Chris Weston, Chief Market Strategist at IG Markets

It’s been a day of trauma for the equity bulls and for many the towel has been thrown in.

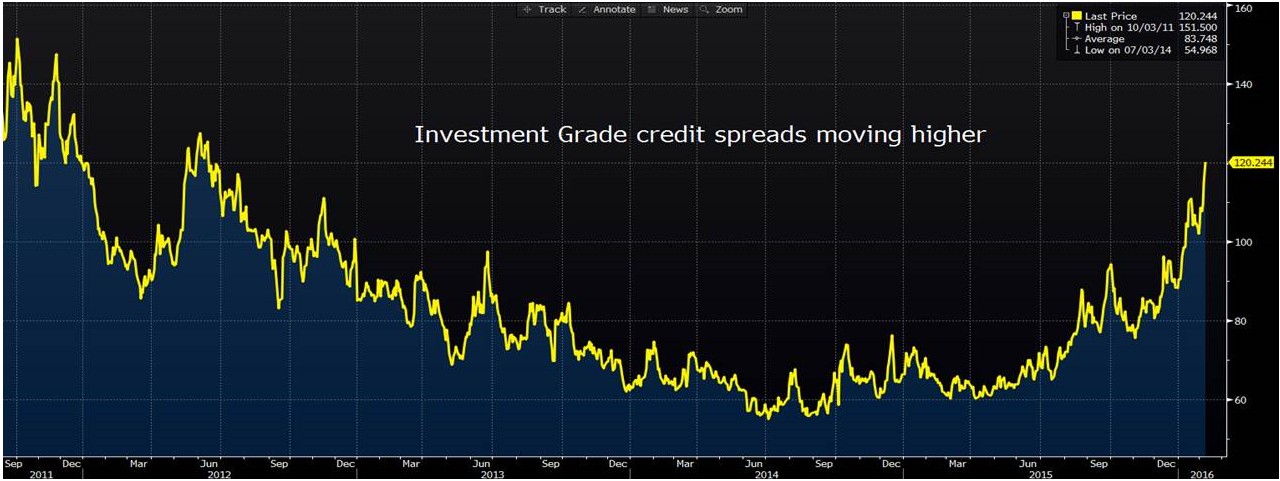

I suggested yesterday that the financial markets were at a key juncture, but the widening in credit spreads and the focus now on credit default swaps suggests that the pain is not going away anytime soon. There is huge demand for portfolio protection in all asset classes and it just doesn’t feel like we are going to see a major turn anytime soon. One can then do a sense check as to what will effectively turn this juggernaut of pain around and this is not a question that is readily answered.

The long-felt pain in the energy sector has now fully morphed into a banking crisis. Much has been made of the demand for credit default swaps (CDS) protecting against future default in the European banking space. Rightly so, when Deutsche has been sold off 58% from its 2015 high and left with a market capitalisation of €21 billion. Given they have €54 billion in bonds maturing over the next two years (much of this in the next two months) and much of their existing funds tied up as regularity capital, things don’t look hugely sustainable. The less focus on earnings numbers the better. One does suspect the market cap does reflect quite a bit of bad news.

Price action in Asia has reflected these concerns with Aussie banks getting smashed, despite not having anywhere near the same balance sheet duress as European banks. Aussie banks don’t rely on the long-end of the yield curve for margin expansion like US banks, but what we do know is the big four Australian banks will be raising up to A$100 billion of debt throughout the year, much of which will be issued offshore. With funding costs on the rise, this will affect net margins and presumably this will be passed onto the costs for business loans. So there will be an in impact on credit and wider economics.

There is a genuine concern that stress in asset markets will start affecting real economics, so let’s forget the US payrolls report, it is a lagging indicator. This period of sustained volatility and deterioration in credit will impact businesses and one has to be concerned about how many households are feeling this drawdown in the financial markets.

(Source Bloomberg)

The Nikkei has been well and truly savaged today, assisted by USD/JPY trading through ¥115.00 (low ¥114.43), the lowest since November 2014. The technical destruction in USD/JPY is there for all to see and we have seen a renewed barrage of currency jawboning from different Bank of Japan officials today. It is clear that strong buying in the Japanese government bond market is not going to drive the JPY weaker in times of extreme volatility, so negative rates have little bearing on markets. Keep in mind that the Japanese ten-year government bond has traded to a zero yield and is poised to go negative and JPY sellers are nowhere to be found. Talk of an emergency meeting from the BoJ is elevated, but what are they going to discuss? The organisation is losing credibility by the day and they can’t control the USD.

US futures have started to roll over, once again reflecting better selling of the Nikkei and ASX 200, after the open of their cash markets and the strong volume going through these markets. Our European equity calls have started to head lower and, despite a savage session yesterday (on huge volume), traders are staring at another negative start.

It must be said that if one is to look for markets that are oversold, then they would immediately turn to Europe. The market internals on the EU Stoxx 50 are about as crazy as you will ever see with just 4% and 2% of stocks above the 50-day and 200-day moving averages, respectively. 60% of stocks are trading at 4-week lows. The FTSE looks unconvinced, so the open could hold many clues and, if sentiment is the guide, then even the smallest of rallies on open will open the door for traders to get out of unwanted longs.

Keep an eye on European sovereign debt as well, as the main focus has been on credit spreads (high yield and now investment grade), but we have started to see Greek, Spanish, Italian and Portuguese yield moving higher. The Greek 10-year jumped 61 basis points yesterday and there will be focus on Greek reforms in this week’s Eurogroup meeting. The last thing traders need to now is for Greece to come back on the radar.

Ahead of the open we are calling the FTSE AT 5672 -17, DAX 8912 -67, CAC 4050 -16