From the FOMC which hiked 25bps as expected:

Information received since the Federal Open Market Committee met in October suggests that economic activity has been expanding at a moderate pace. Household spending and business fixed investment have been increasing at solid rates in recent months, and the housing sector has improved further; however, net exports have been soft. A range of recent labor market indicators, including ongoing job gains and declining unemployment, shows further improvement and confirms that underutilization of labor resources has diminished appreciably since early this year. Inflation has continued to run below the Committee’s 2% longer-run objective, partly reflecting declines in energy prices and in prices of non-energy imports. Market-based measures of inflation compensation remain low; some survey-based measures of longer-term inflation expectations have edged down.

Read on MarketWatch: Fed enters new era of higher rates

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee currently expects that, with gradual adjustments in the stance of monetary policy, economic activity will continue to expand at a moderate pace and labor market indicators will continue to strengthen. Overall, taking into account domestic and international developments, the Committee sees the risks to the outlook for both economic activity and the labor market as balanced. Inflation is expected to rise to 2% over the medium term as the transitory effects of declines in energy and import prices dissipate and the labor market strengthens further. The Committee continues to monitor inflation developments closely.

The Committee judges that there has been considerable improvement in labor market conditions this year, and it is reasonably confident that inflation will rise, over the medium term, to its 2% objective. Given the economic outlook, and recognizing the time it takes for policy actions to affect future economic outcomes, the Committee decided to raise the target range for the federal funds rate to ¼% to ½%. The stance of monetary policy remains accommodative after this increase, thereby supporting further improvement in labor market conditions and a return to 2% inflation.In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its objectives of maximum employment and 2% inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments. In light of the current shortfall of inflation from 2%, the Committee will carefully monitor actual and expected progress toward its inflation goal. The Committee expects that economic conditions will evolve in a manner that will warrant only gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.

The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction, and it anticipates doing so until normalization of the level of the federal funds rate is well under way. This policy, by keeping the Committee’s holdings of longer-term securities at sizable levels, should help maintain accommodative financial conditions.

Voting for the FOMC monetary policy action were: Janet L. Yellen, Chair; William C. Dudley, Vice Chairman; Lael Brainard; Charles L. Evans; Stanley Fischer; Jeffrey M. Lacker; Dennis P. Lockhart; Jerome H. Powell; Daniel K. Tarullo; and John C. Williams.

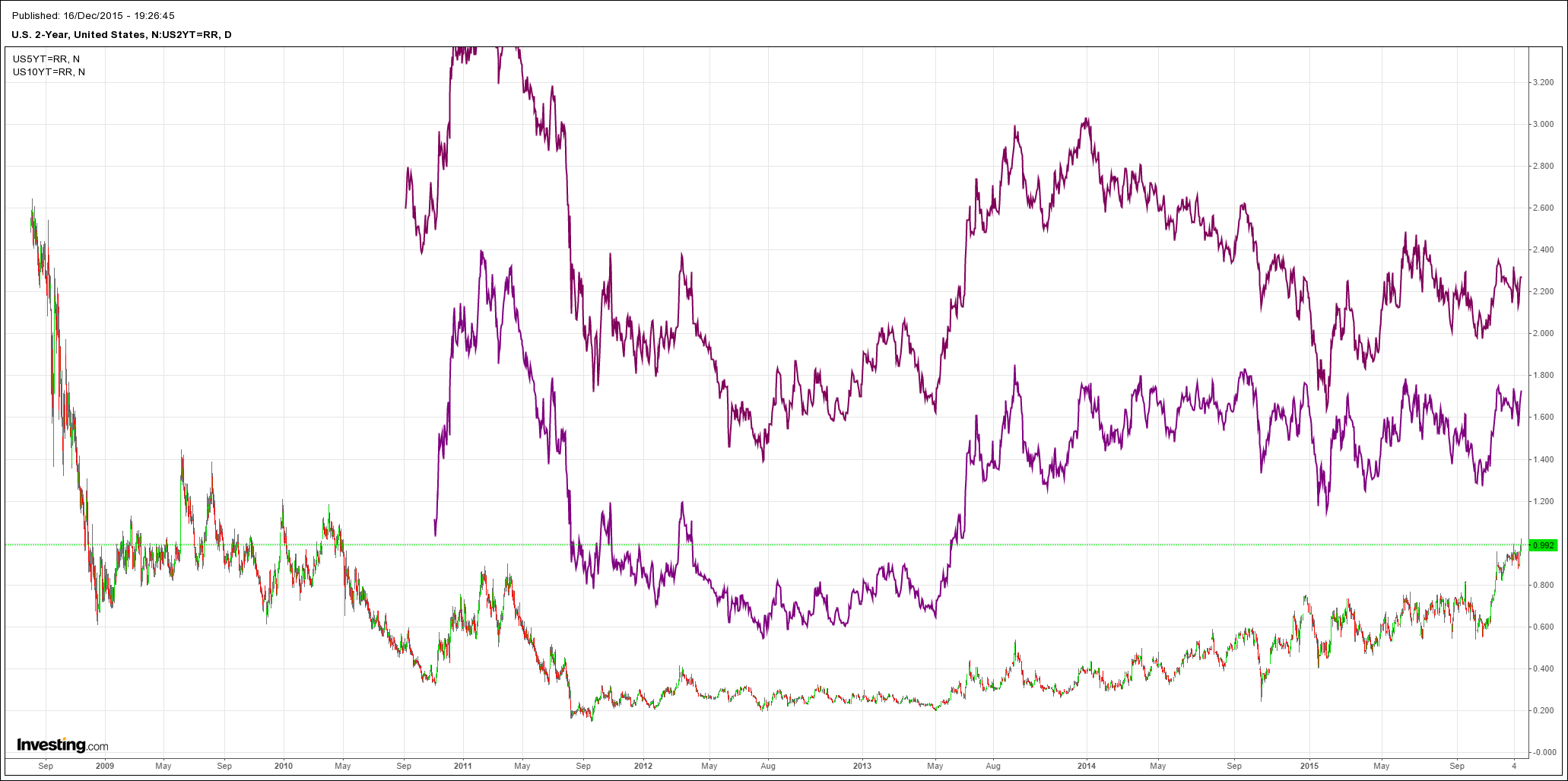

The big mover on the night was short end US yields which broke out to new highs:

Stocks also climbed 1% plus presumably on some kind of relief that we’re underway.

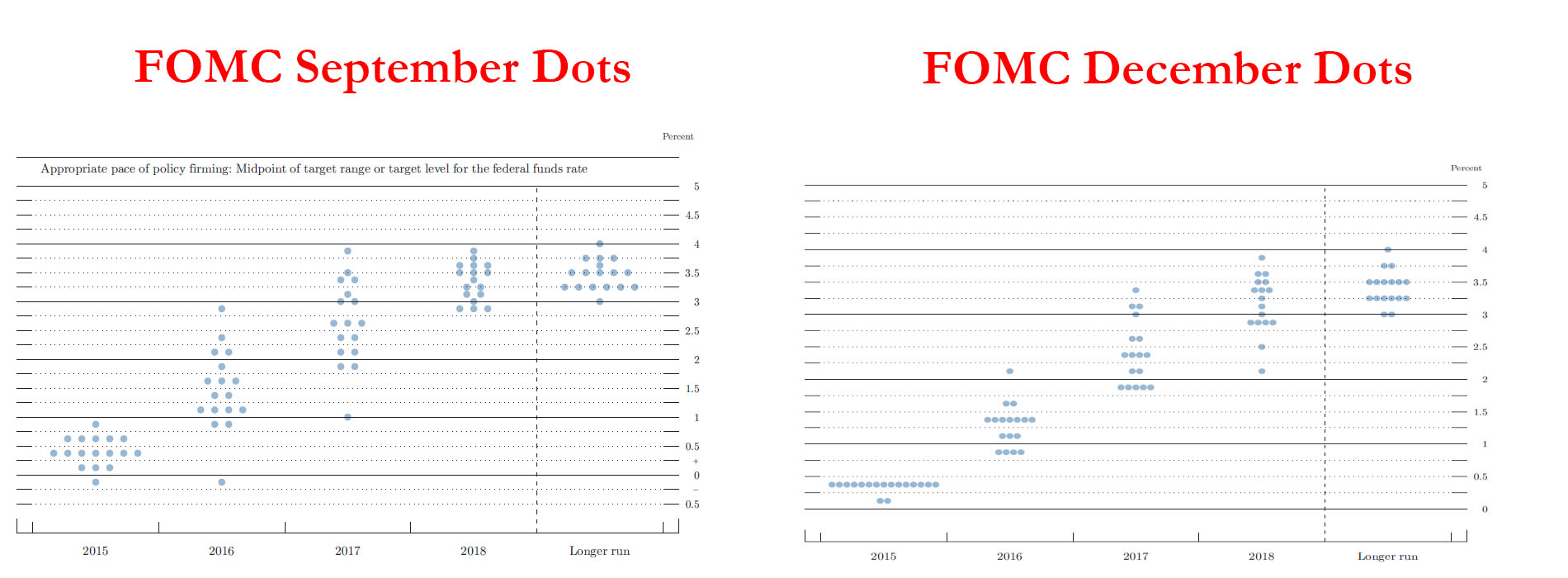

We shall now see how gradual is “gradual”. The December dot plots if anything got steeper:

I’m not sure what stocks are cheering. If the FOMC delivers anything like that schedule, which suggests four more hikes next year, then you can expect the global business cycle to end before we reach next Christmasas the Mining GFC turns nuclear.

But hey, Santa is here! So, say the investment banks.

Goldman:

BOTTOM LINE: The FOMC raised the funds rate to 0.25-0.50%, as widely expected. The post-meeting statement signaled a baseline of further funds rate increases, but expressed caution about inflation developments. The Summary of Economic Projections (SEP) showed an unchanged median funds rate for end-2016; median projections for 2017-18 declined moderately.

MAIN POINTS:

1. The FOMC raised its target rate for the federal funds rate at today’s meeting to a range of 0.25-0.50%, ending a seven-year period at 0-0.25%. The supplementary “implementation note” announced the following changes: an increase in the interest on excess reserves rate (IOER) to 0.50% (from 0.25%); an increase in the reverse repo (RRP) facility rate to 0.25% (from 0.05%); a removal of the cap on the RRP facility (it will be constrained only by the stock of Treasury securities held by the Fed; previously the Fed capped this program at $300bn); and an increase in the discount rate to 1.00% (from 0.75%).

2. The post-meeting statement signaled a baseline of further funds rate increases, but expressed caution about inflation developments. In particular, the statement said: “In light of the current shortfall of inflation from 2 percent, the Committee will carefully monitor actual and expected progress toward its inflation goal. The Committee expects that economic conditions will evolve in a manner that will warrant only gradual increases in the federal funds rate”—stressing the “gradual” message repeated in many public comments by Fed officials. The statement also added that “some” survey-based measures of longer-term inflation expectations “edged down”.

3. The statement also noted that the “stance of monetary policy remains accommodative”, even after the increase in the funds rate—a phrase the FOMC also used during the 2004 tightening process. Additionally, the statement said that the runoff of the Fed’s balance sheet is not likely to begin until “normalization of the federal funds rate is well under way”.

4. In the Summary of Economic Projections (SEP), participants made few changes to their forecasts for the economy and monetary policy. Fed officials raised their projections for GDP growth moderately for 2016 and lowered their projections for the unemployment rate. However, they also reduced the projection for core PCE inflation to 1.6% for end-2016 from 1.7% previously. The median projection for the funds rate at the end of 2016 was unchanged at 1.375%; the median funds rate projection for the longer run was also unchanged at 3.5%. Median projections for 2017-18 declined moderately.

And UBS:

Give the people what they want?

The FOMC met market expectations and hiked rates by 25 basis points, bringing the target range for the Fed funds effective to 25-50 basis points from 0-25 basis points. This move ended seven years of official rates at the zero bound. With the rate hike now behind us the market will shift to focus on three key questions: First, can the Fed make this rate hike “stick” using the tools they currently have. Second, how fast will the Fed keep moving? And, third, what will they do with the enlarged balance sheet?

We believe that the Fed will be able to enforce the target range although we expect it will require the Fed to ramp up the use of reverse repos, consistent with the announcement that repos would only be limited by the Fed’s Treasury holdings. We expect the Fed to hike rates by 25 basis points per quarter in 2016, in line with the “dot plot” provided by the Fed but still faster than is priced in by futures markets.

Data dependent or gradual? Both, if their forecasts are correct.

The statement suggested a committee with solidified views: risks are “balanced”, instead of “nearly balanced” and inflation is expected to rise “to”, not “toward”, two percent. Despite this confidence, as we expected, the Fed stressed that further hikes were likely to be gradual but are data dependent.

At the same time, they did not lower their already gradual expectations for 2016, keeping 100 basis points of tightening over the year as its median (and modal) rate. That said, there was a skew lower in the 2016 dots, but not one we see as being material given the composition of the voters in 2016.