Cross-posted from Investing in Chinese Stocks.

FT: Beijing capitulates after spending $200bn to prop up equities

Beijing’s leaders appear to have belatedly decided it is too expensive and ultimately futile to fight gravity in the equity market, especially as the government is now intervening separately on a massive scale to stop its currency from devaluing further.

Since the People’s Bank of China devalued its currency and introduced a new “market-oriented” foreign exchange price-setting mechanism on August 11, it has had to spend as much as $200bn of the country’s foreign exchange reserves to prevent the renminbi from falling more than it wants, according to people familiar with the central bank and its market interventions.

That was more money than the PBoC had spent over the past two years to keep its currency in the desired range against the dollar, these people said.

Last week in China May Only Have Enough Cash for 6 to 18 Month Defense of the Yuan, I looked at an estimate of liquid reserves from Charlene Chu of Autonomous Research. She estimated the country had $667 billion in liquid reserves, call it $700 billion. If China has already spent $200 billion yuan in the first two weeks of intervention, they could run out of liquid assets by the end of September or October.

WSJ: China to Flood Economy With Cash as Global Markets Lose Faith

The selloff in Chinese stocks accelerated Monday, adding pressure on Beijing, which is planning to flood its banking system with new liquidity to offset effects of its recent surprise currency devaluation, according to Chinese officials and advisers to the central bank.

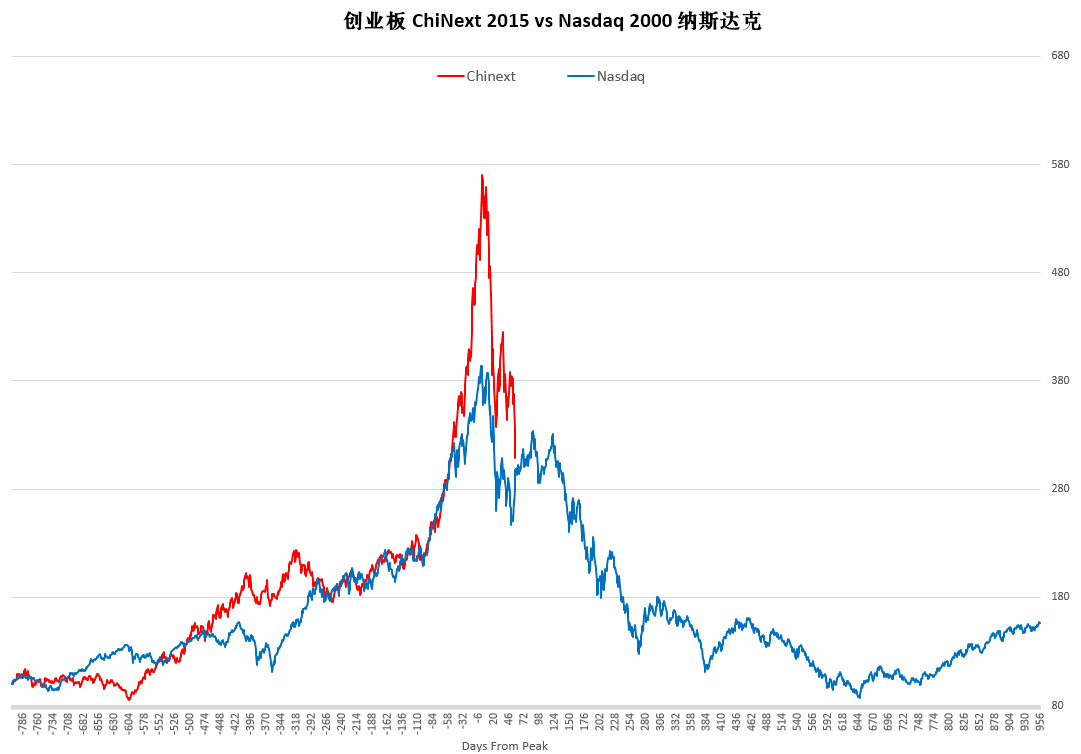

The Shanghai Composite Index dropped 8.5%, bringing its losses since its mid-June peak to roughly 38% and sparking another selloff in stocks and commodities around the globe.

The expected move to free up more funds for lending—by reducing the deposits banks must hold in reserve—is directly aimed at countering the effects of a weaker currency, which could send more funds away from Beijing’s shores. The moves reflect an economy increasingly failing to cooperate with Chinese leaders’ playbook to control the world’s No. 2 economy.

Flooding the banking system with liquidity lowers the value of the yuan, which leads to greater devaluation expectations, more outflows, need for more liquidity injections…

China must do a large one-off devaluation of the yuan or it will bleed its way to a currency collapse.