From Fitch:

Early Signs of Success for Regulatory Intervention in Australian Mortgages

Fitch Ratings believes Australian banks have tightened mortgage underwriting in 2015, largely due to regulatory intervention. However, risks have built within the mortgage portfolios over the past 24 months, leaving the portfolios more susceptible to a significant increase in unemployment or a sharp rise in interest rates – however, neither is our base case.

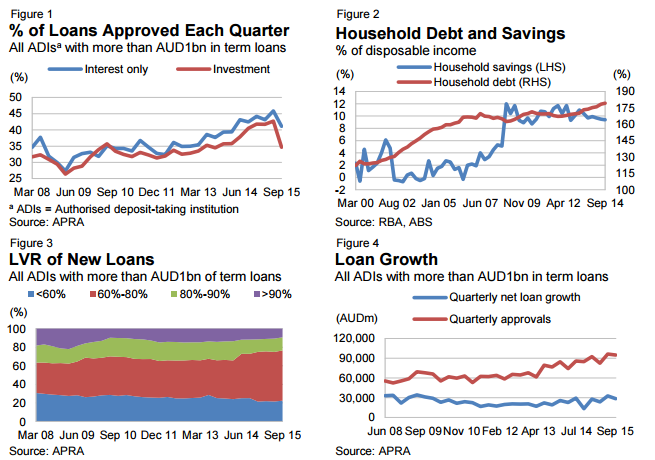

The regulatory focus has been on mortgages for investors and interest-only loans. Investor and interest-only mortgages both showed a sharp fall as a proportion of loans approved in the September 2015 quarter, as highlighted in Chart 1. Chart 3 shows a reduction in higher loanto-value ratio mortgages – a trend evident since 2014. Chart 4 shows that quarterly approvals continue to be well above net loan growth, implying borrowers continue to take advantage of low rates to pay down mortgages ahead of schedule.

The continued increase in household indebtedness, as shown in Chart 2, contributes to rising macroeconomic risks, and suggests households have used low interest rates to take on more debt. House-price growth in Sydney and Melbourne remains high, despite some early signs of moderation since mid-2015.

What to Watch

Owner-Occupied Loans: The regulatory limit of 10% growth for investor mortgages is likely to see banks refocus their competitive efforts into the owner-occupier space. This may lead to looser underwriting for this segment, although we expect the regulators to be proactive in addressing major increases in risk appetite.

Higher Capital Charges: Mortgage risk-weight changes from 1 July 2016 may have a modest impact on competitive behaviour, with pricing adjustments and less appetite for mortgages.

Mortgage Pricing: Higher funding costs, possibly the due to the expectation of higher US interest rates, may also lead to an increase in mortgage pricing. Recent interest-rate increases are a function of higher bank capital requirements and restrictions on investor loan growth.

Ratings Impact: Neutral

The tightened underwriting should ultimately be a positive for Australian bank asset quality. However, there is a risk of modestly higher mortgage arrears and losses in 2016 and 2017, as the loans that have been underwritten over the last 24 months season.

Should have been done in 2011. Rates and the dollar would fallen like a stone and now we’d be into a solid tradables recovery with a more steady and sustainable housing construction cycle. Instead, it’s been done far too late triggering a wild supply side boom and will now be pro-cyclical on the way down with the forthcoming residential construction rollover scheduled to converge with the LNG and car industry employment shocks next year.

APRA may have dragged the chain but it was Glenn Stevens that attacked MP all along.