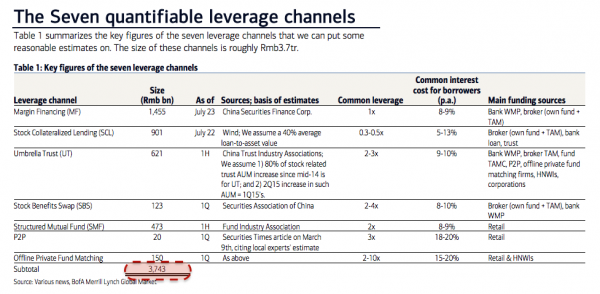

We estimate that margin outstanding, only from the seven channels that we can estimate reasonably, easily exceeds Rmb3.7tr. Assuming an average 1x leverage, it means that at least Rmb7.5tr market positions are being carried on margin, equivalent to some 13% of A-share’s market cap and 34% of its free float. Meanwhile, A-shares ex. banks are still trading at 36.6x 12M trailing PER. We believe that the government will struggle to hold up the market beyond a few months, unless it is prepared to let go some of its other policy objectives including RMB credibility. When the market ultimately settles at a level that can be sustained on fundamental reasons, we expect that the balance sheet of most financial institutions (FIs) may get impaired and the financial system may wobble, due to high contagion risk.

Leverage means relentless selling pressure.

The seven channels mentioned above are margin financing (MF), stock collateralized lending (SCL), umbrella trust (UT), stock benefits swap (SBS), structured mutual fund (SMF), P2P and offline private fund matching. There are a few other difficult–to-estimate channels, such as banks’ corporate/personal loans that ended up in stocks, brokers’ proprietary desk and funds’ subsidiaries. We suspect that the size of these may be Rmb1-2tr. In addition, China Securities Finance Corp. (CSFC) might have borrowed Rmb1.5tr from banks & PBoC to buy stocks. All the leveraged positions may want to unwind at certain point given the inflated collateral value, in our view. Additional selling pressure may come from hedge funds with compulsory winding-down clauses, when the market heads lower.

The risk is that the unwinding of the leverage will be disorderly – due to implicit guarantees behind most shadow banking financial products, investors could easily panic if they suffer from meaningful capital losses, by our assessment.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.