Mr Ross Gittins continues the campaign for national ignorance today:

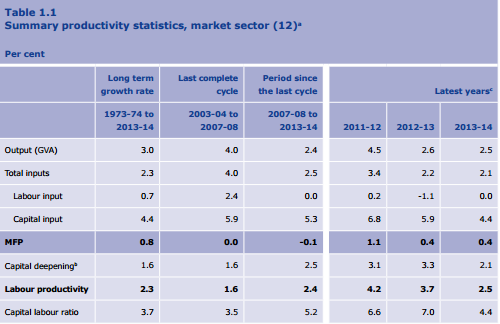

Rummaging through the media’s rubbish bins this week, I happened upon some good news. According to the Productivity Commission’s annual update, the productivity of labour improved by 1.4 per cent in 2013-14.

And get this: in the 12-industry “market sector” of the economy, it improved by 2.5 per cent in that year and by 3.7 per cent the year before.

To give you an idea, the 40-year average rate of market-sector productivity improvement is 2.3 per cent. So, despite all the worrying we’ve been doing in recent years about our poor productivity performance, it seems we’re now doing quite well.

In which case, how come no one wanted to tell us? I can think of three reasons. First is the media’s assumption that good news is of little interest to their customers.

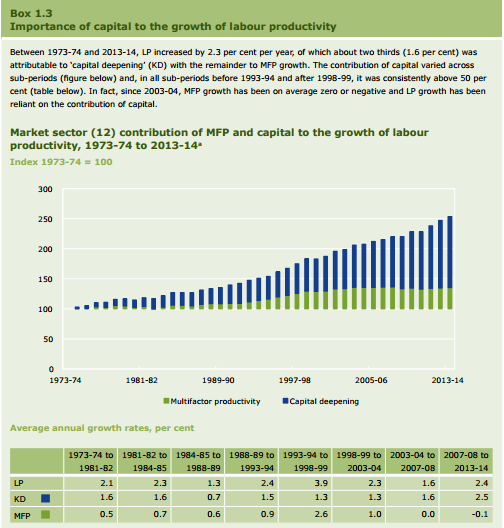

Second is that the Productivity Commission’s preference is for brushing aside the labour productivity figures and getting us to focus on the figures for “multi-factor productivity”, which show an improvement of just 0.4 per cent in 2013-14 and 0.4 per cent the year before. This compares with the 40-year average of 0.8 per cent a year.

Presumably that’s tongue-in-cheek given the reason that the Productivity Commission prefers MFP is because it is the only measure that matters. In terms of economic welfare, it doesn’t matter how good labour productivity is if capital productivity is terrible. You’ll be pushing around the income winners but there’ll be no net economic benefit.

We can, at least, be grateful to the Campaign for National Ignorance for bringing the release to light. It has not been well covered, I admit. But I put it to you that the reason for that is that the PC has not got its public relations act together and productivity of all kinds is basically a crashing boor for non egg-heads.

Anyways, here are the dismal results:

MFP at 0.4%, far below the historic average:

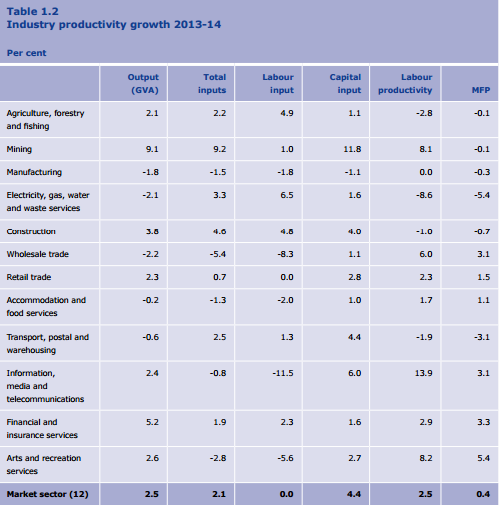

Here is the failure by sector:

And the reasons why are also pretty straight forward:

- massive over-investment in non-productive capital;

- inflated land prices, and

- over-consolidation in every sector destroying innovation and good management.

In short, poor economic structure.

There is still hope that the bad performance will turn around as mining gets more efficient and utilities move past their investment binge (though the greening of the network will inhibit that if not handled correctly). But so long as we rely on a population and housing ponzi to support fattened and rent-seeking services corporations to make up the heart of the economy, the outlook for MFP will remain poor. Obviously.

In fact, the Campaign for National Ignorance has himself recently argued this very point.