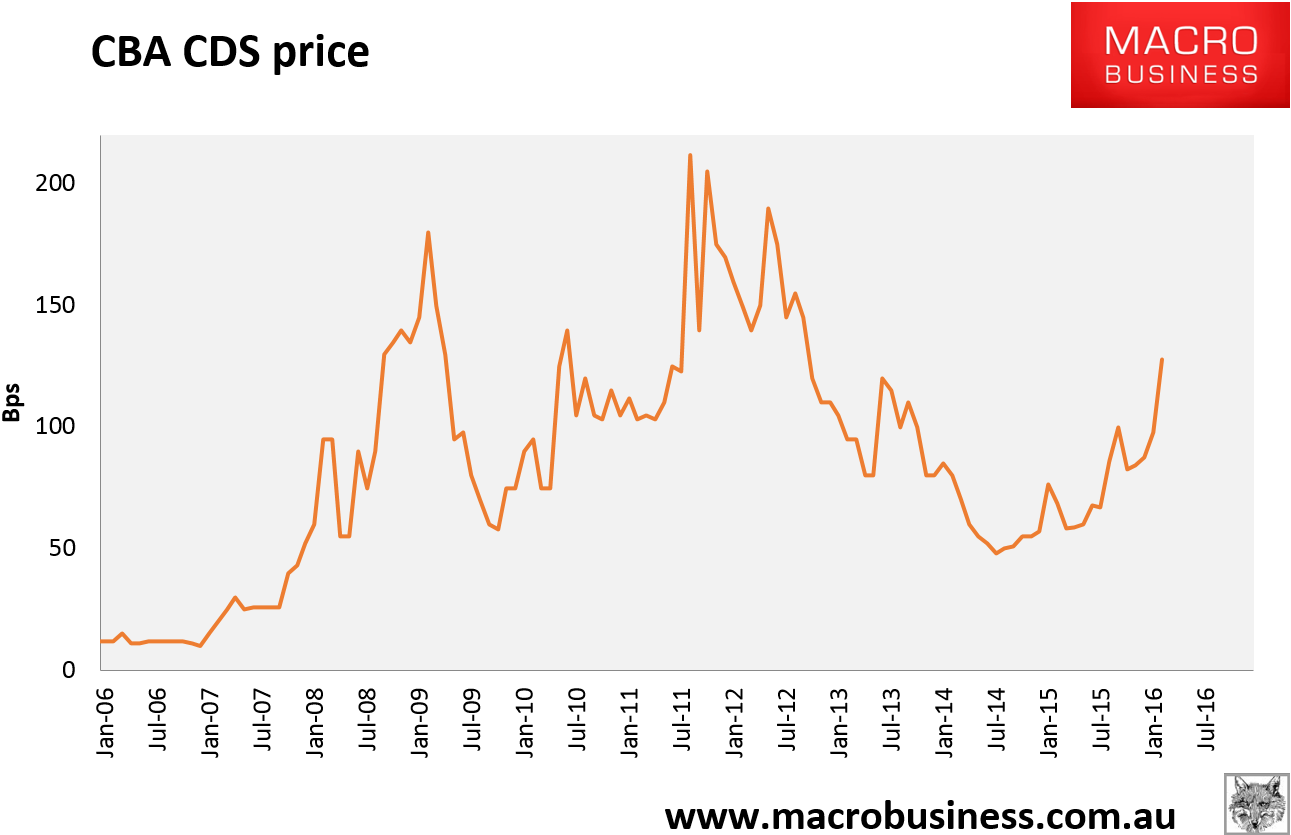

There is also the growing risk that global commodity-associated debt enters some kind of freeze as large scale bankruptcies rock the firms and sovereigns exposed to the complex. We already see that impacting the cost of Australian credit as bank funding spreads blow out and net interest margins are squeezed:

Advertisement

And this is before anything has actually happened. The obvious response to this is also further monetary easing.

For the time being, though, sentiment has turned neutral on the Aussie, as we see in the COT report. Is that a cause for concern? I don’t think so. There have been four stable periods for the currency during its great cascade, all coinciding with brief periods of Australian bond spread out-performance:

Advertisement

Sentiment will turn when growth does.

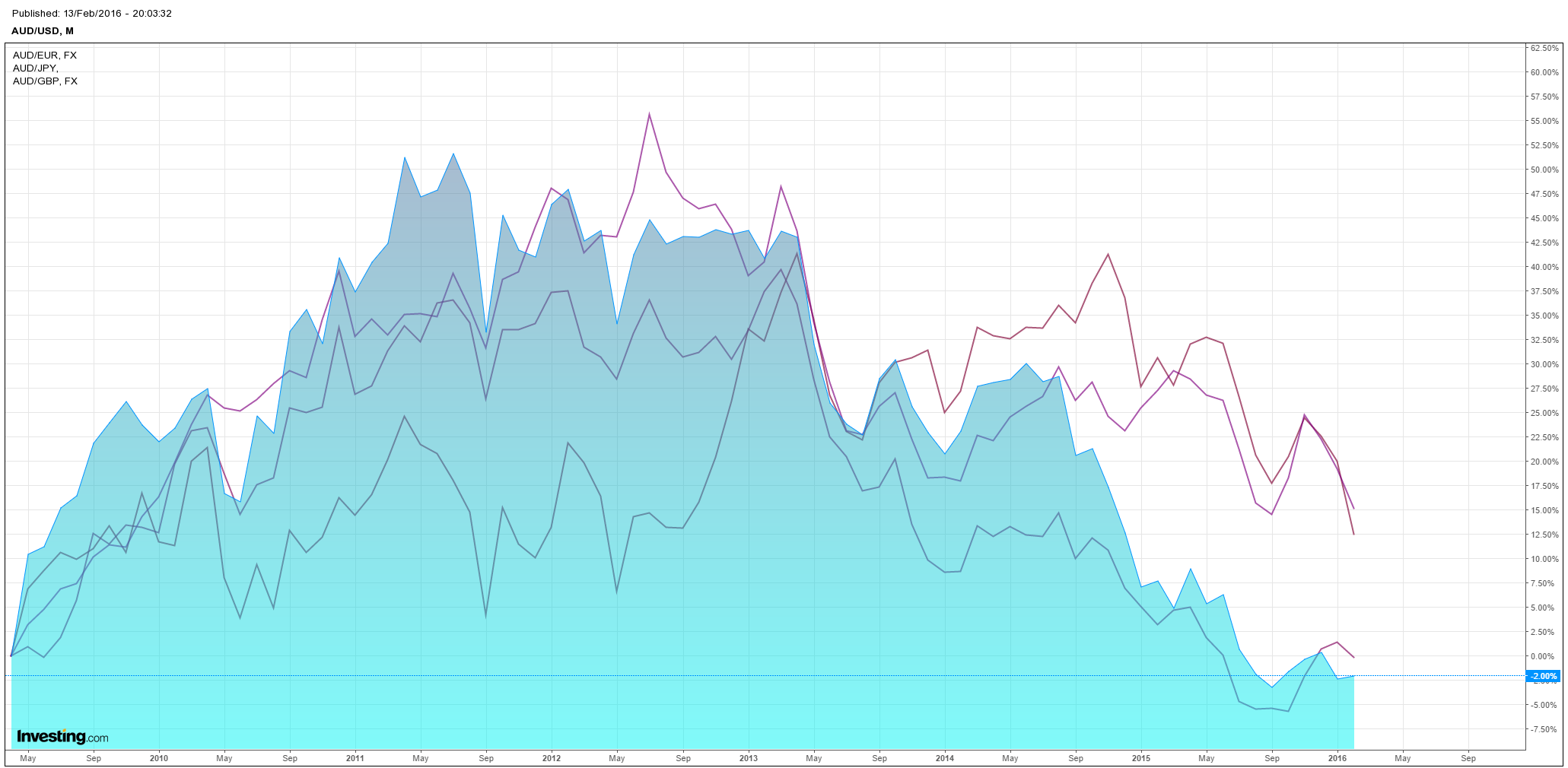

In terms of technicals, there’s really not much to go on other than an ongoing relatively steep downtrend. Against the major developed nation currencies, the Aussie remains weak across the board and making new lows in recent months against everything:

Advertisement

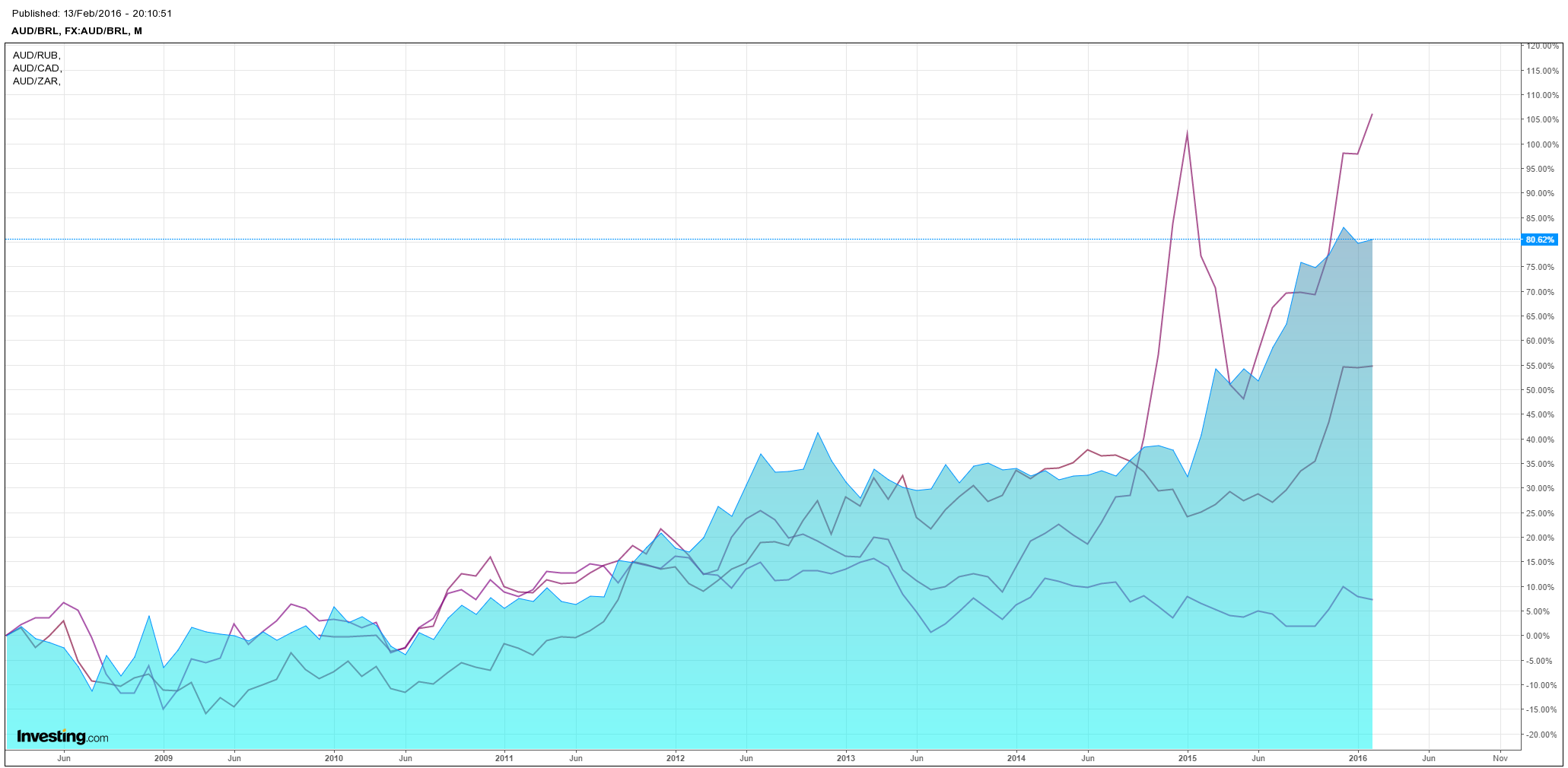

Against other commodity currencies we have out-performed, especially those oil-exposed:

But that is, by and large, to be expected given most are emerging markets. Strength versus the Canadian dollar is largely an oil-based phenomenon as well.

Advertisement

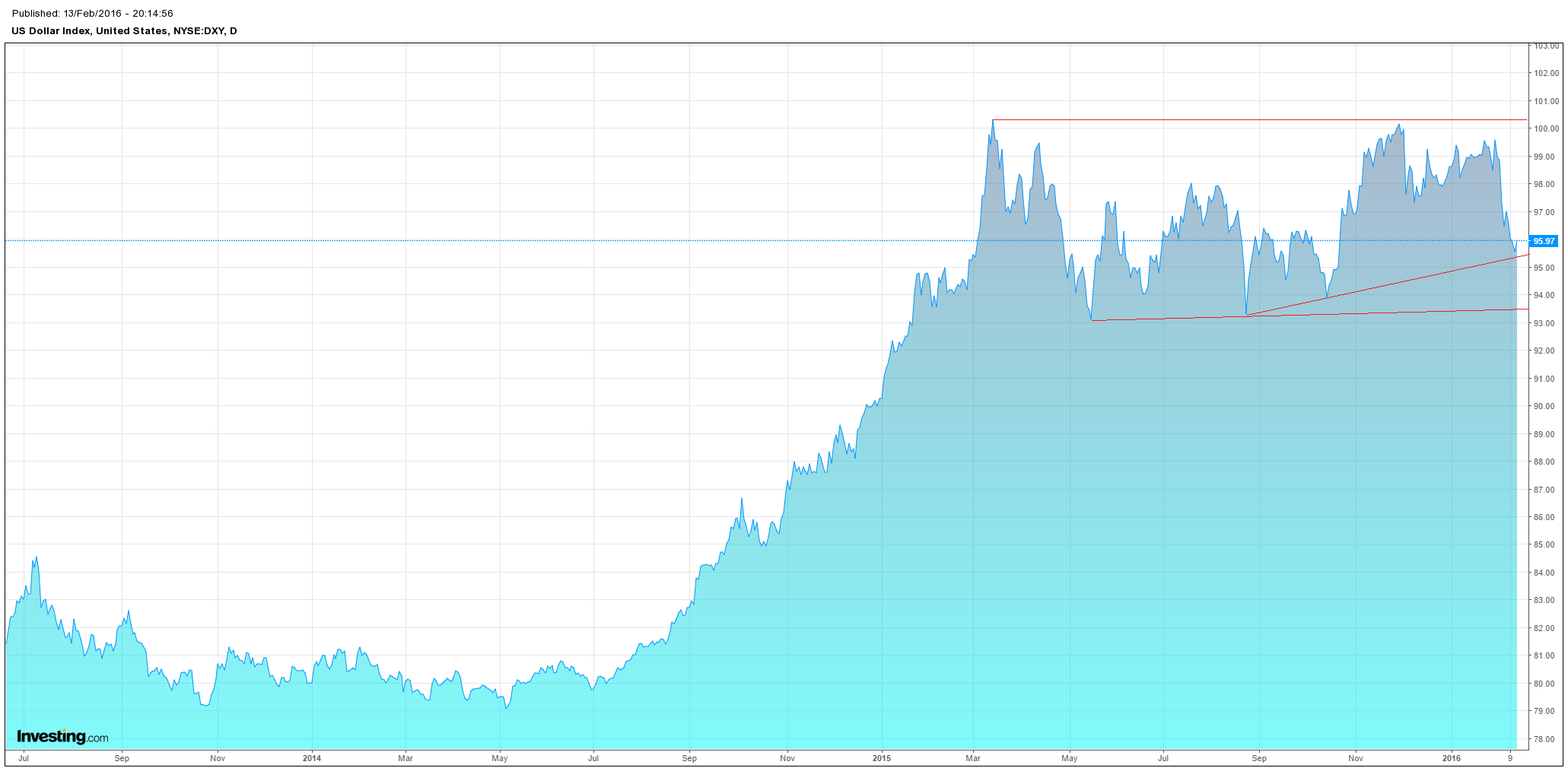

Our last driver, the US dollar, is perhaps the most fraught question when probing further Aussie weakness. The US dollar index has fallen back in recent weeks as its interest rate tightening cycle has eased up:

It retains a bullish chart though there are obvious reasons to think it could sell off further as its oil bust worsens and crowded trade unwinds. The Aussie has been trading in an inverse correlation with the index so that would push it up.

Advertisement

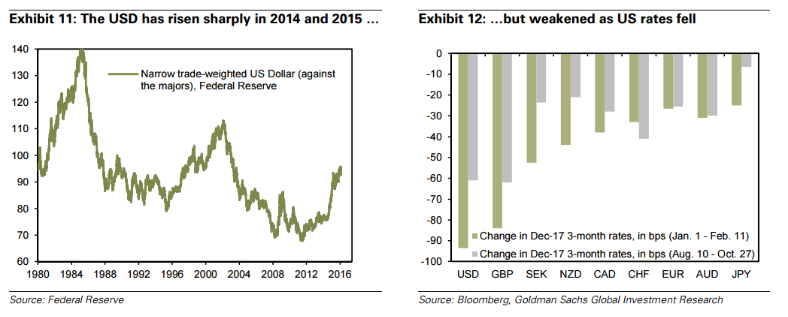

But even here I’m still fairly relaxed. Goldman has a “ten commandments” list for forex in 2016 that captures why:

Over the past month the market has put the USD under substantial pressure, and the DXY has fallen almost 4% since the end of January. The market has all but eliminated Fed rate hikes from the US curve for the rest of 2016, and the USD is lower versus both the EUR and the JPY as risk sentiment has suffered. This sell-off has stopped us out of our 2016 Top Trade recommendation to be long USD vs EUR and JPY.

In response to this uncertainty, last month we published a list of core ‘truths’, which we think will prevail and dictate market direction this year. We revisit and update these below following the BoJ’s January easing, and even more market turmoil in recent weeks.

1. Much more US outperformance than priced. Behind all the short-term worries lurks one important fact that is often overlooked. The Dollar has appreciated 26% versus the majors over the last two years, but US growth has stayed above trend. There is little doubt that net exports and inflation have suffered, but the resilience of the economy suggests that underlying momentum on both the growth and inflation fronts is better than priced, especially now that front-end interest rates have priced out so much tightening.

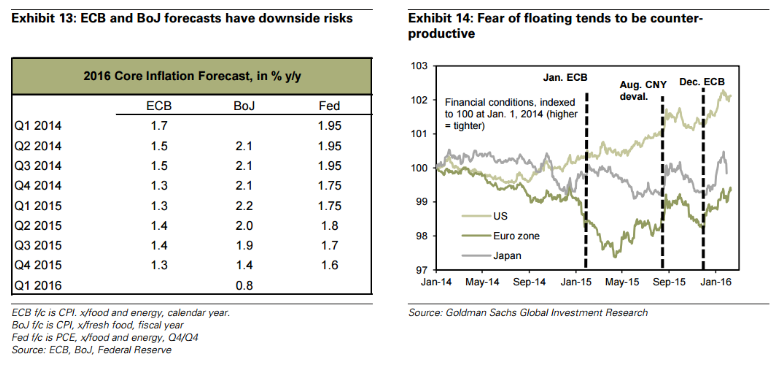

2. The ECB and BoJ can and will ease more. In the wake of recent disappointments, markets worry that the ECB and BoJ are reneging on their commitments to boost inflation, which has been weighing on risk. Both central banks have progressively cut their 2016 core CPI forecasts, fanning fears that they are ‘terming out’ their inflation targets. Indeed, our European Economics team forecasts core HICP at 1.0% this year, below the 1.3% ECB forecast, an illustration of the downside risk to an already low number. In our view, the January BoJ meeting demonstrated the BoJ’s ongoing commitment to its inflation target, even as the market has come to doubt the efficacy of its move to negative rates. For both the ECB and BoJ, we expect more stimulus – in addition to their recent easing steps – as opposed to reneging, which is the basis for our 12-month view of $/JPY at 130 and EUR/$ at 0.95.

3. G-3 central banks will get over their fear of floating. Fear of floating among the G-3 central banks has a price, which is that it destabilises risk, inadvertently tightening financial conditions. One example is the September FOMC, which exacerbated market anxiety over China with its focus on financial conditions. Another is the December ECB, where concern over excessive Euro weakening was reportedly one driver for not taking more aggressive action. Both times, equity market declines caused financial conditions to tighten, making efforts to manage G-3 exchange rates counterproductive. We expect the G-3 central banks to accept more Dollar strength as the lesser of two evils.

4. Low inflation for longer in the Euro area. Much of the discussion over low inflation in the Euro area revolves around global themes, including falling commodity prices and the slowdown in EM. But ongoing structural reforms in periphery countries mean that price and wage levels are likely to keep falling, imparting a deflationary bias to the region, which is distinct from global developments.

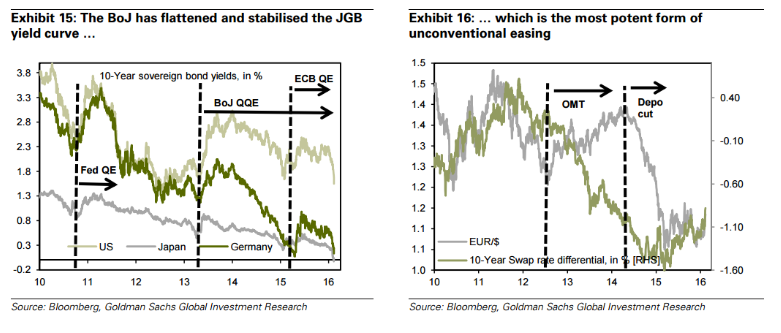

5. Negative interest rates are not a QE substitute. We estimate that a 10bp (surprise) deposit cut is worth two big figures in EUR/$, based on intra-day moves when surprise deposit cuts were announced (September 4, 2014 and October 22, 2015). This means that the bulk of the decline in EUR/$ stems from ECB balance sheet expansion and long-term interest differentials not front-end rates. Our forecast for EUR/$ down anticipates a shift in emphasis back to asset purchases from depo cuts. In the case of Japan, negative rates have augmented rather than substituted for existing QQE measures, and the impact has been to push JGB yields much lower. While the sell-off in risk assets has flattered JPY through interest rate differentials, we expect that ultimately this fall in the JGB curve will push JPY lower via portfolio rebalancing, as in point 6 below.

6. The BoJ is the ultimate QE warrior. Quantitative easing aims to boost growth via a portfolio shift out of safe-haven assets into risk assets. The QQE program has aggressively flattened and stabilised the JGB yield curve, encouraging that shift, such that $/JPY sees ‘autonomous’ moves up when risk appetite is good, for example in the summer of 2014 (the move from 102 to 109) and May 2015 (the move from 120 to 125). EUR/$ has not benefited from similar portfolio shifts because Bunds – the safe-haven asset in the Euro are – have been too volatile. And, as above, in Japan negative rates have not been introduced as a substitute for further QE, but as an augmentation.

7. The Dollar is a ‘risk-on’ safe-haven currency. The correlation of the Dollar with risk has flipped from negative to positive in recent years. This switch reflects rate differentials, rather than a loss of safe-haven status. Negative growth shocks, real or perceived, cause markets to price out monetary tightening in the US, such that rate differentials move against the Dollar. The positive correlation of USD with risk is therefore really a reflection of US cyclical outperformance.

8. Near-term pain, long-term gain for USD from low oil. Falling oil prices have a negative fall-out on economic activity in the short run, weighing on the Dollar by way of rate differentials. But the US remains a net oil importer, so that low for long in oil prices is fundamentally a Dollar positive, once near-term effects drop out. By way of illustration, it was the oil super cycle that derailed the Dollar-positive impulse from rising rate differentials in 2004-08.

9. China’s balance of payments is under control. There is a lot of anxiety that the pickup in capital outflows represents a run on the RMB, making a large devaluation all but inevitable. However, a key reason that outflows were so large in 2015 was that August and December saw the RMB fix weaker, which caused (heavily expectation-based) outflows to pick up. With a current account surplus of perhaps as much as US$400bn this year, China’s balance of payments can absorb a sizeable level of outflows before reserve drawdowns become necessary.

10. It is not in China’s interest to destabilise the world. China is a net exporter, i.e., it depends more than other countries on sound global growth. It is therefore hardly in China’s interest to unsettle markets and derail the world economy. Recent developments most likely point to a greater desire to see flexibility in the exchange rate and a closer link to fundamentals (which includes a shift in focus to a tradeweighted exchange rate), rather than unilateral devaluation.

The first eight points make perfect sense but not the last two. Self-evidently, China is not in control of its balance of payments. At least not yet. And it is not likely to get it. Chinese yuan weakness is the result of its economic weakness and the outflow of capital will therefore continue. Thus authorities are responding to yuan falls not driving them. They may want a lower yuan but not if it blows up their banks which is possible with uncontrolled capital flight. So, like most other things in China, they’ll aim for a glide slope in the currency knowing that they can’t prevent its devaluation. That is a big positive for the US dollar and a big negative for the Aussie given it hurts the competitiveness of every commodity producer on earth.

Advertisement

And this last point is the one that matters most. Even if the US dollar does fall for a period and adds a monetary tailwind to commodity prices and currencies, it is still pushing against the fundamental commodity price weakness driven by falling Chinese demand growth and excess supply. The latter should still win in the end and the Aussie continue to fall, even if more slowly than it might have otherwise.

Given MB still sees this oversupply as the cracked key-stone in the global business cycle arch, and expects that it is large and pervasive enough that rationalisation can only come through a global scale bankruptcy for producers sovereign and private, as well as the outlook that that poses for local growth and interest rates, our forecasts of 60 cents this year and 45 cents as the cycle low remain unchanged.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.