Chris Weston, Chief Market Strategist at IG Markets

With the September FOMC meeting now firmly in the market’s sights, there seems a newfound belief that the Fed’s mindset has shifted to one of ‘we are moving in September, give us a reason why we shouldn’t’.

Federal Reserve governor Jerome Powell took his turn to speak on policy overnight in what was a largely unscheduled speech and, despite sounding a touch more cautious, Dennis Lockhart kept the rate hike momentum going.

USD bulls were willing the US 2-year treasury on for a closing break of the year’s ceiling at 75 basis point, but yet again the buyers moved in. With the fed funds pricing in a 50% probability of a hike in September and the centrists on the board seemingly assisting this view, I would be a seller of two- and five-year bonds on rallies unless the US data really deteriorates. Perhaps the best way to express a view around the September meeting, though, is through 3-month Eurodollar futures (September contract).

Sell 3-month Eurodollar futures (September)

With the market priced so delicately, traders have what is almost a binary opportunity. Quite simply, if you feel they will start normalising policy in September, selling 3-month Eurodollar futures for a move lower would make sense, placing a stop above 99.67. This is my own preference.

This Friday’s payrolls will carry huge bearing for markets and, despite the poor ADP print in US trade, consensus still stands at 225,000 jobs to be created in the payrolls report. On the positive side, the employment sub-component of the services ISM printed a record level of expansion, so this has given hope that this Friday’s print will hold up OK. While the unemployment rate (expected at 5.3%) is critical, I feel the algo’s will be set to sell US bonds and buy USDs on a headline jobs print of 215,000 or more. A number above 250,000 and 3-month Eurodollar futures will get savaged.

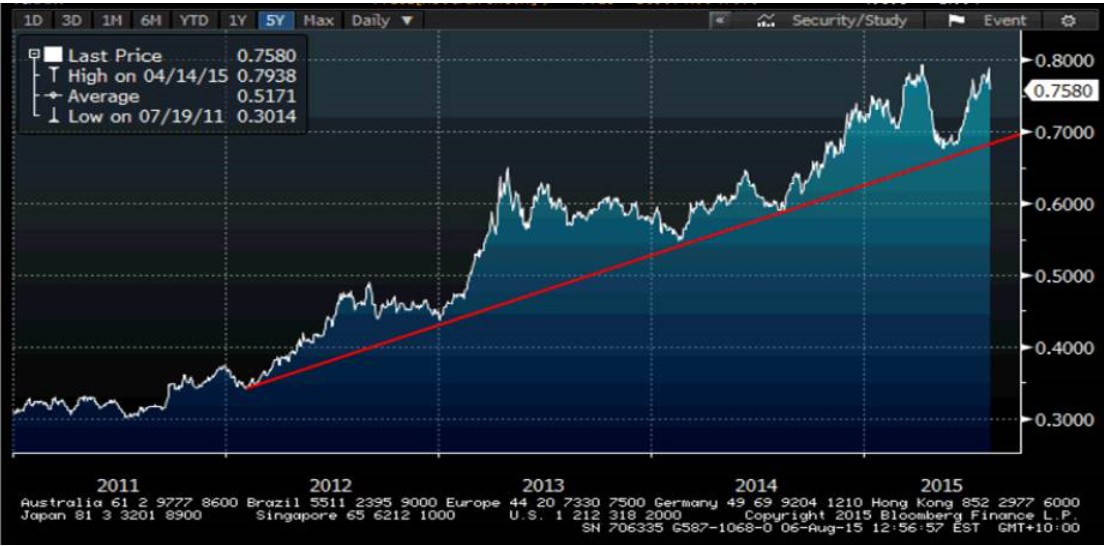

Jobs have been a key theme in Asian trade today with Australian July employment throwing the AUD around. An initial spike to $0.7393 (from $0.7356) was seen in AUD/USD after algo’s reacted to the strong 38,500 net jobs created. However, the move was short-lived as a sizeable jump in the participation rate caused unemployment to increase to 6.3%. This won’t enthuse the Reserve Bank, although all eyes fall on tomorrow’s Statement on Monetary Policy, where I would expect some trimming in growth expectations. Look for the bank’s December forecast of growth to be cut 25 basis points to 2.25%.

Interestingly, the bond market saw the numbers for what they were: finely balanced, containing both positive and negative factors. Yields immediately dropped and there was no initial buying, suggesting the bond market focused emphatically on the unemployment rate over anything else. The ASX 200 saw net selling as well, although there has been some support kicking in for material names.

Long materials, short banks

Like most in the market I have been sceptical of the resource sector and continue to feel this is a trading sector first and foremost. Still, it seems as though we are seeing switching out of banks and into mining names. Today’s announcement from ANZ has reignited the need for increased capital but the financial trading update was also 2% shy of expectations and there seems to be some concern about future profitability in the space. What’s more, if you look at the ASX financial / ASX material sector ratio, you can see remarkable outperformance since 2012 from financials with the ratio moving from 0.34x to where they currently stand at 0.75x. Momentum seems to be waning here and short-term momentum actually favours looking more closely at mining stocks.

(Bloomberg chart showing the ASX financial/ASX material sector ratio)

This is a call I loathe given the trends that are taking place in commodities, but there is absolutely scope for short-term outperformance from mining stocks. Of course, let’s see how Rio Tinto perform when they report just after the close (consensus: sales expectations $18.77b, EPS adj $1.27, net debt $14.58b). While Rio’s financials will always be in focus, traders will be keen to watch out for margins, capital management and of course the outlook, especially for China.

With Asian markets generally mixed, there is no real follow through or inspiration for our European opening calls. US futures are modestly lower, but our European calls are fairly downbeat at present. The focus is clearly on the UK and the Bank of England and, while we are starting to see buyers come in as we approach the open, there is no real discernible trend in cable. In fact, looking at a daily chart of GBP/USD you can see falling intra-day ranges. This makes a lot of sense given what we are seeing priced into the US and UK money market curves, but the trade seems to be standing aside and letting the market dictate. Buy a break of $1.57 or sell a break of $1.55.

Ahead of the European open we are calling the FTSE 6713 -39, DAX 11582 -54, CAC 5171 -25, IBEX 11236 -43 and MIB 23805 -106