In a remarkable decoupling, the standard variable home loan rate for property investors is moving higher while expectations are for the cash rate to continue to fall.

…Even though the banks have for most of this calendar year been removing discounts on investor loans and tightening eligibility criteria, the pricing action last week surprised the market with its timing and magnitude. This is largely because banks have historically been constrained from adjusting variable mortgage rates outside the official cash rate moves made by the Reserve Bank of Australia.

Borrowers for houses should expect the hits to continue. CLSA analyst Brian Johnson says major banks could re-price up all housing loans – including owner occupied – by between 0.55 and 0.65 percentage points, an amount that would maintain group return on equity that otherwise would be lost from the Australian Prudential Regulation Authority’s decision last Monday to increase housing risk weights to a minimum 25 per cent from July next year.

There is nothing at all surprising here. It’s macroprudential in action, three year too late. Banking Day has more:

The banks are responding to a push by the Australian Prudential Regulation Authority to limit the growth in investor lending. They are also facing the introduction of higher capital costs in future.

Macquarie Securities said ANZ’s re-pricing would add 1.6 per cent to its earnings in 2015/16.

Macquarie said that if National Australia Bank and Westpac followed suit they would add 1.6 per cent and 3.1 per cent respectively to earnings.

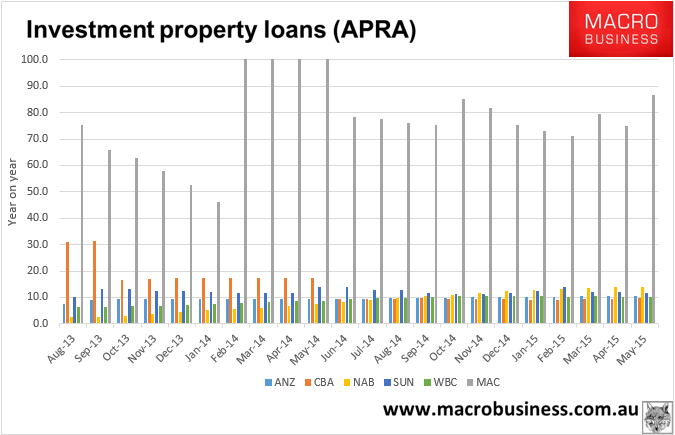

Westpac would get the biggest boost because it has the highest proportion of investor loans. Forty-six per cent of its mortgage book is investor lending, compared with 40 per cent for ANZ, 36 per cent for CBA and 29 per cent for NAB.

“While there may be some volume slowdown, that is the intention and all banks need to slow investor lending to ten per cent,” Macquarie said in a note to investors.

Macquarie predicted that a mortgage re-pricing cycle was about to get underway.

Fairfax Media reported that CUA and Heritage Bank have also raised their investor loan rates and that Macquarie Bank was contacting brokers on Friday to inform them that its investor loan rate would be going up.