We update our Macquarie Mortgage Growth model and as a result we revise down our system housing credit growth expectations (6% in FY16 and 4% in FY17). This will be driven by a reduction in national house price growth from the quarter-ended Mar-16. This drives earnings downgrades of 1-4% from FY16-FY18, however we believe the recent sector sell-off has been overdone and that value has emerged as a result.

It appears we have reached the peak of the current housing cycle on a variety of metrics – Looking at a variety of indicators it does appear that the peak of the current housing cycle has been reached. Credit growth, auction clearance rates, house prices, settlement volumes and the $-value of settlements and are all showing signs of slowing, albeit from lofty levels.

Our economics team expect QoQ house prices to begin declining from Mar-16 with a 7.5% reduction for peak to trough – Reduced demand for housing growth from slowing population growth at a time when a housing supply surge is set to hit the market is likely to lead to a reduction in house prices. Our economics team are forecasting QoQ house prices to fall from the Mar-16 quarter before beginning to recover from Jun-17, with a 7.5% fall from peak to trough.

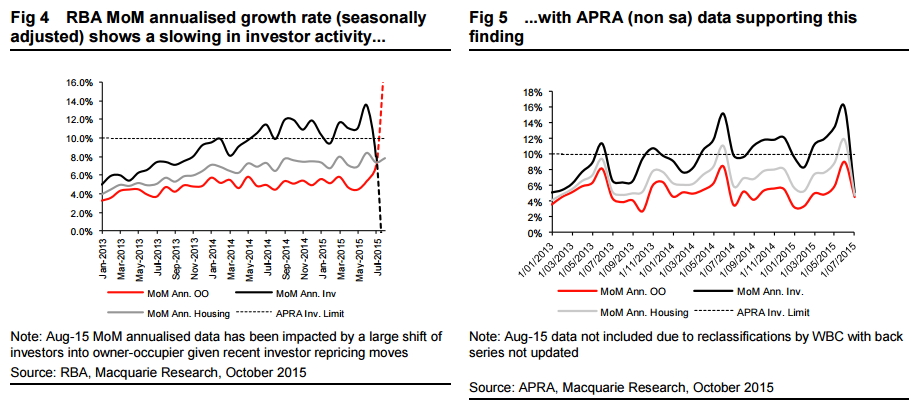

We expect the next housing credit down cycle to trough at ~3% YoY growth – Given the outlook for house prices we anticipate credit growth will begin to slow in FY16 to 6% YoY, with the rate of decline accelerating in FY17 to 4%. We expect we will see the bottom of the next housing credit cycle in FY18. Given each of the last three housing credit cycles have troughed lower than the previous cycle, we expect housing credit to bottom out at just above 3% in FY18.

Bank by Bank analysis WBC/ANZ least affected, with CBA is most – Based on our analysis WBC’s will be least affected (-1-2% p.a.) as they look set to grow above system in 1H16 from having quickly complied with APRA’s 10% investor cap. ANZ are assisted by their current strong momentum in owner-occupier lending although this is offset by their current level of investor growth, which is set to moderate (-1-2% p.a.). NAB take a hit (-1-3% p.a.) due to their highest investor loan starting point, based off APRA data. CBA is the most affected in our analysis given their larger mortgage portfolio and they had been gaining momentum in the capped investor space. (-1-4% p.a.).

According to Mac, one of the drivers of the correction is falling population growth:

We assess the outlook for Australia’s population growth, and implications for the economy, following the release of updated migration projections.

Weaker population growth will lower Australia’s potential growth rate, and also slow the transition from mining to non-mining growth activity. Slower demand growth, particularly for housing, increases the reliance on a weaker currency and lower rates to deliver a sufficient upswing in domestic demand.

The weaker population growth profile means some combination of a decline in house prices, a cut in interest rates; and a reduction in dwelling supply is likely to be needed to restore balance to the housing market. The adjustment is likely to keep rates lower for longer.

Australia’s population growth has slowed and is on track to slow further over the coming quarters. Population growth is still positive, but not as strong as it used to be, and not strong enough to justify the major surge in housing supply that will hit the market over the course of 2016.

Slower population growth adds to the adjustment challenge within the housing market over 2016 as the upswing in supply converges with the impacts of macro prudential policy tools and curbs on foreign investors.

Building approvals and housing commencements, at 200k+ are running well ahead of estimates underlying demand, which we peg at 170-180k once current, and prospective, population growth rates are incorporated.

We remain of the view that further monetary policy easing is likely from the RBA. Our base case is that this is delivered in November, alongside downgraded forecasts for growth and inflation. We have maintained the view for some time that the risks lie with additional easing in 2016.

That’s fair enough analysis in normal circumstances but when you add:

the terms of trade and capex cliffs;

the complete dependence upon residential construction as the offset;

the shuttering of the car industry, and

rising volatility from the emerging markets crisis

what you get with Macquarie Bank’s house price roll over is near instant recession as household consumption dries up, deep rate cuts follow and house prices fall more like 20%. I mean, consider, Macquarie is forecasting roughly the same magnitude of price falls experienced in 2010/11. Virtually the entire country was in shallow recession through that period to “make room” for the mining boom without inflation. This time that boom will be imploding.

If you add an external shock to that, all bets are off for the depth of house price falls.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

We update our Macquarie Mortgage Growth model and as a result we revise down our system housing credit growth expectations (6% in FY16 and 4% in FY17). This will be driven by a reduction in national house price growth from the quarter-ended Mar-16. This drives earnings downgrades of 1-4% from FY16-FY18, however we believe the recent sector sell-off has been overdone and that value has emerged as a result.

We assess the outlook for Australia’s population growth, and implications for the economy, following the release of updated migration projections.