From Russell Clarke, Chief Investment Officer, Horseman Capital (via Zero Hedge):

My wife and I went see to the “The Big Short” the other day. It was certainly very amusing, and explained difficult financial concepts well. I will put it up there in my top three finance based films, along with “Trading Places” and “Margin Call”. I found Margin Call to be the least appreciated of these films, and yet for me most closely matches up to life in an investment bank in the 21st century.

For those that have not seen it, the film centres on a junior risk analyst, who discovers that the potential losses on the bank’s holding of mortgage assets were larger than its market capitalisation. He immediately informs his colleagues, who then pass it onto senior management. One of the recurring themes of the movie, is that the junior low paid staff are all maths and excel spreadsheet gurus, and the upper management are luddites. The junior risk analyst shows his excel model to management, and is constantly told “You know I don’t like these spreadsheets, just tell me what’s going on”. The analyst is eventually introduced to the Chairman of the Board, who asks him to “please, speak as you might to a young child. Or a golden retriever. It wasn’t brains that brought me here; I assure you that.”

If you were unfamiliar with the world of finance, you would think this grossly unfair. The brainboxes of the world toil endlessly, while their know-nothing bosses take home the big bucks. However, I think this is wrong. As the Chairman of the Board elaborates, the reason he earns the big bucks is, “I’m here for one reason and one reason alone. I’m here to guess what the music might do a week, a month, a year from now. That’s it. Nothing more.” The music in this case would be market prices.

The crux of the matter is that anyone telling you what the market is doing now, what the value of something is now, is providing you a freely available commodity; even if, in the cases of some derivative products, you need to be a rocket scientist to be able to give a valuation today. The real value add in markets is to be able to see what future values might be; that is to live in the future, not in the present.

I spend most of my time, while looking at current prices, thinking about and trying to live six months to one year in the future. Thinking about what will be the reaction to what is happening now, and then thinking about what that means future prices might look like. Generally that has worked well for me.

What I can see now is that US growth is slowing, and that the market is likely to price in reduced monetary tightening.

This should lead to a weaker dollar. This makes shorting Europe and Japan very appealing. Theoretically, this should make commodities and emerging markets (‘EM’) attractive, particularly if you are of the view that US dollar strength is the reason emerging markets and commodities have been so weak. However, I think we have chronic oversupply of commodities, and real financial issues in China that cannot be resolved easily. This makes commodity related areas very unattractive, despite the prospect of renewed monetary easing by the Federal Reserve. Furthermore, the reaction to reduced tightening by the Federal Reserve, would almost certainly be more easing by every other central bank in the world. But as we have seen recently with both the ECB and BOJ, monetary activism is not always effective.

I also worry about the prospects of a trade war, as populism becomes the new normal in politics globally.The future for me is now more uncertain than at any time I can remember. Or to fully quote the Chairman of the Board from Margin Call, “I’m here to guess what the music might do a week, a month, a year from now. That’s it. Nothing more. And standing here tonight, I’m afraid that I don’t hear – a – thing. Just… silence.”

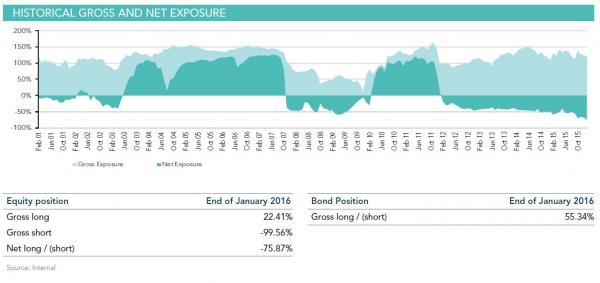

Your fund remains long bonds, short equities.

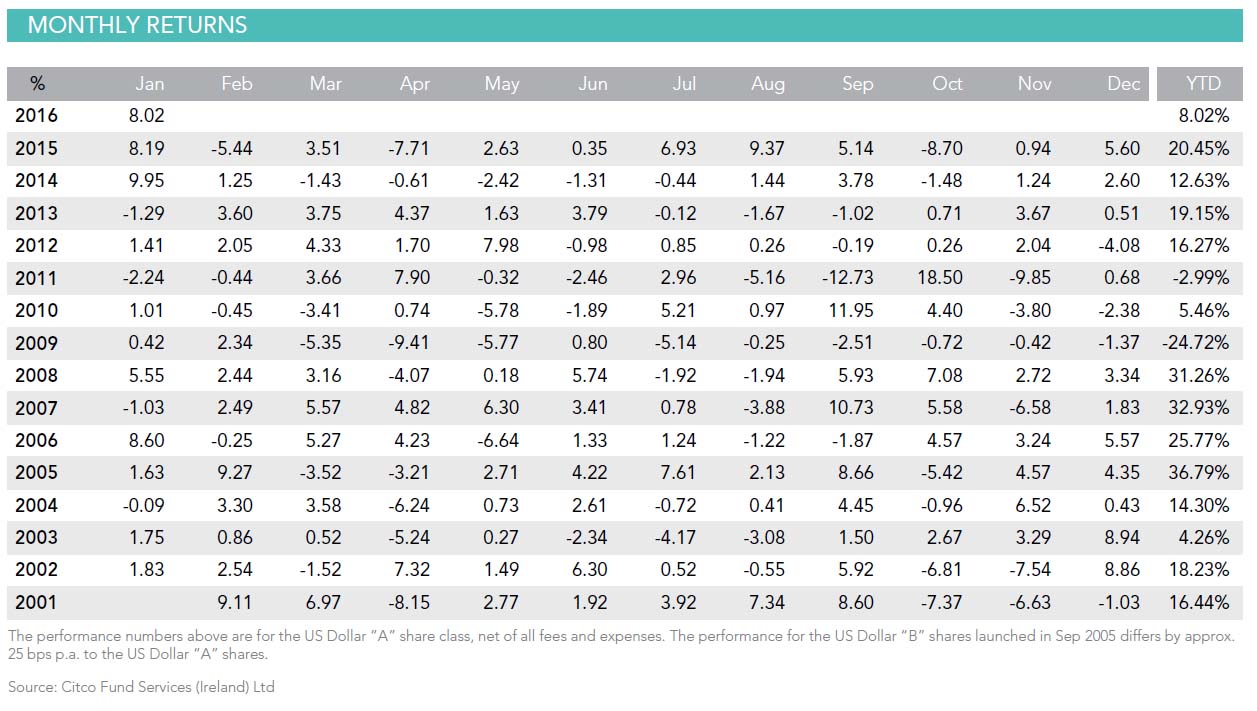

I could not have put that better myself. So how has Horseman Capital been traveling?

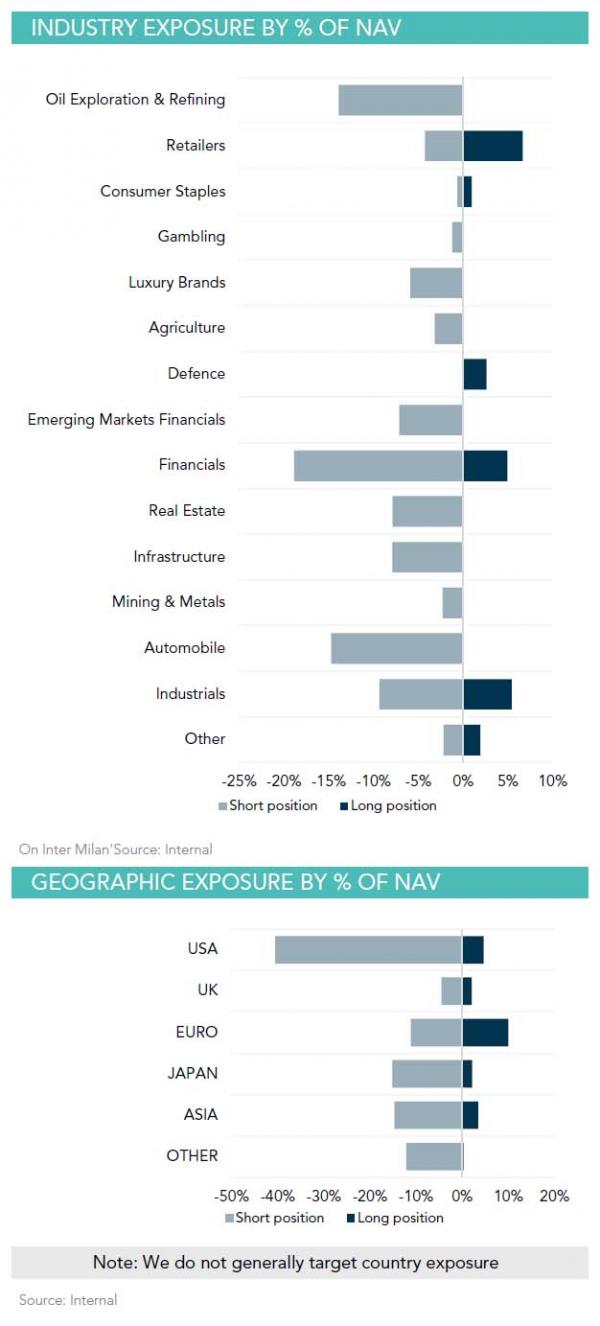

Nicely. Where is it’s money?

And how short is it?

Real short.