The triple-headed risk hydra that has been stalking global markets through 2015 today finds itself switching heads. The hydra is the global withdrawal of post-GFC stimulus in Europe, China and the US. For China, the attempt to manage its structural adjustment to slower growth via a stock market boom (and crash) has at least been stabilised, though the fallout will continue for months and years. In Europe, the threatened awakening from the delusional ideology of austerity as a path to economic restructuring has been reinforced, though the fallout will continue for months and years. Now we turn to the US, and its attempt to raise interest rates.

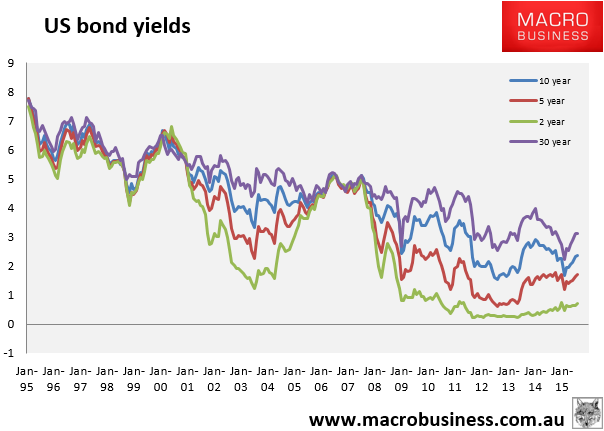

Markets are quite unclear about where the Fed is going. 80% of economists see a September rate hike. OIS markets put the odds at 40% and still favour an early 2016 lift. Bond yields at the short end of the curve have been rising in a steady uptrend for two years but longer dated bonds have continued to fall with inflation and falling commodity prices, most notably oil:

Thus the curve has barely steepened at all in the past two years, which is hardly encouraging for robust growth.

In wider markets gold is getting hammered and the US dollar flying again, which is hawkish, but these two can also be put down to the busted resolutions in China and especially Europe, raising the appeal of US dollars.

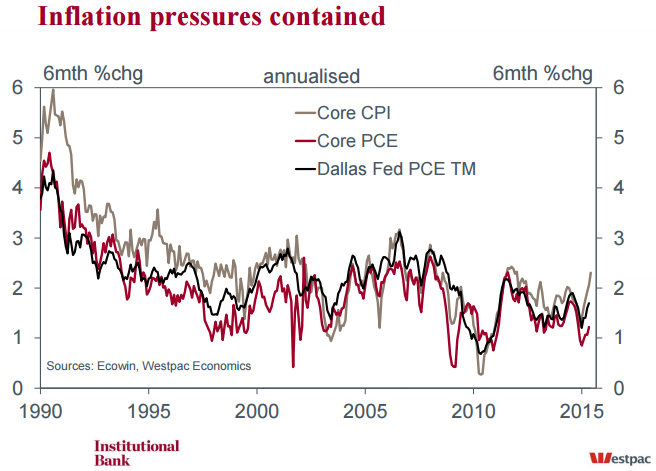

The heart of the matter is inflation or, more to the point, deflation, and too much of it. Following are some detailed charts from Westpac to give us some notion of the trends in US prices. First, Core PCE, the Fed’s preferred measure of inflation is very weak:

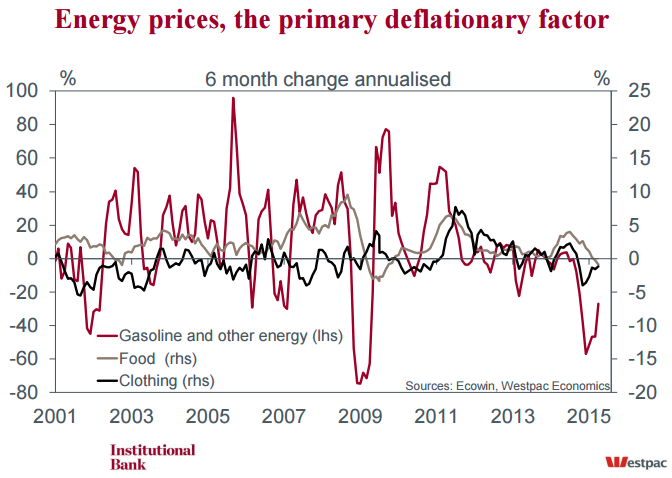

Energy and oil are the key soft spots:

The trend is up as early year falls pass ‘pig through the python’ style out of prices but energy is likely to weaken again in H2 in my view and wider commodities are also plumbing new lows across the complex. Broader inflation is also weak:

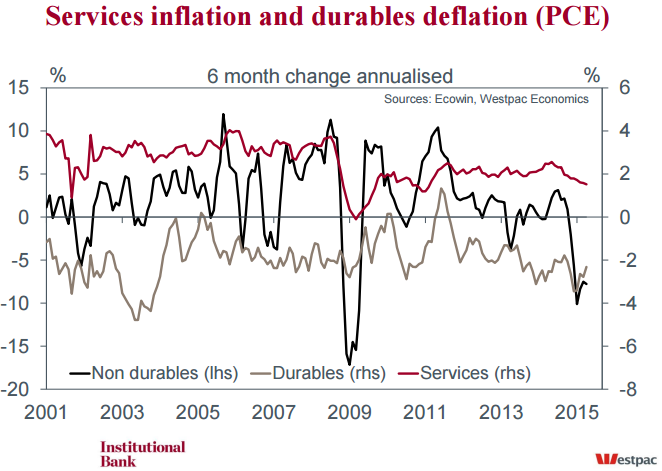

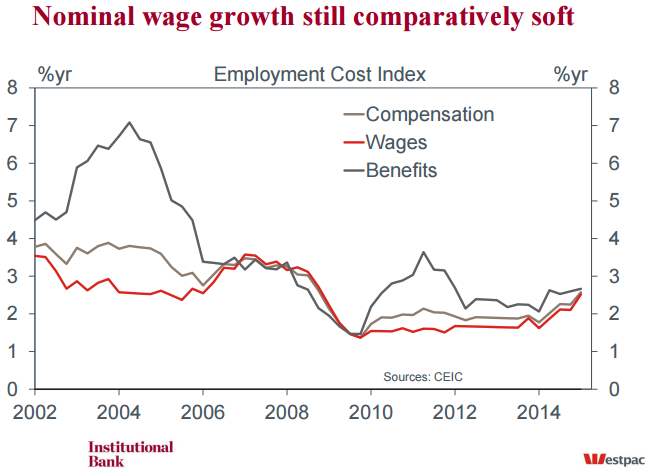

And there is evidence of only very early cyclical pressure on wages:

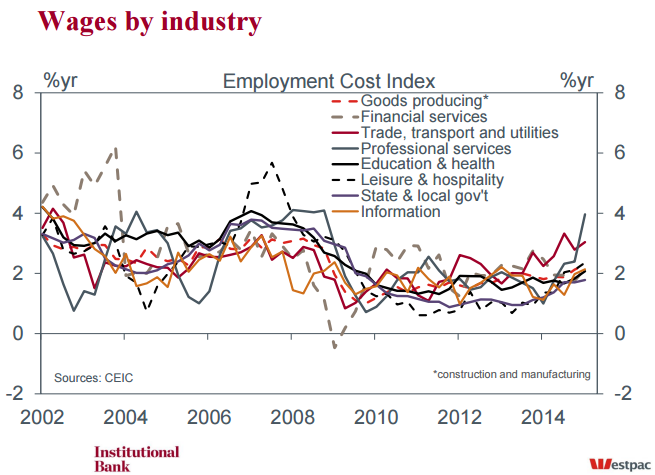

What pressure there is remains quite narrow:

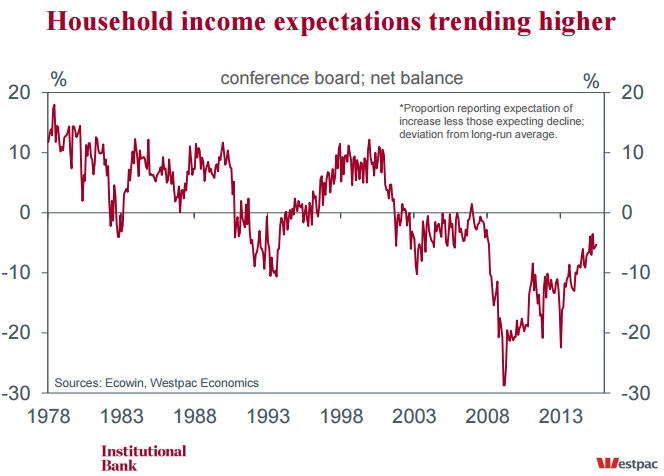

With expectations improving but still at recessionary levels:

In short, in its own terms, the Fed’s inflationary pressures are very weak and any pick up in household income is nascent to say the least. In my experience the Fed errs on the side of easy policy and, frankly, there is not enough momentum here yet to hike. If the improvement continues for the second half then early next year may be the time, but even then the outcome is unlikely to be positive.

Markets seem determined to price Fed rate hikes and provided wider global economy ructions are contained then eventually they will come. But, even in this best case, they are going to be shallow and slow as global markets dramatically amplify the impact through a withdrawal of US dollar liquidity and easing money everywhere else.

I still can’t see the Fed getting past three hikes, if that many, before crisis engulfs global growth and US stocks. The mistake of 1937 is still right frame of reference and Jeremy Grantham’s base case of a year end 2016 crash still looks good.

The good news for investors is that whatever the outcome – China and European stabilisation or not – US tightening risk does not change your allocations: short commodities, short Aussie, cash out of housing.