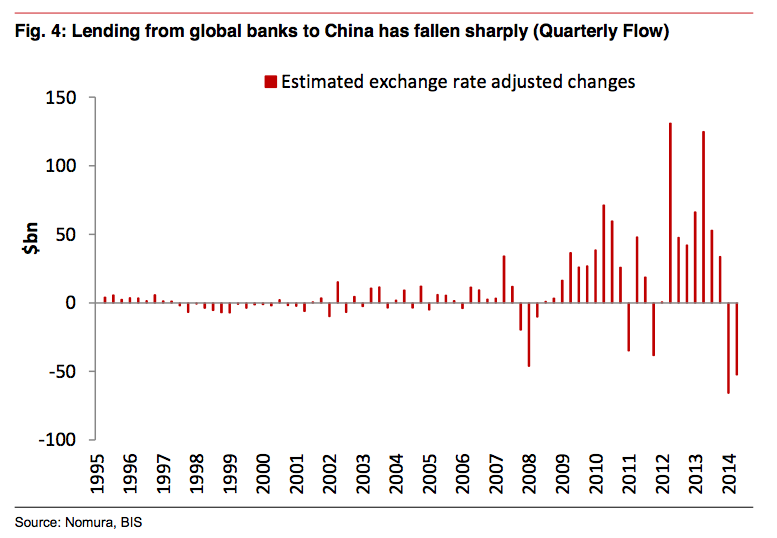

We think that the unwinding of earlier foreign exchange liabilities and “arbitrage inflows” by domestic entities have contributed significantly to the recent large outflows. In the few years before Q2 2014, especially during much of 2013 and early 2014, as the expectation of RMB appreciation had been strong and the onshore-offshore interest rate gap had been large (Figure 2&3). As a result, domestic entities accumulated foreign exchange liabilities rapidly, including through offshore borrowing. China’s short-term foreign debt rose significantly and foreign banks’ international claims to Chinese entities expanded by $440 billion between end 2012 and Q1 2014, according to data from the Bank of International Settlement (BIS) (Figure 4).

Since Q2 2014, following the PBC’s move to guide a modest weakening of the RMB, the market has expected a depreciation of the RMB instead. The weakening of Chinese economy and cuts in interest rates, and the strengthening of the USD along with QE tapering, have solidified expectations of further RMB depreciation. Such changes have prompted Chinese entities to reduce FX liabilities and accumulate FX assets.

If we assume a special ‘transfer effect’ of around $50bn and remove it from the data, the underlying intervention need in Q2 is cut in half, to around $50bn. This is closer to the PBOC’s reported FX sales, which total just $5bn during Q2. A lower magnitude of FX sales is more consistent with the magnitude of flows observed in the US Treasury market, which indicates around $20bn in sales, on our estimates (more on this below).

Conceptually, capital payments to AIIB and other regional development entities may also entail a drag on reserves in the future. However, from a short-term perspective, the amounts involved are not particularly significant. For example, the AIIB is meant to have a capital of $100bn, of which China’s share is roughly 30%. Moreover, only 20% of this is paid-in (while the rest is callable). In China’s case, this amounts to around $6bn of paid- in capital, and even this relatively small amount would only be paid in over several years. Hence, we do not view such transactions as material to the overall outlook for China- related capital flows and its reserves in particular.

Overall, the underlying trend in terms of intervention is weak, but the fast-paced reserve draw-down in Q2 may be an outlier.

One specific component within ‘other investments’ that has shifted very substantially is inflows from foreign banks. Foreign lending (likely in USD) used to average +$50bn per quarter but turned negative (around -$50bn) in Q4 2014 and Q1 2015. BIS data, which can be used to cross-check the Chinese BoP data, show a broadly similar pattern (we focus on the flows as reported by the FX-adjusted changes in locational exposures).

An analysis of the breakdown of bank flows indicates that banks in the United Kingdom and Taiwan account for a sizable portion of the swing, followed by banks in the United States and Japan (unfortunately, it is difficult to break out activity from Hong Kong) in the BIS data.

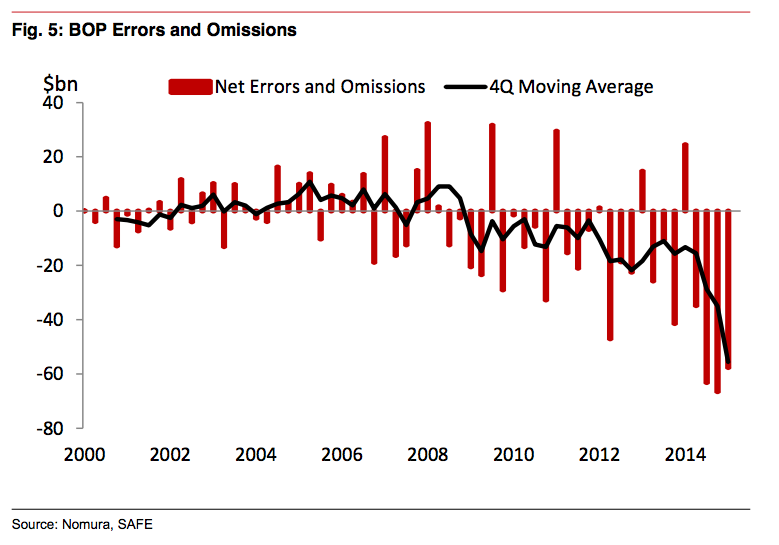

Away from the activities of foreign banks in China, there have been movements in recent quarters in the ‘errors and omission’ category within the balance of payments. By definition, this line item does not have a clear interpretation, as it is simply a residual. However, it is typical for the errors to increase in the face of unrecorded outflows; as such, it may reflect a degree of capital flight. The errors have been negative (i.e., suggesting unrecorded outflows) for some time, but they have become more negative in recent quarters. The increase in this component over the last year is in the region $30bn. Hence, it is a significant figure, but an order of magnitude smaller than the change in the bank-related inflows discussed above.

Whether the balance of payment data is a decent reflection of reality is a tricky question. For example, capital flight may be reflected in excessive invoicing of goods and services imports. But the trade surplus and the current account surplus are expanding, helped by rapidly falling commodity exports. Hence, the effect of any capital flight occurring within the current account is not sufficient to dominate other forces currently at play.

Overall, it seems that changing behavior of foreign banks is responsible for the main component of the shift in the overall flow picture. It is possible that this shift partly reflects a decline in demand for CNY carry trades. In any case, these flows could be important to monitor. Foreign banks have sizable exposures in China (currently around $800bn vs. $400bn in 2010). But at the current pace of reduction ($200bn annualized), the exposures will be materially reduced as soon as the end of this year. From this perspective, it is not obvious that further acceleration in outflows from this specific source is in store.

That said, sentiment in Chinese financial markets have clearly deteriorated markedly over the last four to six weeks (as evidenced by the collapse in the local stock markets). Hence, it is possible that capital flight may accelerate from here. But this would be a new dynamic, not something that we can directly observe quite yet. Hence, it is too early to say something precise about the magnitude of this effect.

There is one thing we can say about it that is certain and that is that capital flight is exacerbating the Chinese slowdown by keeping the real interest rate higher than it would be otherwise, just as capital inflows did the opposite on the way up. That may not overly perturb Chinese authorities given they’ve plenty of monetary ammunition in store but it’s not that easy. If they are forced to ease more quickly than they would like to stabilise property and the old economy then capital flight will almost certainly intensify and a nasty feedback loop forms.

At some point it could become necessary to choose between interest rates and the currency peg in a moment of crisis, not the way they would like it I’m sure.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.