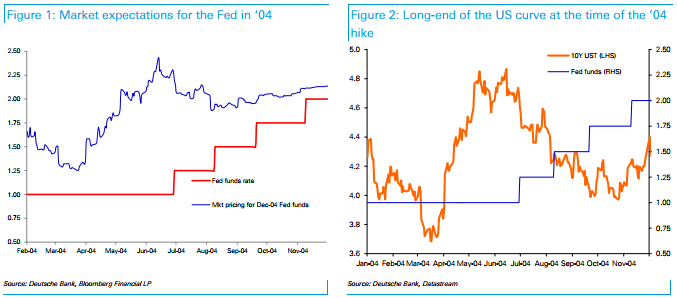

Summary: If the Fed hikes in December it will be the first upward move in the funds rate since June 2006 and the first start to a tightening cycle since June 2004. We look back to the June 2004 experience to see whether it offers any clues to how the AUD fixed income market might be impacted by the start of a Fed tightening cycle.

The front of the AUD curve doesn’t seem to have been greatly impacted, perhaps because the RBA was already well into its own tightening cycle. The long-end of the curve was much more directly impacted, though by the end of 2004 the direction of the 10Y ACGB and UST began to increasingly diverge as the shift in relative front-end pricing supported a sharp compression in the 10Y spread.

What inferences can we draw from this about the likely impact of a December Fed tightening on the AUD fixed income market? We think any impact on the front-end of the AUD curve will likely be relatively modest and short-lived. In saying this we do note that the RBA is in a very different state now than it was in 2004. It is possible that this means the Fed move will have a much greater impact.

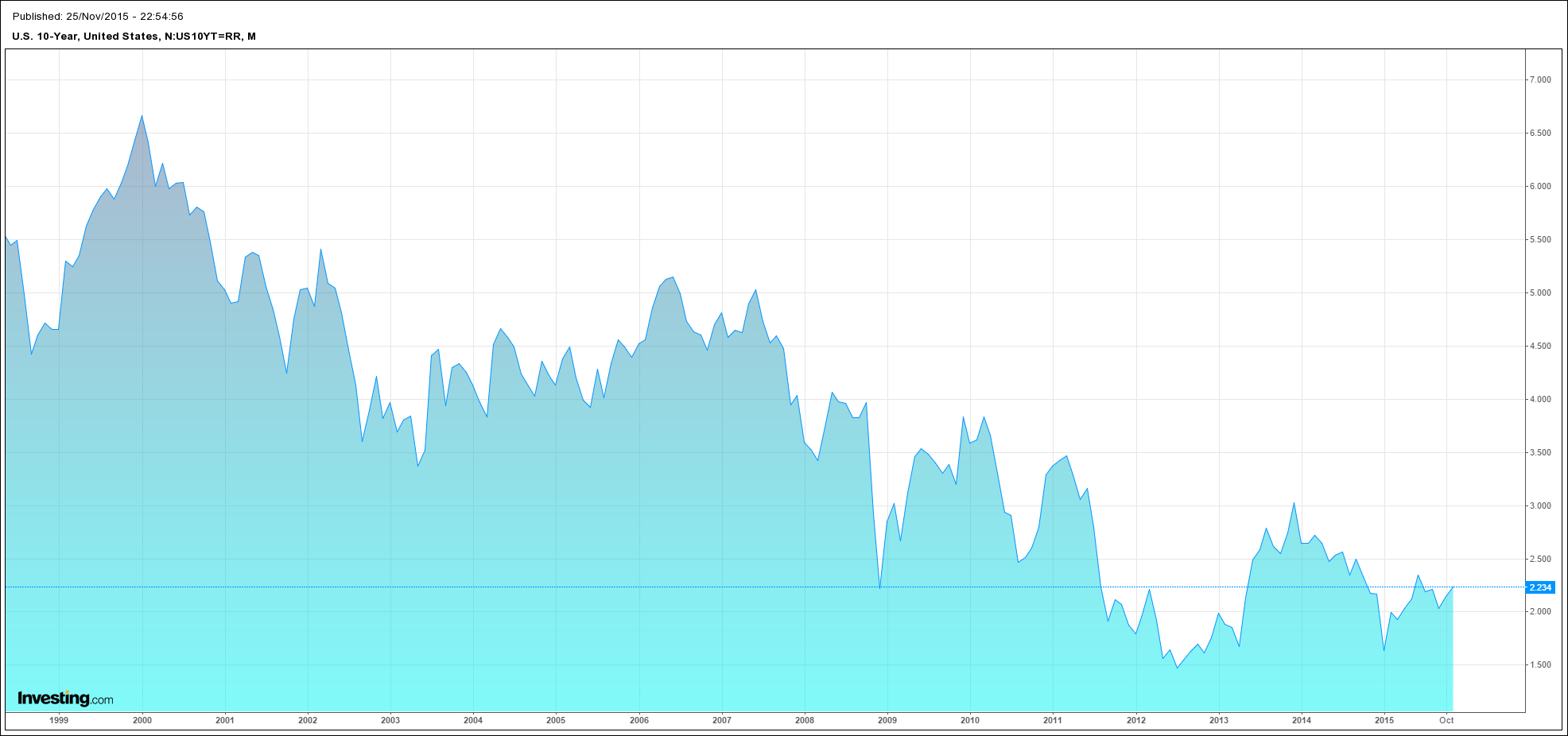

The long end of the curve will likely be impacted to a much greater extent, in our view. Can we conclude from the experience in 2004 that the 10Y UST will not sell-off in reaction to the Fed rate hike? We think a key difference between now and the start of the 2004 cycle is the slope of the US curve. By the time the Fed hiked in June 2004 the Fed funds/10Y slope was in excess of 350bp. This slope is currently more than 100bp flatter. Hence there is much less ‘protection’ for the long-end.

This makes us cautious about the duration outlook for the AUD bond market going into the FOMC’s December meeting. This caution is reinforced by concerns over market liquidity so close to the end of the year and uncertainty about what the Fed may say about the fate of its SOMA portfolio.

We are of the view, however, that any material sell-off in the 10Y ACGB on the back of a move in the 10Y UST will likely be a buying opportunity.

The world was indeed very different in 2004. Chimerican capital flows defied Fed tightening throughout the cycle and prevented any big sell off in long bonds despite rampaging oil prices and commodity inflation. What Greenspan described as the “bond market conundrum”. Eventually the 10 year priced about 180bps versus 425bps for the cash rate:

This time around it is difficult to know how the US long end will react. Will it price a recovery or a Fed mistake? Recent price action looks like it doesn’t know, either, not least because inflation is now chronically low and the hikes are clearly going to trigger commodity and emerging market turbulence.

Advertisement

One thing that is true is that if the 10 year does sell it will drag up the Aussie long end. That is a buying opportunity, sure, given more rate cuts will come but it’s no ‘buy and hold’. When the sovereign ratings is stripped trouble will hit the long end.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.