With the much-anticipated 16 December FOMC meeting around the corner, the 4 December US non-farm payrolls (NFP) is one of the most important remaining data points. The significance of recent NFP surprises in driving asset prices has been increasing since summer 2014 and is near historical highs.

We last observed this pattern of market behavior during the 2004-2006 Fed hiking cycle, suggesting this relationship exists due to market expectations for rate policy normalization.

During the previous hiking cycle the importance of NFP surprises rose ahead of the first hike and continued to rise until the end of the hiking cycle. Despite high anticipation for the next Fed hike, the importance of the employment report could remain elevated even after the initial liftoff. This relationship is particularly pronounced now as the Fed has adopted a data-dependent stance, and each NFP report will likely continue to play a key role in informing the path of subsequent Fed policy decisions.

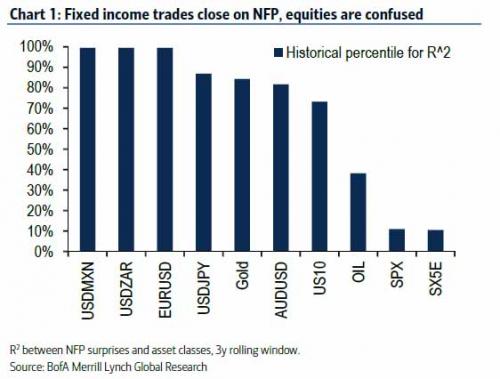

…In past hiking cycles, financial assets all became more correlated to NFP surprises heading into the initial hike as the market began anticipating Fed policy changes. Currently, the importance of NFP surprises is elevated for USD pairs and rates, but low for equities.

This is an important divergence from the previous hiking cycle when all three asset classes exhibited consistent reactions to NFP surprises. Historically, on positive surprise days, dollars and equities rallied while rates sold off.

One possible explanation for this divergence is that a December hike would take place at a time when global growth has been slowing rather than accelerating. World GDP YoY growth has been declining since 1Q14, whereas it was increasing during the 1999 and 2004 hikes. Another potential reason is the hike could disturb global imbalances from years of zero-interest rate policy. For these reasons, the risk of a policy mistake is greater than during previous hiking cycles.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.