Today Martin North produced another of his excellent proprietory household surveys:

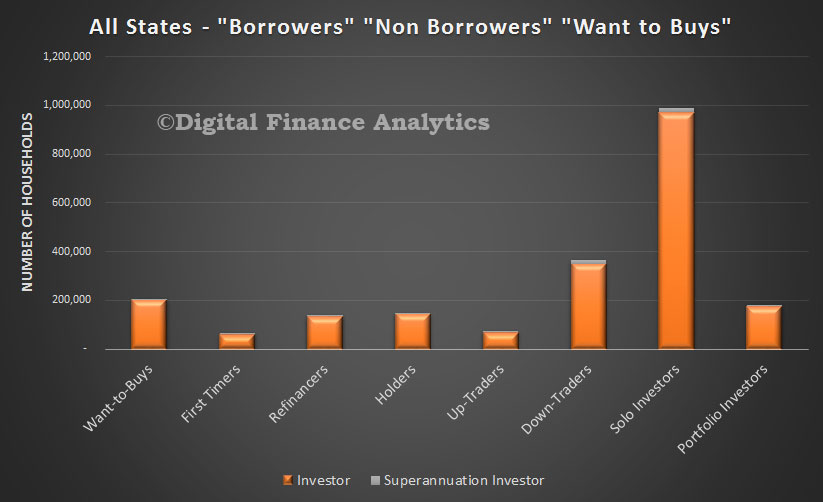

Continuing our analysis of the latest DFA household surveys, we look at the investor segment. You can find our segment definitions here. We start by estimating the number of investors in the market. Overall, there are 2.16m households with investment properties, up from 2.01m in 2014. The growth is explained by the entry of increasing numbers of first time buyers, and more down traders becoming active.

We also see the continued rise in the number of portfolio investors – households with a portfolio of investment properties, to nearly 200,000. A significant proportion will have more than five properties. Around 75% of portfolio investors expect to transact within the next 12 months, 49% of solo investors and 52% of down traders.

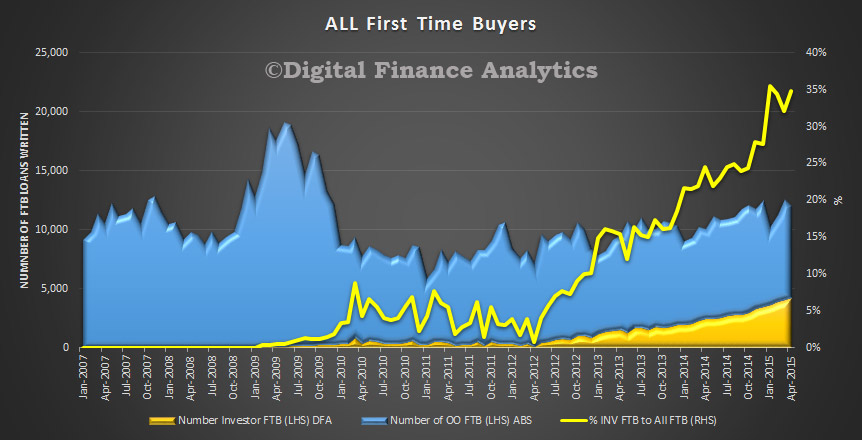

First time buyers are increasingly going direct to the investment sector, with more than 50% of first time buyers in Sydney following this path:

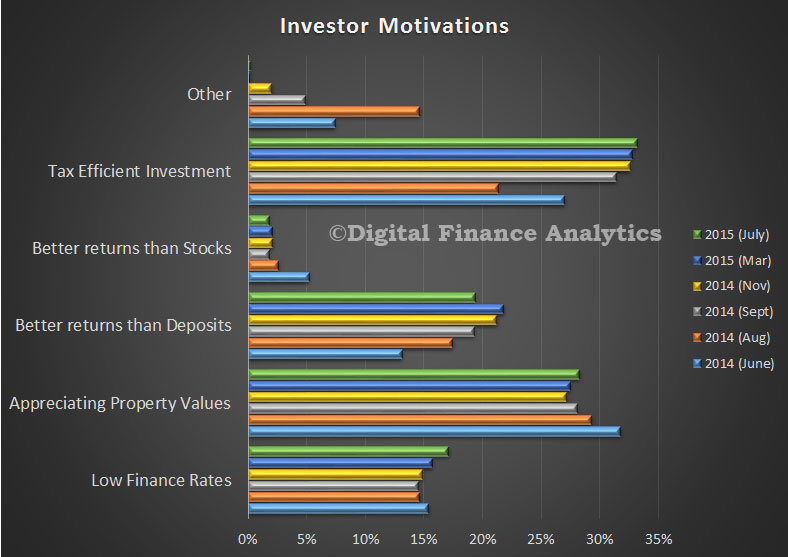

The latest motivation data suggests that appreciating property value, and tax effectiveness remain the main drivers to transact. They are also influenced by low finance rates, and the ability to get better returns than from deposits. A rising number of investors are now relying on rental income for future living expenses, this is especially true among down traders, who need higher returns than bank deposits:

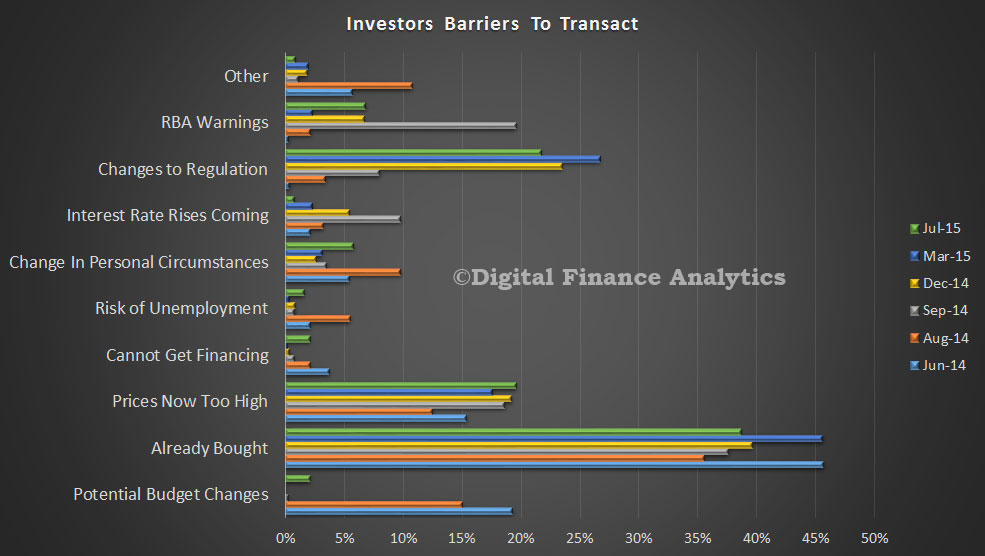

Some barriers to transact do exist, the main issues are that they have already bought, and are not considering another purchase (38%), that prices are getting too high (20%) and some concerns about the changing regulatory environment – leading to availability and price of finance (22%). But concerns about rising interest rates, budget changes and RBA warnings are relatively low. We did note a slight rise in those unable to get finance – the main reason was that the transaction LVR was too high to meet current underwriting rules:

Finally, we continue to see a rise in property purchased through superannuation. Tax efficiency and appreciating property values, backed by low finance rates are key. We think that about 5% of transactions are now within superannuation:

So it reconfirms that property is really just another investment asset class, and many are using the current gearing and capital gains tax breaks quite logically. As we have discussed before, this is distorting the overall marker, and excluding many potentially willing owner occupied purchasers from the market.

In short, greed continues to rule fear. Readers will know that my base case for property is that it will bust with the next global shock as the RBA runs out of interest rate cuts and fiscal stimulus is limited by sovereign downgrades.

But it is worth remembering how the 2003 Sydney boom came to grief given it is the closest historical analog that we have to the current boom. It, too, was period of international instability with worries in the Asian Financial Crisis and the Dot Bomb crash holding local interest rates very low. The point worth most recalling is that that boom was sailing along just fine until the RBA intervened with potent jawboning and two rate hikes. Just two was enough to bust Sydney.

Advertisement

The situation now is rather similar. Interest rates may be lower adding greater momentum but we do have strongly jawboning monetary authorities and we have just had out first mortgage rate hike for investors.

They may not be terribly concerned about it right now and can cite Chinese buyers or population growth and, if they have any brains, more cash rate cuts. The reduced sticker shock of mortgage rate hikes versus cash rate hikes (and cuts) may also be an important support.

But MP tightening and investor mortgage hikes will slow activity and as weakness in the West creeps East, a second rate jump owing to a little more macroprudential tightening may be enough to turn Sydney and Melbourne markets to fear and trigger a rerun of the 2003 bust, from the AFR:

Advertisement

…Depending on the bank, many investor borrowers are paying interest rates that are anywhere between 0.27 and 0.6 percentage points higher than those charged to owner-occupiers.

…Managing director of mortgage broker Homeloanexperts.com.au Otto Dargan said he expected further increases in banks’ interest rates for property investors.

This is because banks are trying to avoid being the cheapest lender for investor loans, which would risk leading to an influx of customers.

“The interest rates for most investor loans are likely to be 0.4 percentage points to 0.9 percentage higher than rates for owner occupied loans by the end of this year,” Mr Dargan said.

We could see some slack taken up by owner occupiers but they have not been the driver of the cycle and if investors get spooked then a key difference with 2003 may come to fore. This time there is no mining boom to save the wider economy and support a “soft landing”. Indeed it is the exact opposite.

Given the looming global shock of one kind or another over the next 18 months, I’m not sure why anyone would wait around in the property market to find out.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.