From the FT:

Athens will be given a final chance to present a new reform plan to eurozone leaders on Tuesday night despite a hardening attitude to Greece in many capitals after the emphatic rejection of previous bailout terms in Sunday’s referendum.

But eurozone officials said leaders were unlikely to agree to restart rescue talks to keep Greece in the currency union at a hastily convened summit in Brussels, despite the Greek overture.

The European Central Bank tightened the screw on cash-starved Greek banks on Monday evening when it required them to stump up more assets in exchange for emergency loans. It did not reveal the scale of its adjustment to the collateral rules, but expects all four of Greece’s largest banks to retain access to the loans. It kept the cap on these loans at a total of €89bn.

How many last chances does that make?

Meanwhile, every man and his dog wants to call BTFD, from Business Spectator:

“Many would see this as a buying opportunity,” says BT Financial Group chief economist Chris Caton. “Greece will be an ongoing source of volatility but, given its economic size and the very limited exposure of the private sector to its debt, it’s very difficult to see the situation becoming calamitous.”

“It increasingly looks like Greece is the odd man out,” says AMP head of investment strategy Shane Oliver. While Portugal and Ireland and several other Eurozone countries have come through a mix of austerity and reforms without major political ructions, Greece is really a “special case,” he says.

Memo to Shane, Portugal and Ireland have done none of the restructuring that Greece has done and have been bailed out by the ECB. The AFR has more:

Perpetual global equities portfolio manager Garry Laurence said however that Greece itself, at only 2 per cent of Europrean GDP, was a very small part of the global economy.

“It’s just creating a lot of uncertainty and what you’re seeing is risk premiums starting to rise,” he said.

“The uncertainty in global markets is around what the ramifications are of Greece exiting and how much debt they actually owe, and who owns that debt, and what it all means.

“I wouldn’t be surprised if they do agree on something but if they really do default, its not so significant to global GDP growth,” Mr Laurence said.

Ausbil chief economist Jim Chronis said developments from Greece was not news to change asset markets or asset allocation.

“The thing that is new is that we know is the US is recovering quite well and rates will increase,” he said.

“You should be really focusing on the US and when they hike rates. It’s a question of will they do it.”

That’s depends upon what your allocations are. If you are long a falling Australian dollar, commodity prices and weakening domestic demand then you’re allocations are right.

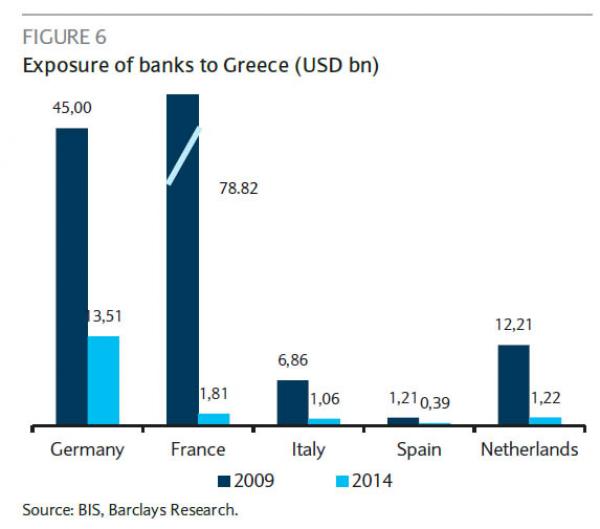

Whether it is has a wider impact will depend upon how the probable default plays out. The amounts are huge and will cause peripheral interest rates to rise. Private banks have been well prepared in direct terms, from Barclays:

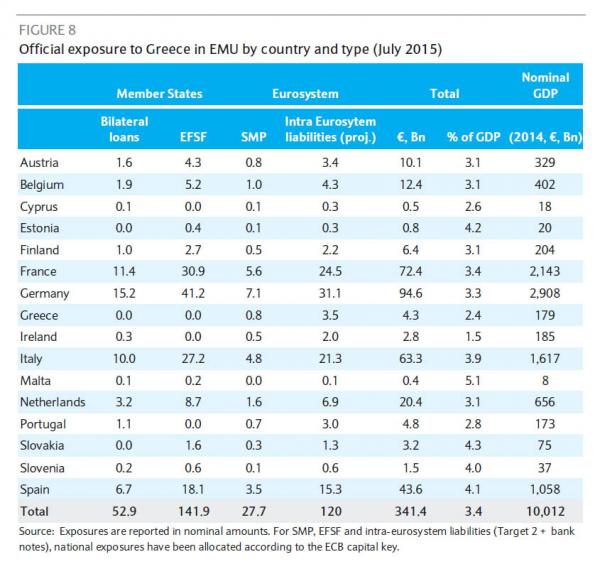

But that’s only direct exposure. The public liabilities are huge:

Nearly all of the Eurozone’s many fiscal firewalls and special funds are just shells. They have no money in reality but will need it if Greece defaults:

The backstops are not entirely infallible

Some of the backstops, if needed, are either untested or incomplete. One example might be the new banking union. At present, the €55bn resolution fund is still 95% unfunded, deposit guarantee schemes are still mostly ex-post funded and there is still no pan-European deposit insurance. More importantly, holdings of peripheral debt on domestic bank balance sheets are rising substantially in recent years. In Italy and Spain, for instance, domestic government bonds as a percent of total bank assets have risen from 1.5% and 2.3% respectively in 2009, to 6.5% and 7.8% at end 2014 and February 2015 respectively. Any period of prolonged, significant peripheral stress would almost surely lead to some, perhaps significant, widening in bank credit spreads.

As for the ECB’s OMT programme, it has never been tested and it is not quite the pure “lender of last resort” backstop many in the market have come to believe it to be. To start, ECB OMT purchases come with significant conditionality. Any country seeking this assistance must apply for a programme, which would almost surely come with fiscal and structural reform prescriptions.

Greek exit and an official sector default would be new precedents

The biggest risk for contagion, in our view, is that the Greek “no” vote would most likely set in motion two precedents – an exit and default of official sector debt – that have never really been stress tested in the euro zone, either technically, or perhaps more importantly, politically.

Greek default would have a non-negligible effect on EA balance sheets…

As we have said in the past, a default on official sector debt would be large, but technically manageable, at about EUR195bn in bilateral loans and EFSF/ESM loans. In addition, SMP bonds held by the ECB amount to EUR27.7bn and Intra Eurosystem liabilities (mainly Target 2) amount to EUR118bn. Altogether, the official exposure to Greece amounts to about EUR340bn, nearly 3.5% of EA’s GDP, sizeable but probably manageable

… while a default opens up a host of political risks that remain unanswered

A default on the European loans could create considerable political backlash in EA countries against further support for periphery economies. Right-wing parties, such as AfD in Germany, Front National in France, Party of Freedom in the Netherlands, and True Finns in Finland, have repeatedly opposed bail-outs to periphery countries, especially to Greece. But even more moderate parties may question the bail-out mechanisms as the Greek default of 2012 was meant to be a one-off. Smaller countries are also unlikely to take it lightly as; as a percentage of their country GDPs, these countries would bear a larger share of the burden (eg, the Baltic countries).

If Greece exits and defaults big there will be fiscal chaos in Europe. The ECB can contain some of it (so long as it is bailed out!) but you just don’t where the next mole will pop up.

What we do know is one of the two biggest currencies in the world suddenly has a large fissure running right through the middle of its institutional structure and nobody knows how it will be closed. Treating that as simple BTFD is BFS.