This note takes a closer look at the state of play in Australian exports, investment and employment with a view to gauging the prospects for GDP growth. With hard commodities comprising around 40% of exports, investors’ preoccupation with the troubled mining sector is understandable. Momentum in non-mining activity, supported by a meaningfully weaker A$, is providing some compensation, but the risks to economic growth are nevertheless tilted to the downside.

The commodity supercycle is now in its final stage, marked by declining prices, rising output and shrinking investment. Australia’s large mining groups are exploiting their low cost base and high iron ore grade to ramp up supply and expand market share. At the same time, the non-mining sector has turned around, with manufacturing and service exports growing at their fastest pace since the crisis – a development that has attracted relatively little attention.

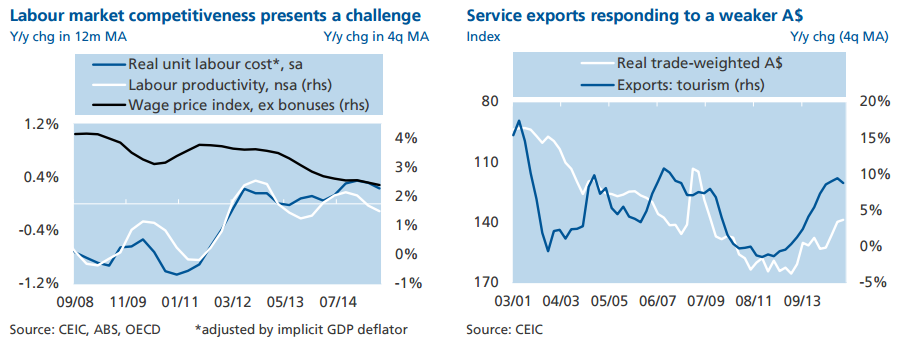

Services have already surpassed iron ore as a share of total exports, underpinned by solid growth in tourism and education – both particularly sensitive to currency dynamics. China’s nascent rebalancing is also altering the composition of demand for Australian exports away from natural resources; monthly tourist arrivals have doubled since 2011, while Chinese students now make up a quarter of the overseas total.

The investment picture is more sobering. Non-mining capex has gathered some steam, but this has not been enough to prevent a sustained contraction in overall business spending. Buoyant residential construction is a bright spot, but manufacturing capex is stagnating at recession-like levels. Importantly, the contrast between non-mining exports and investment sheds light on the RBA’s explicit emphasis on the exchange rate channel, as well as RBA Governor Stevens’ apparent reluctance to proceed with further rate cuts at this juncture.

Currency depreciation is having a quicker and stronger effect on real activity than falling interest rates are. Investment has been relatively unresponsive to successive policy rate reductions, and it should continue to be so for a while longer. If the latest official capex survey is anything to go by, mining disinvestment has a lot further to run, with virtually all spending undertaken in the boom years set to be fully unwound by end-2016. Moreover, record-low rates have created pockets of excess in the real estate market, although recent regulatory efforts are having some success in shifting the mix of (accelerating) housing credit growth away from investors to homeoccupiers.

Still, the RBA’s task is only going to get harder from here. Domestic and external macro headwinds are set to intensify, skewing the risks for real GDP growth to the downside. With household debt at over 1.8 times income and the savings ratio under pressure, consumer balance sheets are increasingly stretched. To be sure, unemployment has been surprisingly stable and job growth has steadily accelerated to a 2% annual rate. Strength in household service employment (a third of the total) is more than offsetting labour shedding in the mining sector, where wages remain comfortably above the national average.

However, mining-related compensation is only marginally dampening the downward pull on overall earnings rooted in the preponderance of part-time, low-paid job creation. And competitiveness remains under strain from sub-par productivity growth. As such, the labour market’s resilience masks weak fundamental trends, which are likely to weigh on domestic demand in future.

At the same time, China’s protracted slowdown renders a repeat of recent gains in commodity export volumes highly unlikely. Impetus has already started to flag; unless export prices pick up meaningfully, resource exports will no longer suffice to offset the hit to output from the contraction in mining investment. Also, the prospect of sustained CNY depreciation should make incremental A$ weakness harder to engineer, in view of the CNY’s 28% weight in the trade-weighted A$. And the bulk of the decline in metal prices may already be behind us, leaving less room for rhetoric about the need for exchange rate ‘adjustment’ to softer terms of trade. Finally, if the A$ overshoots to the downside, (currently welcome) import inflation may become too pronounced for the RBA to ignore, thereby limiting the room for reducing rates in the event of a shock.

Supported by a weaker currency, Australia’s non-mining sector has been taking up some of the slack left by the receding resource boom. But there is a good chance that the low-hanging fruit has been picked, skewing the near-term risks for GDP growth to the downside and complicating policymakers’ reaction function.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.