From UBS:

US$ Earners – Reduced But Still Overweight

A key portfolio theme for us has been our overweight to stocks that benefit from a weaker Australian dollar. In Australia’s case these are mostly overseas domiciled translation exposures with the US$ the dominant (and our most preferred) exposure.

We concede that this is a popular trade among portfolio managers. However we continue to be positively exposed to the theme for a number of reasons: 1/ the logic of a lower A$ is still fairly compelling in our view, albeit becoming less so as the A$ heads toward fair value 2/ the trade offers an attractive risk/return skew as many high quality US$ stocks may perform well even if the A$ doesn’t fall but merely range-trades and 3/ we think valuations among these stocks on average still don’t look onerous.

The logic of a lower A$ is fairly compelling in our view. This is on the basis that purchasing power parity (PPP) is still below level the spot level of US$0.72 (being in the US$0.65c-70 range). Additionally, interest rate differentials should compress over the next one to two years as the Fed will likely do more than RBA. Indeed, we believe (cash) interest rate parity is not out of the question within two years which could see the A$ overshoot the UBS mid to high 60s fair value estimate.

Even if we are wrong in our view that the Australian dollar falls to cUS$0.68 (with downside risk), the US$ basket may still perform well under a scenario where the Australian dollar range-trades around the current 72c level. We believe this potential resilience is likely due to the quality (on average) of stocks in this foreign earners basket and their reasonably strong medium-term growth prospects. Only a clear uptrend in the A$ to would likely driven underperformance. This is unlikely in our view.

Valuations don’t look onerous. While the trade is a popular one we don’t find evidence of many stocks in this basket as being priced for a lower A$. Most stocks appear priced for a spot exchange rate. This seems consistent with the consistently positive reaction of the basket to a lower A$.

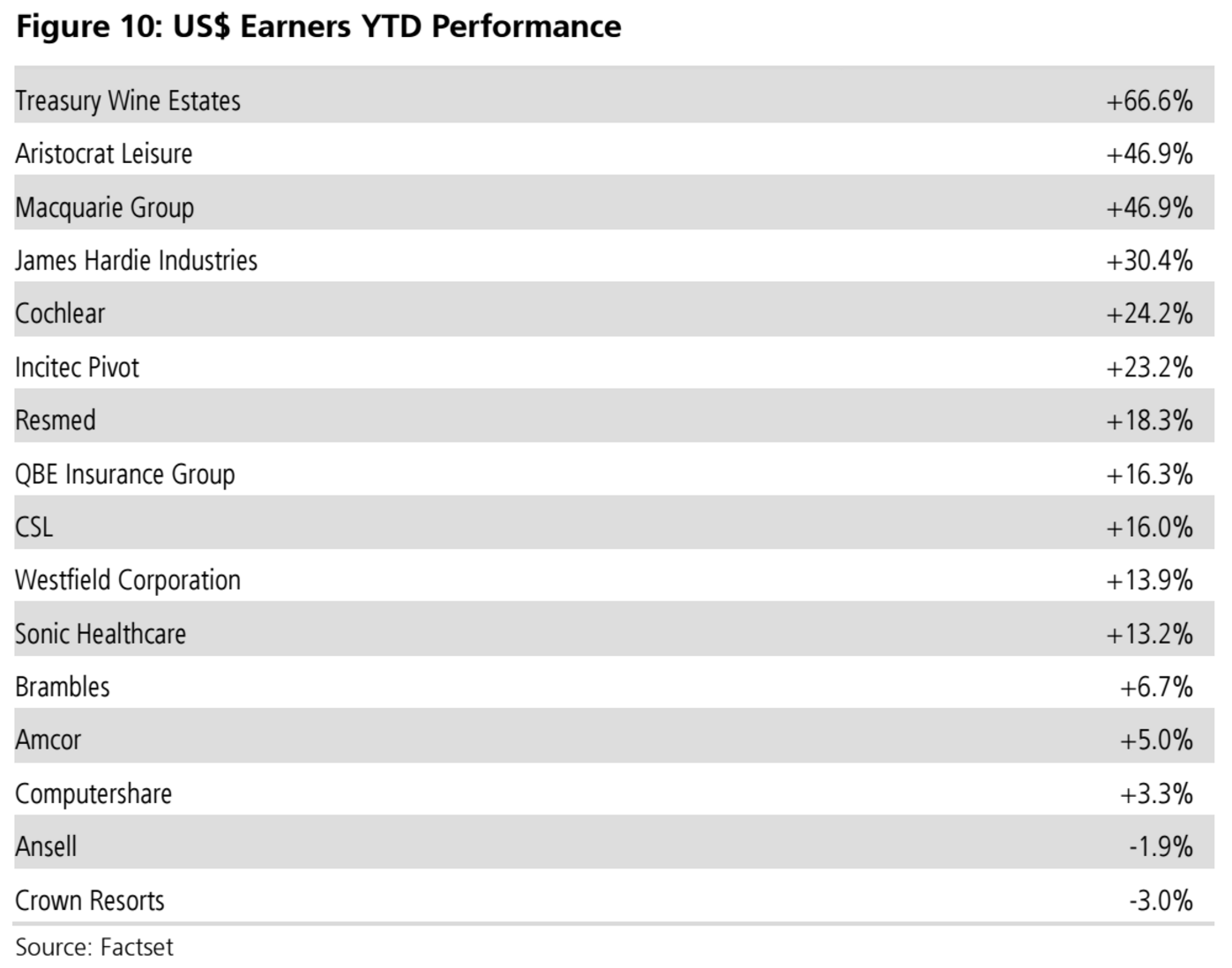

Based on our analysis of both exposure to the US$ earnings, stock fundamentals and valuation our most preferred stocks are CSL and Incitec Pivot. We also like Westfield Corporation, QBE Insurance Group and Macquarie Group.

Readers will recall that this has been MB’s pet equity allocation since early 2012. I am more bearish than anyone on the Australian dollar because few yet recognise how onerous will the be task of rebuilding Australian tradables after 20 years of economic mismanagement so reckon that these are also the stocks to carry for the next cycle. Having said that, I switched to selling the rallies in recent times in preparation for the inevitable general equity bust as the US tightens monetary policy.

Here is the UBS basket: