From The Australian today:

The Australian economy is now adjusting to the new normal of mid-tier commodity prices, record-low interest rates, a lower dollar and the shuffling of people and resources from one location to another, from industry to industry.

…Of course, there are serial gloomists; some high-profile media and financial market analysts have predicted 10 of the past three recessions….Sticking out his neck further, and more often, than most has been The Australian Financial Review’s Christopher Joye…Such heart-racing, high-sugar punditry is sadly the norm at the AFR.

The facts suggest other issues are at play. Inflation is under control. The spectre of a US-style home price collapse or Japanese long malaise are fanciful. The “bubble heads” ignore the economy’s supply responses, particularly the build-up of medium-density housing and the better use of suburban infrastructure.

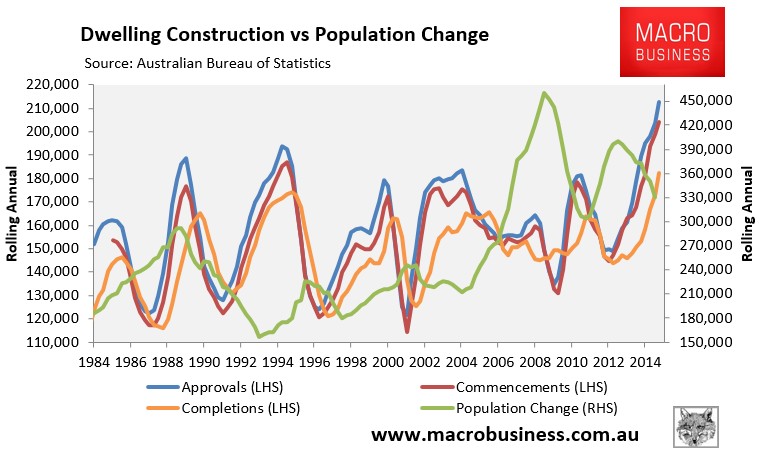

Just a quick point, the supply response is one reason why we can see this as a bubble in prices. Immigration growth is falling fast just as the supply response goes through the roof:

This is one reason why Goldman Sachs is now forecasting a housing glut in short order. Thus The Australian’s argument doesn’t even make sense in its own terms. Other reasons to see it as a bubble include the capex cliff, terms of trade shock, record high household leverage and record low affordability. It is the case that the bubble is providing some offset to the mining bust in the short term but that is only replacing one economic imbalance with another and it will also correct.

I’ll leave the last word to Mr Joye in this exclusive riposte:

“The Oz is suffering from relevance deprivation syndrome on housing matters having been so far behind the curve throughout this debate. I cannot recall how many articles they have written arguing I was wrong on housing over the last 12 months. It’s sad because our unfashionable forecasts for double-digit price growth and record increases in both the house-price-to-income ratio and household debt-to-income ratio since 2013, and the emergence of a disturbing asset price bubble that would force regulatory interventions, have proven spot-on: even the Treasury Secretary John Fraser says there is one. This critique also ironic because The Oz was fond of publishing my opinion pieces on the topic following my 2003 report to the Prime Minister on affordable housing strategies. I don’t think The Oz’s position is founded in logic—it seems to be more borne out of a desperate reflex to try and catch up to the AFR’s agenda-setting efforts to foster this debate. Macrobusiness’s Leith van Onselen and David Llewellyn-Smith have also done a tremendous job in this respect.”