A couple of IB takes on the ASX profit season are worth a look today. UBS is cheerful:

Key Takeaways

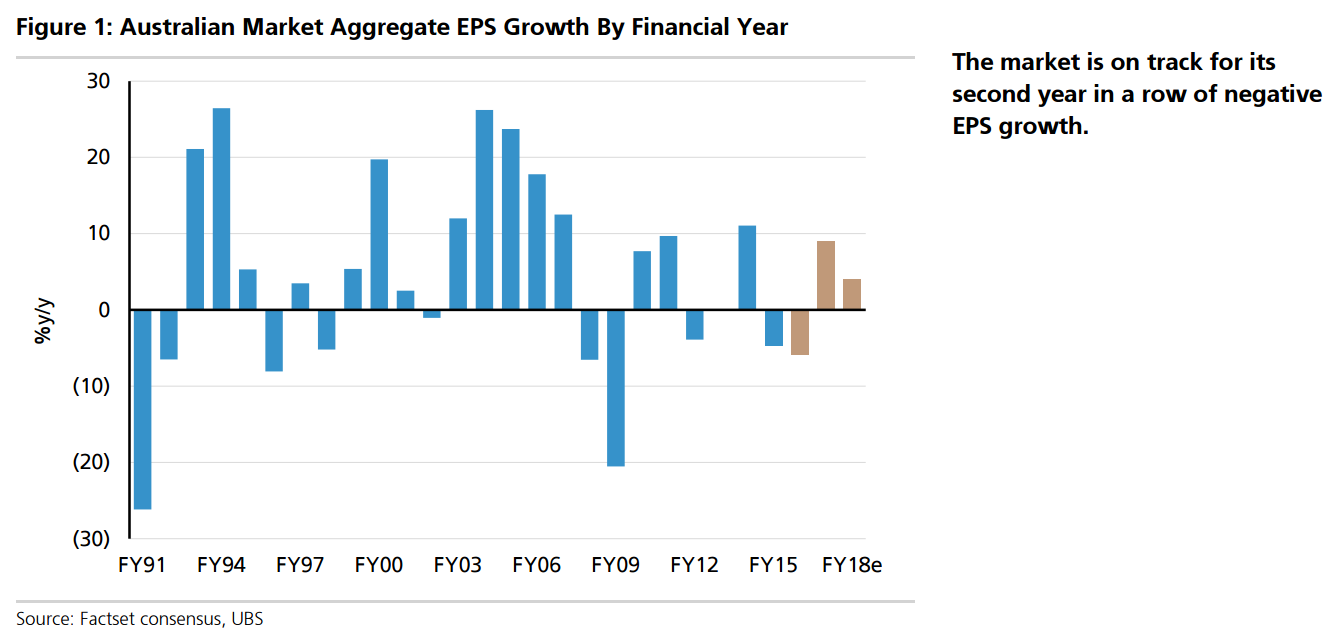

More beats than misses and net positive guidance, but FY16 edged very slightly down. Share price bounces confirm ‘better than feared’ outcomes. EPS revisions less dramatic than share price moves, but some significant upgrades and downgrades at the stock level. Market earnings growth still negative, albeit moderate growth (+4%) exresources. Big caps are dragging on earnings growth. Median stock is doing better.

Sector Thematics

Reasonably good performance from stocks leveraged to the domestic economy particularly housing and consumer related. Small caps performance was relatively similar to large caps with EPS revisions relatively flat but share prices reactions tilted to the positive. High P/E large cap stocks on average delivered. Value stocks had a mixed experience but we note some dramatic jumps on better than feared results. There was mixed performance from US$/Foreign currency earners. Reasonably pleasing performance from the big banks but weaker performance from regionals.

Earnings Better Than feared

But Market Still Nervous On Macro Risks Overall reporting season could be classed as ‘better than feared’. While estimates have edged down a touch, reactions suggest this is better than the market feared. Market weakness this month can mostly be attributed to global macro concerns – in particular concerns around the global banking sector although some jitters around the housing market entered the public discourse late in the month.

“Better than feared” is a relative term that tells you nothing except the level of anxiety in the sell side was high. We are in a profits recession and that is not good. Moreover, it results in this, from Credit Suisse:

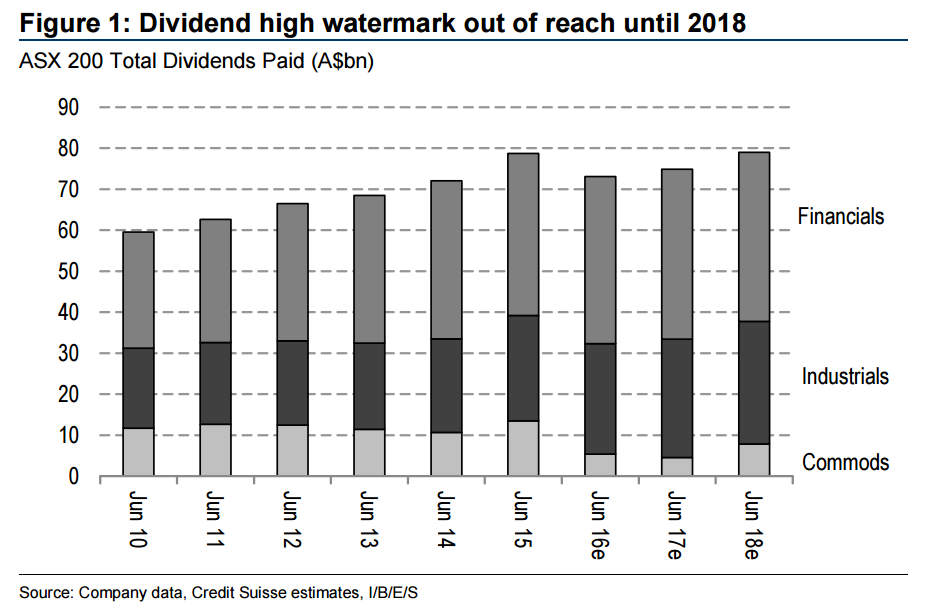

Bad for Selfies: The most recent reporting season was a period of large downward revisions to ASX 200 DPS forecasts. This was to the detriment of many income seeking investors in Australian equities for the yield. Meanwhile, analysts upgraded EPS and free cash-flow forecasts.

■ Scrapping the progressive dividend: Australia Inc.’s progressive dividend policy is being scrapped. Analysts are forecasting $A73bn of dividends to be paid in FY16. There was A$79b of dividends paid in FY15. Commodity companies account for the all of the expected decline in ASX 200 dividends.

■ Too early to end the restructuring program: The outlook for growth remains subdued. Sales forecasts continue to be dreary with little mild contraction forecast for this year and 4% expansion in 2017. Expectations are for an equally dreary EPS outlook. It is too early for Australia Inc. to call off the current restructuring program in place. We expect companies to continue to cuts costs, restrain capex and reposition businesses.

Advertisement

With yield now shrinking expect the ASX to continue to de-rate in the global context.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.