Markets saw a big bounce (and then reversal…) today as the Bank of Japan unexpectedly announced they would cut their policy rate into negative territory. Concerns had been mounting that the BOJ were increasingly tapped out in their ability to ease monetary policy any further, and today’s 5-4 decision shows how bitter the divide between hawks and doves is on the BOJ. The announcement opens the door to sustained further easing by the BOJ throughout the year. Although the fact markets pared back this bounce soon after the announcement may in some respects reflect growing market concern that central banks are delving into a tit-for-tat currency devaluation war. And the grand macro-economic elephant in the room is what happens if China is forced into a major one-off devaluation in retaliation. Markets are unlikely to react well to a big CNY devaluation, and the further the ECB and the BOJ force their currencies down the more they push the PBOC to act themselves.

- Former PBOC advisor Yu Yongding mounted a very cogent argument for a free-float of the CNY overnight. His argument was that the Chinese economy currently has the resources to withstand a major one-off devaluation, “China is still running a large current-account surplus and a long-term capital-account surplus, and it has not fully liberalized its capital account; so the chances are good that the renminbi would not fall too far or for too long.” Investors should be watching very carefully as Chinese FX reserves approach the key USD 3 trillion level.

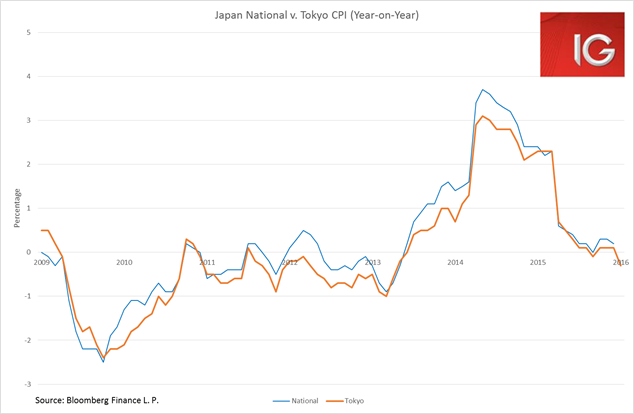

- The Japanese data released today underlined the case for the BOJ’s decision. Inflation has fallen away dramatically with Ex-Food and Energy CPI seeing its first monthly decline since January 2015. The leads the Tokyo CPI have provided for CPI in January, however, look incredibly weak with headline year-on-year Tokyo CPI hitting its lowest level since April 2013.

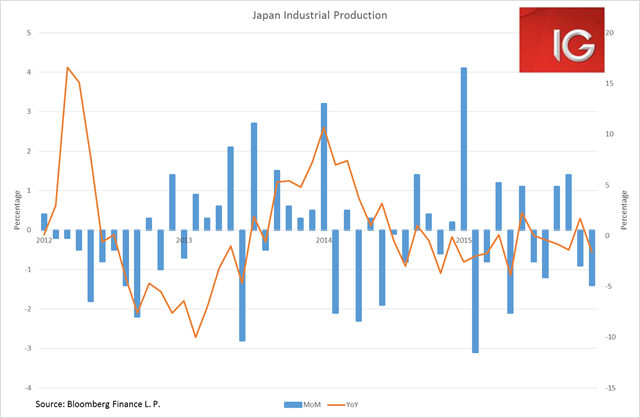

- Industrial production numbers were also very weak for December, seeing the biggest month-on-month drop since May 2015. The back-to-back monthly declines in Japanese IP are pointing to a weak Q4 GDP print.

- Given the BOJ’s actions today normally one would infer that Japanese stocks and long USD/JPY are the place to be in 2016. But the uncertainty around what Chinese Q1 data will look like and what decision the PBOC makes to halt the haemorrhaging of FX reserves are major strikes against those views. If you’re going to be long any equity market this year, the Nikkei and the Topix are certainly the better looking dirty shirts around. But I would be waiting until March/April when we could see a major selloff from a combination of weak Chinese Q1 GDP and/or CNY devaluation and that would be the bottom I would be buying at. And because of that in the very short term the yen could continue to see some weakness, but China concerns will undoubtedly see the JPY revisit the 115 handle or lower.

- ASX: The ASX has had a very volatile day with investors clearly very split in their views on the market. Of most concern for a lot of Aussie investors was the major underperformance by the healthcare sector. Healthcare and biotech stocks somewhat inexplicably suffered a major bout of selling in US markets overnight and that seems to have spilled over into our market. Even healthcare darlings, Blackmores and CSL, saw unusually heavy selling.