So, finally, Chinese authorities have arrested the Shanghai bust by threatening to shoot anyone selling stocks. It is beyond the realms of experience to know what that means for market prices going forward. Will it go straight back up? Is it a bear market rally and the decline will resume in short order? If it were the West the answer would very obviously be the latter but if show trials for shorts begin who knows?

The median return of the China A-shares over 12 months to the market peak on 12 June is 200%. 185 companies are in the top 10 percentile; the median return is 410%. These companies declined by 57% from the peak on 12 June to 7 July. SHCOMP, SZCOMP and Chinext were down 28%, 38% and 40% during the same period…

As of 8 July 2015, 1,347 companies, or 40% of A-share free-float market cap, are not trading, up from 431 companies on 12 June 2015.

All A shares, excluding 764 suspended stocks, declined by 48% on average from the peak on 12 June to 7 July. Sector-wise, all sectors declined more than 40% from 12 June to 7 July. Telecom dropped the most at 52%, following by Materials (-50%), IT (-49%), and Industrials (-49%).

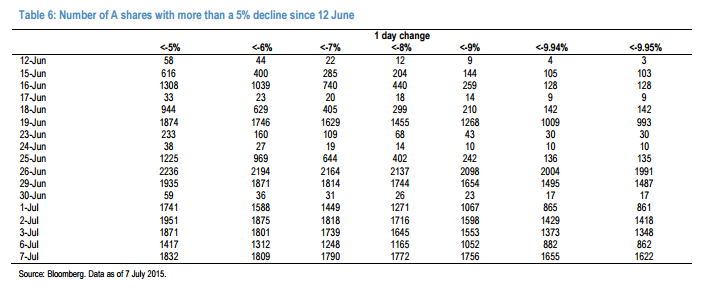

Over 1,000 companies have declined by more than 9% in eight trading days since 12 June. The normal daily price limit is 10% for A shares

And more jaw-dropping from JPM:

Advertisement

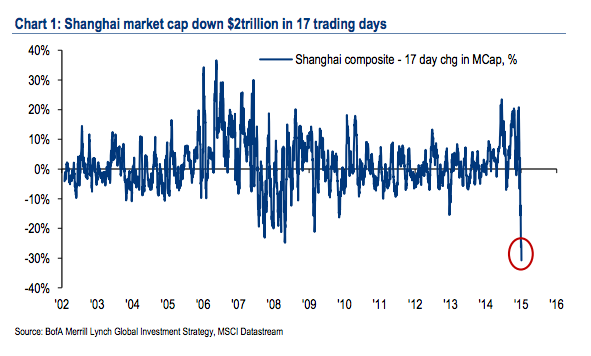

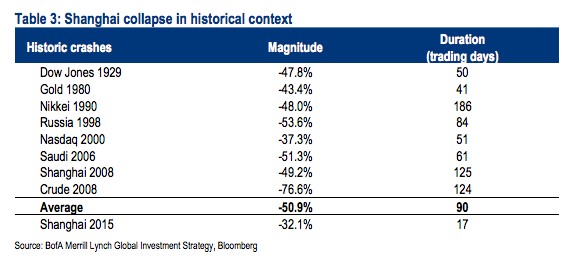

The market cap loss on the Shanghai composite has been staggering: $1.96tn since June 12th, a loss of value that exceeds the entire market cap of the combined UK, Swiss & Eurozone financial sectors, and a figure comparable to the GDP of India. The duration & magnitude of the initial drop from the high in 8 well-known bubbles has been on average 51% in 90 trading days (see Table 3). Thus far, Shanghai is down 32% in 17 trading days.

As for going forward, Credit Suisse thinks the risks are very high and thus it’s all good, also from FTAlpahville:

When a central bank says “whatever it takes”, we think the market should listen. The US Federal Reserve did so in 2008 and the European Central Bank did so in 2012. Is it the People’s Bank of China’s turn now?

The equity market panic has continued, with the Shanghai Composite Index diving by 32% over the past four weeks and share prices of smaller companies dropping even more. The authorities have launched two rounds of confidence-boosting measures over the past two weekends, neither meeting with much success.

The first round of confidence-boosting measures, anchored by cuts in interest rates and stamp duty, failed dramatically, as conventional policies had little impact in stopping the mechanical unwinding of leveraged positions. Over the past weekend, Beijing switched to administrative intervention by banning short selling and suspending IPO processes. State-controlled pension funds and sovereign funds are buying large caps, in an attempt to boost the index. More extraordinarily, the central bank injected liquidity in to the China Securities Finance Corporation Limited (CSFC) to buy stocks, without any pre-set limit in amount or timeline. Still, the measures did not seem enough to stop the market deleveraging and spiraling downward.

Why do we argue that systemic risks are approaching? Although hard data may not be apparent, anecdotally we note substantial leveraging up during the first five months this year, amid an extraordinarily steep rise in the stock markets. On top of the forced liquidation of umbrella trust funds, which has pushed the market toward a self fulfilling downward spiral, we now fear a chain reaction. Some companies and shareholders of companies mortgaged their shares to leverage up to invest in the stock market. Some homeowners mortgaged their house to invest in stocks. It looks like further forced selling is on the way. Worse, structured products were wide spreading, creating hidden risks that potentially could deliver unpleasant surprises.

…While quite concerned about the consumption channel, we are seriously worried about the financial channel for the following reasons: (1) The weakest links this time are brokerage accounts and funds which have thin balance sheets and weak public faith; (2) The leverage levels of some investors may be substantially higher than is currently understood publically, given widespread underground/over-the-counter activities; (3) Unchecked structured products could transmit risks quickly from one product to another and from one company to another; (4) The fall in the stock market makes it harder for the local government debt swap scheme; (5) The property market may be affected.

Besides the economic rationale behind making an outsized policy response, political considerations are equally important.China has one of the world’s highest retail investor participation rates in the equity market. With the drastic fall in share prices recently, we think social stability is clearly at stake. The market weakness also undermines President Xi Jinping’s reform plans and anti-corruption campaign. Premier Li Keqiang expressed his strong preference for having “one big shot” at stopping the panic after he returned from a European trip. The PBoC, the MoF and the SASAC, on 8 July, all demonstrated a strong political will to stabilize the capital markets. In our view, the political will to take outsized policy actions in Beijing today is stronger than that seen in Washington in early September 2008.

Nevertheless, the Chinese authorities are in unchartered waters. The market they are dealing with is very different from the one they faced several years ago. It probably will take some time to figure out the right mix of policy tools and more importantly to demonstrate policy determination. We are inclined to believe that Beijing will escalate policy responses until they start working. We have listed a few options that we believe Beijing may consider, but stress that unconventional measures probably would work better in current market conditions.

And Deutsche muses about the pros and cons of plunge protection from Zero Hedge:

Advertisement

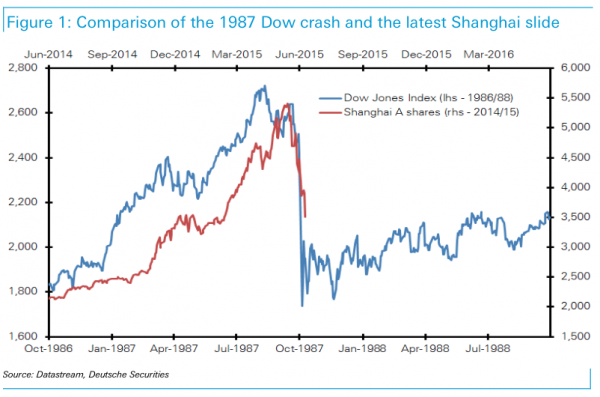

The ’87 US plunge protection team: sweet & sour lessons for China

Unlike 1987 when Greenspan was a one-man plunge protection team using rate cuts to support the market, China has fewer constraints to substantive direct price keeping operations, but there are strong arguments against actions going beyond smoothing activity.

The PBOC is struggling with ‘the holy trinity’ – maintaining a currency peg for stability, targeting interest rates and RRR directed at the real economy, providing equity support, and all this while attempting to liberalize interest rates and open the capital account. It’s a tall ask. Internationalization of the currency should be slowed.

The sweet

1) The slide in Chinese equities has some characteristics of the US 1987 crash in so much as ’the October crash’ in 1987 unwound relatively short-term gains mostly established in the prior 10 months. As per Figure 1, the one-year prelude to the 1987 US crash showed a similar pattern to China equity gains, albeit Figure 2 also shows how China’s equity appreciation was much larger than the US gains that immediately preceded the 1987 crash. The important point is the equity surge was relatively shortlived, so there never was quite enough time for a feedback loop to develop from higher asset prices driving a stronger real economy driving the asset bubble ever higher. The real economy implications are not as acute when a short-lived bubble pops.

2) Remember the mythical ‘plunge protection team’. The market has consistently spoken about how the 1987 crash prompted the creation of a ‘crisis group’ of senior US officials that would draw up lines of support for the equity market if faced with a similar collapse in equity prices. For better and worse, China is much more willing and has fewer constraints on official intervention, and the role of the PBOC funding China’s Securities Finance Corp as a source of support notably for a small cap stocks, at a minimum has the prospect of smoothing any price decline.

The sour

1) The flip side of any official equity intervention, and as important the recent suspension of trading in some shares, is the obvious lack of transparency. This has resulted in good stocks/assets being sold to hedge illiquid asset exposure that itself destroys confidence even as it creates good value for select equities. China has the resources to support the equity market in the shortterm, but there are inherent problems in artificially supporting prices. It undermines the markets confidence that a base has been reached, and in the long-term further distorts the allocation of capital. These are arguments why plunge protection should be no more than a smoothing facility to encourage fair price discovery.

2). The US substituted a late 1990s equity bubble with a housing bubble which did not end well. China’s experiment in substituting housing froth with equity froth, is plainly not succeeding. This all falls under the title: ‘troubles with policy traction’ that adds to China’s growth risks.

3). Collateral damage. The problems of credit creation dominated by bank lending is compounded by the sizable part of lending that is backed by property and a much smaller but substantial amount of collateral comprised of ‘movable’ assets like equities, commodities, and receivables. There is then more scope for contagion to work across asset classes and intercede directly into the banking system via the impact on collateral. This space needs to be watched closely.

4). ‘Proof’ that the PBOC is not omnipotent. Greenspan’s rate cuts immediately after the 1987 crash did seem to stabilize the situation. He was a one man plunge stabilization team, and this was in retrospect the early stages of the ‘Greenspan put’. Even this ‘put’ distortion was ultimately seen having huge costs. The PBOC is already much more stretched than the Fed ever was. They are struggling with ‘the holy trinity’ – maintaining a currency peg for stability, interest rates and RRR directed at the real economy, equity support, and all this while attempting to liberalize interest rates and open the capital account while maintaining fiscal discipline. It’s a tall ask. It would suggest that some objectives like the internationalization of the Rmb be deferred.

Summarising:

Shanghai is a bust. When a market is not allowed to fall at the point of a gun it is not a market. This hardly enhances China’s adjustment to more efficient uses of capital;

the communists will do whatever it takes to re-inflate it;

the downsides for the economy are all bad but less so than it appears.

The upshot for me is that China will slow more swiftly than it would have done. The bubble was largely a sideshow anyway in terms of the trajectory of growth. Whether it rises, falls or does nothing from here the faith in authorities will be shaken. Property will recover less even than was already the case, consumption be a little lower, banks will have to deal with an even larger pipeline of bad loans, public debt restructuring will take a bit longer and investment slide on.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.