Chris Weston, Chief Market Strategist at IG Markets

There seems little doubt that we have reached a key juncture for the world’s financial markets and if confusion wasn’t at fever pitch two weeks ago then things are even worse now. We always stated that when the Federal Reserve raised rates it would only give more certainty to when uncertainty starts, and this is clearly playing out.

With all that’s going on, it’s worth taking a look at the various market cross-currents to make a more educated view on where we are.

Will we see a recession in the US and other developed nations?

There is little doubt this is the number one question being asked right now. A solid US payrolls has done little to dent this view. In fact, the spike in the USD only exasperated the implied probability, although traders are certainly acting with calmer heads today; equities and equity futures have found better buying on open.

The market has been fixated on the US yield curve, which at 110 basis points (two- versus ten-year US treasuries) is the flattest since early 2008. They are focused on a widening of credit spreads (see Bloomberg chart below), which again have blown out to the widest spread relative to US treasuries since 2008. Credit default swaps spreads, specifically in the banking space, have also been moving aggressively. When blended with volatility in the equity markets, tighter lending standards and USD strength, we can get a sense of overall financial conditions. As things stand, the current stress in asset markets is akin to around 100 basis points of tightening on the US economy. The strong fear is this stress – that is clearly being felt in the financial markets – will start to filter through to Main Street.

Are the moves overdone?

- S&P 500 short interest as a percentage of market cap is at 2.6%, which is hugely elevated relative to history.

- Institutional US equity net futures positions are at a record low – equities are just so unloved.

- US equity outflows have amounted to $40 billion in 2016 and, looking further afield, outflows from emerging markets have materialised for 14 straight weeks.

- 10% of German stocks are trading above their 50-, 100-, and 200-day moving average. The DAX itself is trading at the lowest level since December 2014.

- The Fed funds future market is now pricing in a 60% chance of one hike in 2016 and 38 basis points (or 0.38%) of tightening by December 2017. Clearly the Fed is not going to hike four times this year, but there are so many trading opportunities here for those who think we won’t see a recession.

The wash-up for those who follow money flow is to absolutely stay cautious for now. These are not the sort of theme’s you see when we are due to see a near-term turn in the markets.

One still needs to look at the positives to make a case that credit and the US yield curve are pricing in too dire a situation:

- US consumer credit grew $21.3 billion in December

- US vehicle sales recovered in January

- The forward-looking new orders sub-component of the ISM manufacturing report increased

- The Atlanta Q1 GDP is tracking at 2.1%, although this is likely to be revised lower in the coming weeks. Still a recession seems unlikely.

Janet Yellen to provide clarity

All eyes will be on Janet Yellen’s semi-annual testimony to Congress this week and there will be much focus on her vision around the impact tighter financial conditions have had on economics. It should give us some insight as to whether market pricing has just got way too bearish, although the more cynical traders will detail that no central bank and only a handful of economists have ever correctly predicted a recession a year out. One suspects Yellen will be dovish, but will we get to hear that the world is about to collapse, which seems to be priced into markets? This seems highly unlikely and we may see some selling of fed funds futures and longer-term US treasuries, and ultimately buying of USDs.

Assets to have on the radar week:

- As goes the USD, as goes risks appetite. Expect outperformance from European markets if EUR/USD does push lower.

- EUR/USD reached the measured move and triangle target of $1.1250 and I wouldn’t be surprised to see a move down into the $1.1083 (the 38.2% retracement recent rally from $1.0810). EUR/JPY looks like a buy for a move into ¥131.80 (top of the channel), with a stop below ¥129.90.

- Oil: It’s hard to look past the impact oil is having on markets and another collapse in price would subtract from risk appetite.

- The S&P 500 needs to hold the 1873-to-1870 area (as highlighted by the blue rectangle). If long, I would be using this as an area for stops.

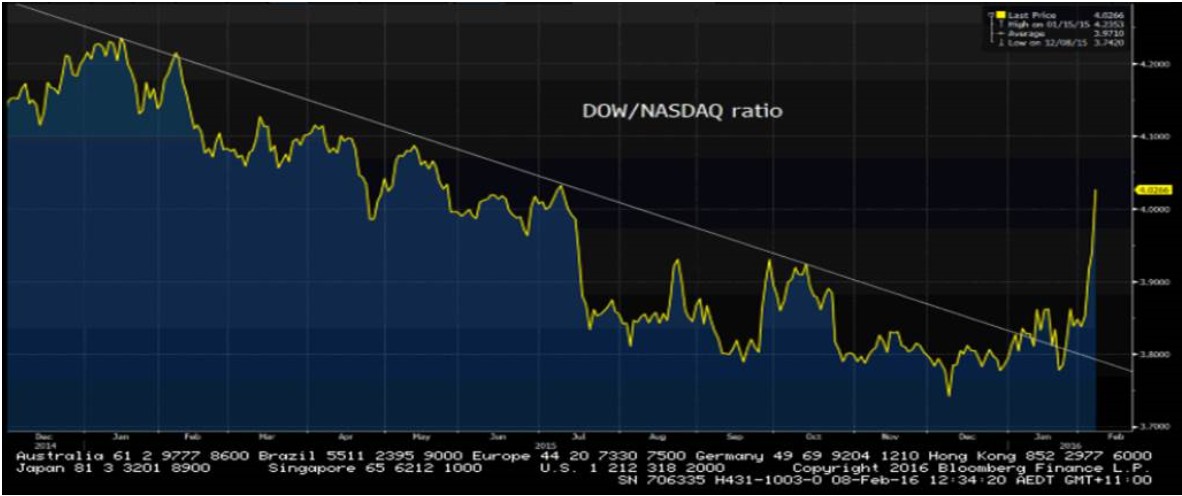

- Long Dow, short Nasdaq 100 has been a brilliant trade and, if we look at this from a ratio perspective, one could say the Dow has had it too good of late. I would be taking profits on this trade and, if we do see a turn in risk this week, then I would expect the Nasdaq 100 to outperform.

- Gold is technically overcooked and I’ll be watching for a move into former trend support at $1151. If gold can hold that level, we could see a stronger move into $1200.

- ASX 200: A big week for earnings, notably CBA and RIO. The index seems to have found a new range of 4800 to 5000.