In our view, the worst thing about China’s slowdown is not the risk of some kind of cataclysmic economic meltdown or financial crisis but that – in sector after sector – the investable ways to “play” China shrink to the local names on the right side.

If you wanted to participate in Chinese wealth creation and rising consumer confidence during the stimulus years and before the start the anti-corruption campaign, the best choices (the then-tiny Brilliance notwithstanding) were foreign: European luxury goods and premium autos

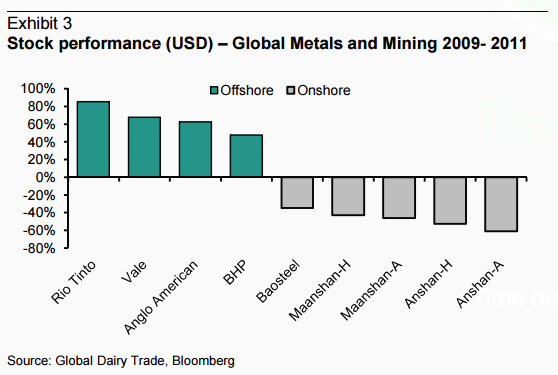

And it is over not just for coal, oil, iron ore but also for luxury, premium autos and fried chicken and possibly robotics and mass market autos too. That means that we return to the four requirements for emerging market investing. And at the same time as normal service resumes, China’s lack of local, investable companies and the appetite for intervention by the Chinese government is getting exposed.

Advertisement

The most corrosive aspect of the slowdown in the Chinese economy over the last three years is not that the level of debt within the Chinese economy and the risks associated with capital allocation and debt servicing. It is the simple fact that the old playbook – Australian iron ore, French leather, fried chicken and Bavarian engineering – doesn’t work anymore. The ability to pair Chinese demand with professional, shareholderfriendly, U.S. or European management is over….and arguably over forever.

The next chapter was therefore supposed to be A-shares:investing in Chinese companies benefiting from structural or cyclical shifts in China. Yes, China might be slowing. But remember: since GDP growth doesn’t matter for local market performance… who cares? The slowdown might be bad news for foreign plays on Chinese demand. But, again, the Chinese government would presumably be quite happy to see foreign companies now struggling to capture economic rents from China. That leaves Chinese companies in the “right” sectors in China as the obvious, best place to invest.

…The problem for investing in China is now two-fold… and those problems both relate to “transmission”. First, China has done a poor job over the last decade of developing companies with sustainable competitive advantages, attractive returns, good managers and strong stock performance. That can be fixed, and quickly… by the right companies and with the right incentives.

The second problem is much duller and may have a far longer shelf life. Christine Lagarde was right this week when – in addressing recent market interventions by the Chinese government – she described it as a “duty of central authorities” to address “disorderly functions” by markets. But the various and well-documented attempts to enforce stability in the Shanghai market over the last month (which are continuing this morning) go directly to old-fashioned “transmission” concerns. In other words, the old days are back. As a consequence, things are likely to remain cool in Shanghai, and for longer than just the summer.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

The most corrosive aspect of the slowdown in the Chinese economy over the last three years is not that the level of debt within the Chinese economy and the risks associated with capital allocation and debt servicing. It is the simple fact that the old playbook – Australian iron ore, French leather, fried chicken and Bavarian engineering – doesn’t work anymore. The ability to pair Chinese demand with professional, shareholderfriendly, U.S. or European management is over….and arguably over forever.