This mania for margin trading—which allows individual investors to borrow from the broker to up the amount of their stock bets, magnifying the size of gains and losses—is a new thing. Back in 2007, Chinese stock regulators forbid leverage. But as part of an effort to open up financial markets, they’ve softened restrictions of late. In October, nearly 5 million retail investors had margin accounts, up from less than a million two years prior.

The China Securities Regulatory Commission said on Friday it had banned Citic Securities, Haitong Securities and Guotai Junan Securities, the largest brokerages by assets, from opening new margin trading accounts for three months, following investigations into high-risk margin trading.

China’s securities regulator is tightening control over lending to small stock investors in an attempt to cool an overheated stock market. The China Securities Regulatory Commission (CSRC) has banned a type of margin-trading business called an umbrella trust, tightened control over other financing and told brokerages to limit potential risks, the commission said in a statement on Friday.

The CSRC has also allowed fund managers to lend shares to short sellers, according to the statement.

The major reason for the sharp pullback was due to a large Chinese brokerage (Guo Sheng Securities) cutting off margin financing for retail investors who want to trade in ChiNext stocks.

The ChiNext index, which comprises mainly small-cap companies who are typically seeing high growth and high valuations, has seen an incredible rally of over 160% on the year.

This could explain the move to restrict margin financing by the broker to limit risks in the event of a market collapse.

China Securities Regulatory Commission moved late on Wednesday to relax collateral rules on margin loans. But that failed to staunch market losses on Thursday, with the Shanghai Composite Index closing down 3.5 per cent and the Shenzhen stock exchange finishing the day down 5.6 per cent.

In the latest effort to cope with the worst domestic stock market crisis in years, China’s market regulator said on Sunday that it would allow the country’s central bank to provide liquidity support to the government-backed margin financeagency, China Securities Finance Corp.

The China Securities Regulatory Commission said in a statement on its website that with the support of the People’s Bank of China, China Securities Finance could expand its business and continue to help the government to stabilise the stock market.

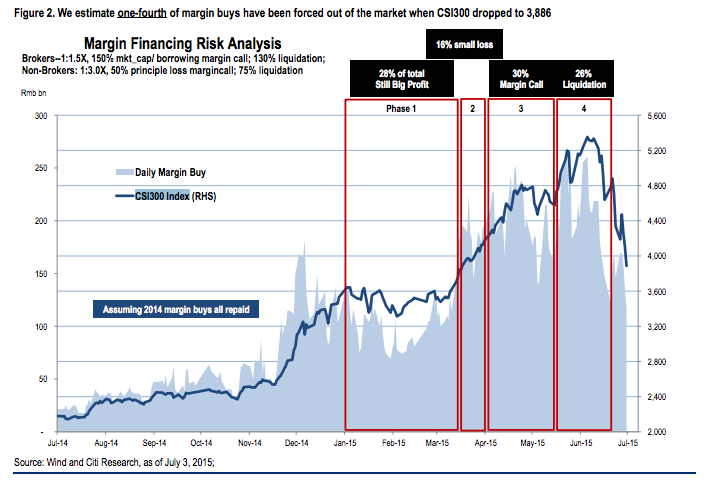

Despite the sentiment help, we believe continued deleverage, and possible reform concerns given recent administrative intervention, will cap index upside. Our calculation suggests only one-fourth margin buys have been forced out so far.

Advertisement

But, judging from today’s action, keeping this contained from here will likely take more firepower than has already been used. Firepower that will really put paid to that “decisive factor” stuff and potentially restart the problem.

And the fallout from JCap’s Anne Stevenson-Yang:

It is worth pausing for a moment to think how unprecedented this event is, not only the setting of a specific goal for the major index of the so-called capital “market,” but trumpeting it far and wide. The July 4 English edition of the People’s Daily simply wrote: “The brokers will not sell the stocks they held on July 3 and buy more in a proper time so long as the benchmark Shanghai Composite Index is below 4,500 points.” Analysts who compare China’s current rescue efforts to TARP need to note that TARP rescued operating companies, not a stock index and focused on the viability of operating companies, not the optics that a speculative derivative of the economy represented.

…And if the plan succeeds, it will likely succeed for the blue chips that are explicitly targeted, while the midand small-caps go into free-fall. But it is the small caps that have been falling the most and triggering margin calls, and it is also the small caps in which the retail speculator plays. That means that even a successful stabilization plan will likely leave the average investor with deep losses. Yet it is precisely the average investor’s cash that is needed; regulators can generally access the cash flows of SOEs and sovereign funds by fiat, but they need to induce retail to fork over cash, to bring in resources from outside the circle of State-owned capital.

In May, A-share insiders sold a combined 1.68 billion shares, up by a factor of three from the previous month. That figure does not include RMB 3.5 bln in bank shares sold by Central Huijin. State actors have already tucked away capital gains; now their goal is to strategically spend a small portion of those gains in order to induce the retail investor to come back to the market, because without the retail market, the equation does not work. The goal, after all, is to capture household savings.

…[But, anyway, China’s plan to hold up the market] seems unlikely to do more than introduce volatility intraday. The dramatic fall in Shanghai, in fact, looks like the start of a genuine financial crisis.

For one thing, leverage in China is always higher than it initially appears; it is just too easy to get credit from the banks. Although brokers we interviewed said they think that only 5-10% of the retail market has borrowed money off market to fund brokerage accounts, the exchange likely includes a range of capital that is technically spoken for and must be repaid. Executives are trading working capital “borrowed” from their companies, and this has to be paid back by a certain audit date. There may be commodities, such as copper, sitting in the FTZs as collateral. Borrowings from high-interest lenders on the gray market have gone into the market and, anecdotally, these loans are going belly-up very rapidly. On-line wealth management products have to preserve the liquidity and redeemability that set them apart from brick-and-mortar competitors. Companies that take advantage of short, high-return investment opportunities with operating cash floats, from taxi hailing services to e-commerce retail escrow holders, must be watching nervously. As the market positions unwind, we will see a surprising number of forced sales, followed by real economy defaults, policy changes, and guarantee breaches.

I still see the Shanghai bubble and bust as largely marginal but as a figment of the ongoing hard landing it isn’t and the mad scramble to save it by Chinese authorities kind of resembles the growing panic that seized US authorities as they at first underestimated the subprime bust, then fought it with conventional tools, and were ultimately seized by outright panic.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.