Yesterday’s awful capex report today sees more sell side rumblings of recession both in the short and medium terms. Morgan Stanley is not impressed with current data

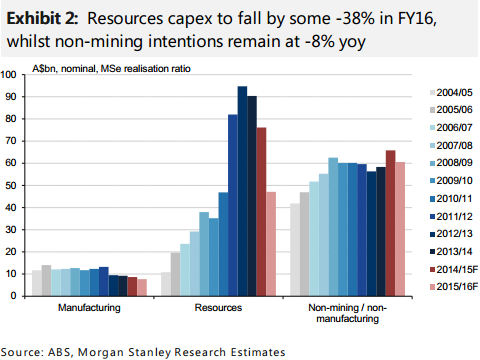

Quick Comment: Australian investment data was mixed in 2Q15, as the intense drag from the resources sector (-38% in FY16) is paired with as till patchy non-mining outlook (-8%).

…Heading for negative 2Q GDP? Our tracking estimate for 2Q GDP points to a decline of -0.1% qoq, with a negative surprise from machinery and equipment today,as well as dwellings investment yesterday, partly offset by some lumpy work in resources-engineering coming through (likely LNG related).While a weather-related drag of around -0.4ppt from net exports will be part of the story, we expect the weak profile of domestic demand will challenge the consensus view on Australia’s improving momentum.

And UBS was horrified at future data:

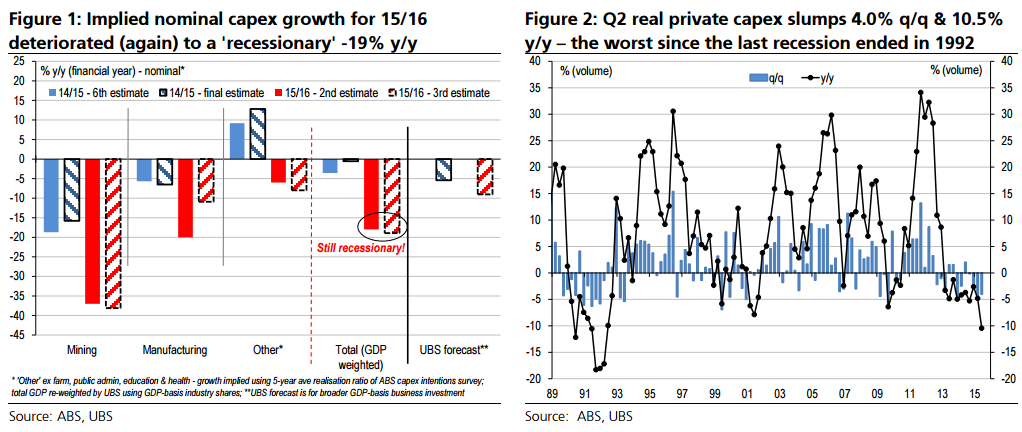

Outlook: 15/16 implied growth downgraded again to ‘recessionary’ -19% y/y Meanwhile, for nominal capex intentions, the 3rd estimate of 2015/16 was a bit better than expected at $114.8bn (UBS & mkt: $111.0bn), an upgrade of 10% from the 2nd estimate of $104.5bn. However despite this, based on historic ‘realisation ratios’ (5-year average, GDP re-weighted), nominal implied growth in 15/16 was still actually worse at a ‘recessionary’ -19% y/y (was -18% previously). This is because intentions by industry showed “other” deteriorated sharply. Mining remains in depression (-38%, was -37%), while manufacturing was less weak (-11%, was -20%); but the double-dip in the large “other” category got even worse (-8%, was -6%).

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.