S&P has released its new BICRA scores for countries and Australia come out OK:

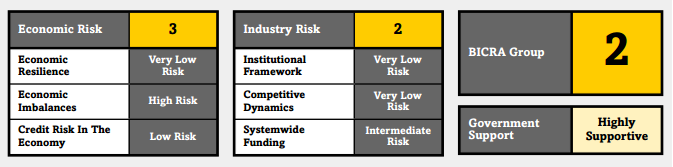

Standard & Poor’s Ratings Services classifies the banking sector of Australia (AAA/Stable/A-1+) in group ‘2’ under its Banking Industry Country Risk Assessment (BICRA). Some of the other countries in group ‘2’ are Canada, Germany, Hong Kong, Japan, Singapore, Sweden, and Switzerland. (See chart 1). Our bank criteria use our BICRA economic risk and industry risk scores to determine a bank’s anchor, the starting point in assigning an issuer credit rating. The anchor for banks operating only in Australia is ‘a-‘. Australia benefits from being a wealthy, open, and resilient economy that has performed relatively well during and following negative cycles and external shocks, including the global recession in 2009. We forecast that solid economic growth will continue over the short-to-medium term, even if slightly below trend given a muted recovery in non-mining business investment. We see potential risk of low interest rates contributing to higher house prices–as has occurred in recent years–adding vulnerability to the banking system although we believe that likely loan losses will remain very low by international standards. In our view, the economy is dependent on external savings to fund economic activity and growth Australia’s high current account deficits and external debt. We regard institutional and competitive environment for banks in Australia as low-risk. We believe the structure of the banking industry is supportive of industry stability–with a small number of strong retail and commercial banks dominating the industry. We believe that conservative and proactive regulatory and governance frameworks engender very low risk appetites and underpin banking system stability. Offsetting these positive elements, however, are the Australian banking system’s relatively low levels of customer deposits and its sizeable dependence on net external borrowings, despite some improvements in banks’ funding profile in recent years.

And the economic risk:

In our base case, we expect inflation-adjusted national average house price growth to slow down to about 4% in the next 12 months, broadly in line with the trend over the past three months. We consider that if–contrary to our base case expectations–the house prices in Australia continued to show strong growth, the banks operating in the country would face increased economic risks. Our base case expectations reflect the recent regulatory actions, including the increased capital requirements for the Australian major banks, clear direction to the banks to “appropriately” price for risk taken when underwriting investor mortgages, more stringent serviceability tests, and a soft 10% limit on investor mortgage growth per institution. We consider that the recent trends of decreasing net immigration and increasing supply of housing stock should also aid in slowing down the pricing growth. We note frequent market commentary predicting a slow-down in house price, which could also curb price growth. Finally, we believe that inflation-adjusted house prices in the states of Western Australia and Queensland are likely to continue the flat trend or show a mild decline in the next one year. We believe that the risk of a sharp, disorderly correction in house prices remains low because the stable economic outlook for Australia. If a sharp fall in house prices were to occur, in our opinion, it would likely be accompanied by broader macro-economic weakness across the country. In our view, this scenario could materialize due to the uncertainty in the international economic and a less upbeat economic outlook on Australia’s major trading partner, China. In our view, if China were to experience a hard landing–which we see as a low-probability outcome–there would be a meaningful negative impact on the Australian banking sector. This could increase the cost of credit for Australian banks, increase financial stress of borrowers, limit the ability of banks to pass on these costs to customers and, therefore, constrain earnings.

S&P sees good industry risk with ongoing low loan losses and external funding risk mitigated by strong government support:

Government role. In our opinion, the Australian government plays a strong role in supporting the funding needs of Australia’s banks, and has been responsive and flexible during times of stress. The government has an effective track record of providing guarantees for wholesale and retail funding throughout the global financial crisis. Additionally, the RBA also catered to the funding needs of the banks by modifying eligible collateral criteria. Further, the RBA has set up a committed liquidity facility (CLF) for the Australian banks which also supports the implementation of the Basel III liquidity reforms in Australia. As Liquidity Coverage Ratio (LCR) framework came into effect on Jan. 1, 2015, banks with larger and more complex with respect to liquidity risk are subject to LCR. Fourteen locally-incorporated ADIs requested for CLFs to meet their LCR requirements and APRA granted approval to all of them, with the aggregate amount of about A$275 billion accounting for nearly 6% of total banking system assets. This transition to the CLF has solidified our assessment of funding and liquidity as it has the effect of formalizing government liquidity arrangements for banks.

The two risks, then, are more tearaway house price growth or a Chinese hard landing:

In our baseline scenario, we expect Australia to rebalance economic growth toward the non-mining sectors, and continue to show GDP growth in the 2.5%-3% range in the near term, buoyed by reasonably solid consumption, elevated asset (housing) prices, and still strong real exports despite the falling price of iron ore. Investment growth remains subdued, reflecting the ongoing rebalancing away from the mining sector and the slowdown in Chinese growth. The continued depreciation of the exchange rate should facilitate this process. An alternative scenario for us is on the downside –namely if China was to experience a hard-landing scenario.

In a China hard-landing scenario, which we estimate to be a low probability, we estimate that China’s GDP growth slows down materially. Likely associated sharp falls in commodity prices and the Australian dollar could result in disorderly dislocations in the Australian economy. This could potentially cause a contraction in the Australia’s economy, which in turn could result in a material increase in the unemployment rate, and a material decline in residential property prices. Under this scenario, the systemic risks faced by banks in Australia would increase more significantly. Consequently, we would expect to see pressures on the economic risks faced by the banks operating in Australia, which would also significantly test capitalization levels. Consequently, in such a scenario, we expect to see at Australia least one-notch weaker stand-alone credit profiles for all financial institutions, and lower ratings on most of them.

Another alternative scenario, which could pose heighten systemic risks faced by the banks operating in Australia in our view is if –contrary to our base case expectations–the house prices in Australia continued to show strong growth. In our base case, we expect inflation-adjusted national average house price growth to slow down to about 4% in the next 12 months—broadly in line with the trend over the past three months.

We consider it highly unlikely that a scenario would emerge in the next two years that would materially lessen systemic risks faced by a bank in Australia. That said, should house price appreciation taper and there be no other new or emerging concerns impacting economic imbalances then this could alleviate economic risks, in our view.

It does not seem to occur to S&P that Australia is already in a “China hard landing scenario” even if China is not, as that nation rebalances its growth, destroying the income base of the Australian economy in the process:

If it ain’t cyclical then it ain’t visible. Structure just does not come into it, until it does.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

the global recession in 2009. We forecast that solid economic growth will continue over the short-to-medium term, even if slightly below trend given a muted recovery in non-mining business investment. We see potential risk of low interest rates contributing to higher house prices–as has occurred in recent years–adding vulnerability to the banking system although we believe that likely loan losses will remain very low by international standards. In our view, the economy is dependent on external savings to fund economic activity and growth Australia’s high current account deficits and external debt. We regard institutional and competitive environment for banks in Australia as low-risk. We believe the structure of the banking industry is supportive of industry stability–with a small number of strong retail and commercial banks dominating the industry. We believe that conservative and proactive regulatory and governance frameworks engender very low risk appetites and underpin banking system stability. Offsetting these positive elements, however, are the Australian banking system’s relatively low levels of customer deposits and its sizeable dependence on net external borrowings, despite some improvements in banks’ funding profile in recent years.

In our base case, we expect inflation-adjusted national average house price growth to slow down to about 4% in the next 12 months, broadly in line with the trend over the past three months. We consider that if–contrary to our base case expectations–the house prices in Australia continued to show strong growth, the banks operating in the country would face increased economic risks. Our base case expectations reflect the recent regulatory actions, including the increased capital requirements for the Australian major banks, clear direction to the banks to “appropriately” price for risk taken when underwriting investor mortgages, more stringent serviceability tests, and a soft 10% limit on investor mortgage growth per institution. We consider that the recent trends of decreasing net immigration and increasing supply of housing stock should also aid in slowing down the pricing growth. We note frequent market commentary predicting a slow-down in house price, which could also curb price growth. Finally, we believe that inflation-adjusted house prices in the states of Western Australia and Queensland are likely to continue the flat trend or show a mild decline in the next one year. We believe that the risk of a sharp, disorderly correction in house prices remains low because the stable economic outlook for Australia. If a sharp fall in house prices were to occur, in our opinion, it would likely be accompanied by broader macro-economic weakness across the country. In our view, this scenario could materialize due to the uncertainty in the international economic and a less upbeat economic outlook on Australia’s major trading partner, China. In our view, if China were to experience a hard landing–which we see as a low-probability outcome–there would be a meaningful negative impact on the Australian banking sector. This could increase the cost of credit for Australian banks, increase financial stress of borrowers, limit the ability of banks to pass on these costs to customers and, therefore, constrain earnings.