Angus Nicholson for Chris Weston, Chief Market Strategist at IG Markets

Superbowl and the Year of the Monkey will be ushered in on Sunday, but fans of FX volatility will also be welcoming important US and Chinese economic releases over the weekend. US Non-Farm Payrolls (NFP) will be released this evening (00:30 AEDT) and investors will be keenly watching whether the deterioration in a range of other US data has spilled over to the job numbers. China’s FX reserves numbers (out on Sunday) have gained a new importance as global investors play a game called “Guess the Threshold (of FX reserves where the PBOC would decide to devalue the currency)”. Given these two key data points, what outcomes would result in maximum volatility? A big miss on the NFP numbers (150,000 or less) would see a further dive in the US dollar, killing expectations of any further rate hikes by the Fed. If China’s FX reserves decline by USD 100 billion or more, expect short interest on the CNH and HKD to rally strongly. USD declines, in the event of a NFP miss, also put further upward pressure on the CNY real exchange rate in turn making the case for a CNY devaluation more pressing. Exciting times.

The CNY midpoint was strengthened by 0.16% again today, marking two days in a row. This looks like some of the PBOC’s well-worn tactics of shaji xiahou (“kill the chicken to scare the monkey”) as they try to shake out some of the shorts ahead of the FX reserves data release. It is hard to believe that FX reserves would decline by significantly less than USD 100 billion given the PBOC’s heavy intervention in quelling the differential between the onshore and offshore CNY in January.

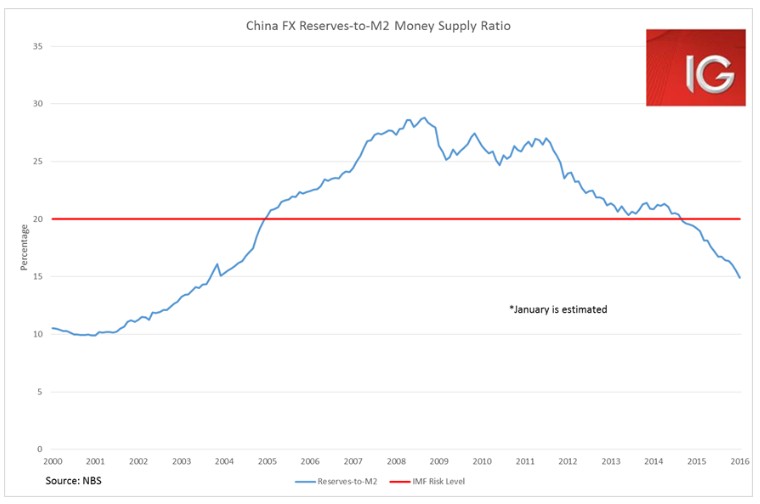

Most significantly, I estimate that a decline of USD 100 billion would take China’s FX reserves-to-M2 money supply ratio to 14.9%, its lowest level since 2003 and well below the IMF’s 20% “level of prudence”. This date has particular symbolism, as it was in 2004 when the PBOC first allowed cross-border trade in the CNY and the Great CNY Carry Trade first began in earnest. In short, January could see this ratio show a total reversal of the 2004-2014 CNY carry trade (R.I.P.).

However, this major data point is released at the beginning of Chinese New Year (7 February) holiday, how will this affect currency markets? Our dealers are reporting that CNH and HKD will still be traded next week, but the actual currency delivery will not occur until 16 February. While the currency pairs will still be traded, the lack of holiday induced liquidity could see quite dramatic volatility in the pairs. Also one wonders whether the PBOC will take a holiday on intervention, which could see the CNH dropping to new lows. One thing is for sure, hongbaos with Non-CNY denominated currency will be going down a treat this Spring Festival.

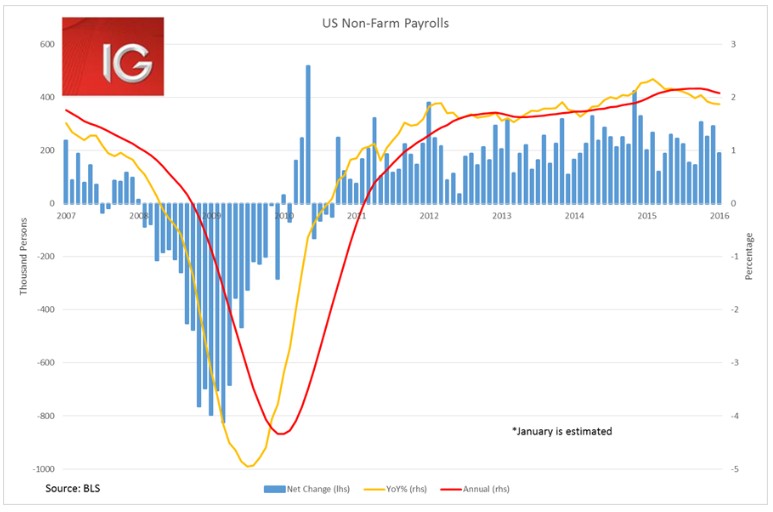

NFP

Current expectations are for the NFP to come in at 190,000 this evening (00:30 AEDT), and the strong performance of the ADP employment data this week does bode well for the release. However, the January PMIs have all seen the employment component weaken dramatically and seems to have been a major contributor to the reassessment of the likely rate hiking cycle.

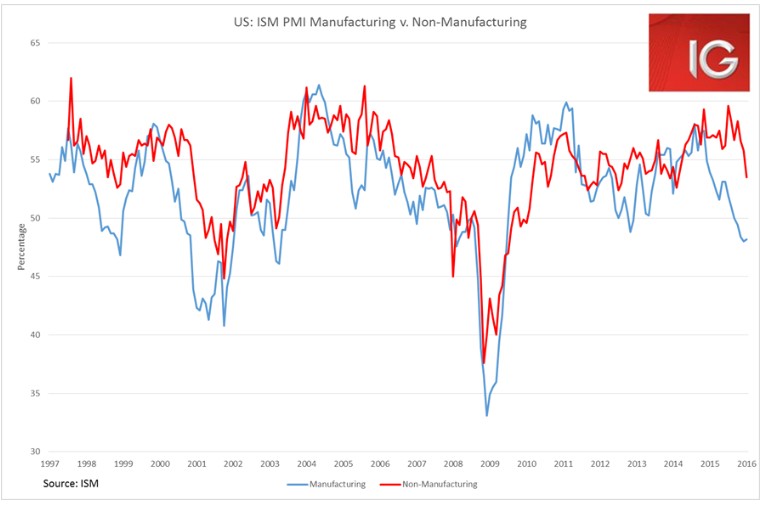

The ISM Manufacturing and Non-Manufacturing PMIs provide a great visualisation of the current predicament in the US. When both PMIs have headed into contractionary territory, the US has had a recession, as in 2001 and 2008. Yet, in 1998 the manufacturing PMI crashed into contractionary territory while the non-manufacturing PMI held firm above 50 and the economy avoided a recession. Indeed, there are compelling similarities with the current macro environment and that of 1998 – EM crisis, a rally in the US dollar around a rate-hiking cycle. The low point for the manufacturing PMI in 1998 was 46.8, while currently it is holding at 48.2. The big macro question this year will be whether US domestic demand can continue to outweigh the terrible external demand situation.