The transition in the economy from mining and energy led growth to nonmining growth drivers is proving more protracted than expected.

In our report last year Rebalancing 101: What Might The Economy Look Like we argued that rebalancing was achievable but would require further depreciation of the AUD. Consistent with this, the AUD has continued to decline and together with another round of monetary policy easing, economic growth has held up reasonably well and unemployment hasn’t risen significantly. But economic growth remains stuck below trend, inflation is close to the bottom of the target band and there is spare capacity in the labour market.

Domestic demand isn’t the only answer to filling the gap left by mining.

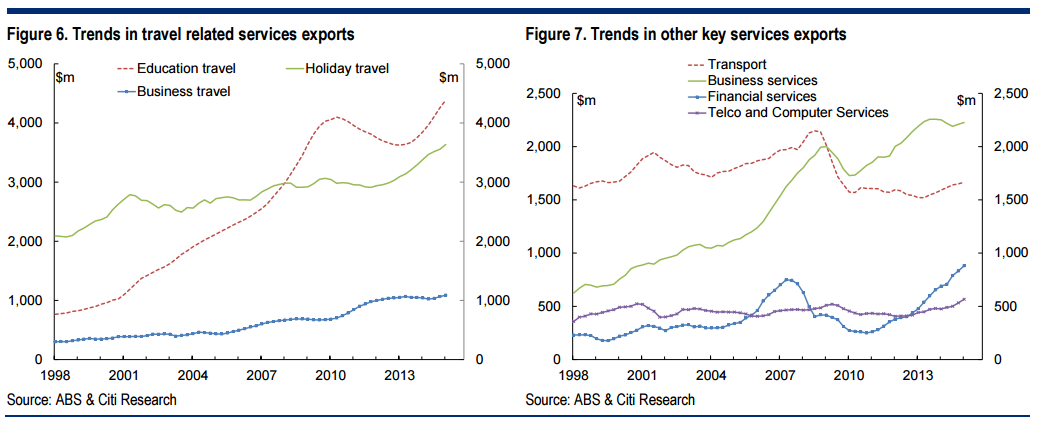

With China having now passed through the most commodity-intensive phase of its economic growth and the AUD adjusting to reflect this change, new export opportunities will be an important part of the rebalancing of the economy. Four services are in the top 15 export categories (Figure 1) and, as a group, exports of services are larger than agricultural and manufacturing exports (Figure 2). They account for 19.3% of all exports and 4.0% of GDP (Figure 3). Many services are delivered via joint ventures offshore and so aren’t included as exports.

There are already runs on the board.

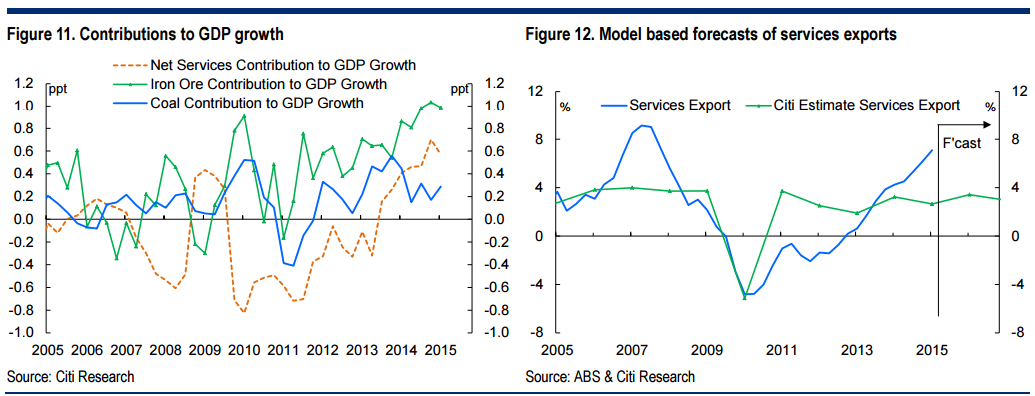

The rise in the AUD associated with the mining boom and weakening in demand during the global financial crisis squeezed services exports. The recovery in exports of services began during FY13 and has built strong momentum in tandem with the moderate recovery in global demand and the lower AUD. Services exports contributed 0.3ppt to GDP growth in the past 12 months compared to 1.0ppt for iron ore and 0.3ppt for coal (Figure 4).

The transition is a lot slower than expected because there is no transition. Tourism was always going to rebound. It’s the low hanging fruit of a falling currency. The problem is it will not be enough as mining export earnings crater and energy severely disappoints, and domestic demand folds as property slows, which authorities now want.

What Australia needs is a gigantic new strategy to boost exports and import competers of all kinds. It should have had a strategy during the mining boom to prevent hollowing out of non mining tradables. It should not have let the car industry fold on the verge of a currency collapse. We should have had a massive competitiveness push since 2011 when it became obvious that dirt was dusted.

All of these “services will save us” analyses are backward looking defenses of a busted economic structure that has resulted from ceaseless macro mistakes. Someone other than MB needs to start looking forward.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.