I’ve been quite enjoying the work of Capital Economics in recent times but they’re Aussie rep has lost it today:

…If the economy were to continue growing at a rate a little below its potential (which the RBA now estimates is between 2.75% and 3.00%) and the unemployment rate remained close to 6%, then we would agree that further rate cuts would be unlikely and that the next move would be up, albeit not for some time. There are four factors, however, that could yet make the RBA start to seriously consider cutting rates again.

The first would be evidence that mining investment is falling by more than the RBA is expecting or that non-mining investment is failing to rise as it is hoping. The release of June’s private new capital expenditure survey this Thursday (27th) will shed more light on this.

The second factor, which would be a sharper slowdown in economic growth than the RBA expects, won’t affect the RBA’s thinking until after next Tuesday’s policy meeting either, simply because the GDP data for the second quarter won’t be released until next Wednesday.

Third, it is possible that job growth will yet slow in response to the easing in GDP growth seen late last year and in the first half of this year. After all, since employment is a lagging indicator, it can take a few quarters to respond to changes in activity.

Finally, there is a chance that further volatility in global financial markets, either caused by concerns over the health of China’s economy or the Federal Reserve’s plans to raise interest rates, could influence the RBA’s economic forecasts.

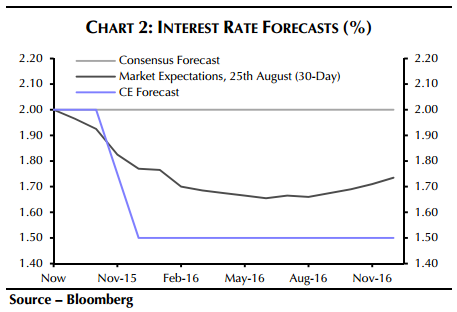

Well, that’s a bit of unfortunate arse-covering. CE does not appear to have changed its 1.5% outlook for the cash rate, which is too high, so why this shilly-shallying?

Today the RBA is more likely cut before year end than previous weeks so it’s poorly timed as well.

Advertisement

All of this meeting to meeting jibber jabber really is quite beside the point. Rates are going much lower. As low as they can go. Who cares when precisely?

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.