The talk among traders once again has been around moves in commodities and what that is saying about global growth.

Doctor Copper is painting a fairly bleak picture, with LME copper and aluminium trading to, or near the lowest levels since 2009 today and CME copper futures trading to a new contract low today. Brent and WTI oil are looking vulnerable, although we have seen some buying around the 7 July lows of $55.10 in Brent today. Iron ore futures (I’ve looked at the more liquid January contract) isn’t showing the same sort of stress and seems to be consolidating after 25% plunge from 10 June into July, although the longer-term trend is down.

Gold also joined in printing a new low of $1,077, although there has been some buying coming into the metal.

The issue of falling commodities has replaced Greece and Chinese equity volatility as the centrepiece of the capital markets. This seems to be premised on a toxic mix of increasing future surplus figures (in the forecasts), but Chinese growth and concern of a September move from the Federal Reserve are also in play. I am personally sceptical as to whether we will start seeing downgrades to global growth forecasts of 3.5%. However, there are signs inflation expectations are starting to move lower.

Of course, today’s Caixin flash China manufacturing will only add to the concerns and what a speculator miss, relative to forecasts, it was! AUD/USD fell an initial lazy 50 pips on the print but as the day wore on, the AUD has been savaged and if your preference is to follow a good old fashion trend, GBP/AUD is what dreams are made of. Headlines that ratings agency S&P could lower Australia’s sovereign credit rating if the budget doesn’t improve are also helping the bears’ cause, although it shouldnt really surprise as the market is on alert for the rating to be put on ‘negative outlook’ anyhow. Still, the mix of poor Chinese data, weak commodity prices and the prospect of an AA rating seems like the perfect storm for AUD deprecation.

Aussie Banks saw selling pressure on the S&P warning and this seems fair as a move to AA- could see cost of term wholesale funding rates rise as much as 15 basis points. This at a time when banks are looking to raise capital in-line with the new APRA rules.

Resource stocks didn’t really need the manufacturing data to see headwinds. However, prior to the data drop buyers had started making their way into Aussie material names. Clearly the data took some of the wind out of the buyer’s sails.

Commentary from the Caterpillar CEO Doug Oberhelman has also been widely talked about on trading floors and weighing up the commentary it’s hardly inspiring stuff. With end markets showing signs of slowing and the order backlog at the lowest levels since 2009, you can see why the stock was sold off by just over 3%. However, the comments about ‘stagnant’ global growth have caught the attention of the market and is aligned with emerging concerns about global growth.

There are signs that global equities could struggle from here but as always, its worth looking at the bond and credit markets as a guide for other asset classes. Generally, as a rule equities will follow credit markets.

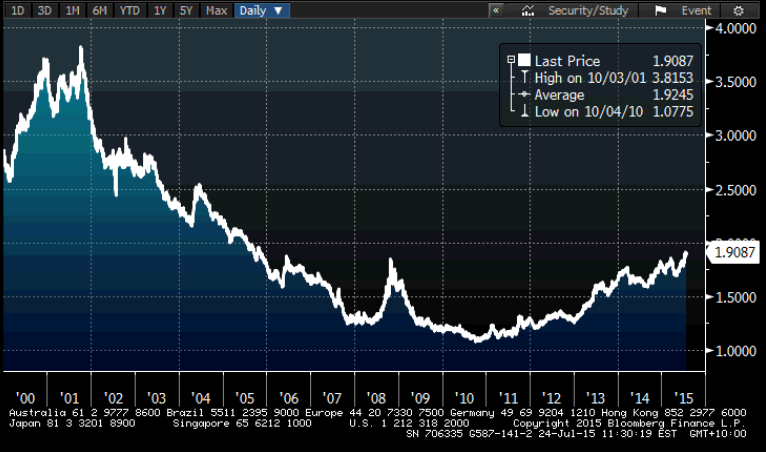

In terms of the impact on five-year inflation expectations the bond market (I’ve looked at ‘breakeven’ rates) has clearly reacted, with the market dropping 27 basis points to 1.47% since 18 June. We’ve also seen a reaction in the US yield curve (one of the most reliable measures around the perception of growth) which has dropped 21 basis points to 157 basis points. This is certainly a move thematic of growth concerns, but we are not at levels that should cause significant selling of equity positions.

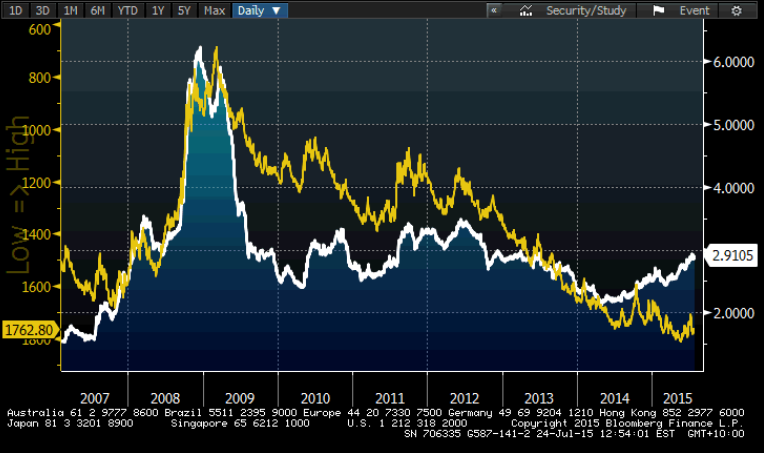

We have seen some signs of stress in US corporate credit-default swap space, specifically looking at the more leveraged junk space, but again there are no real signs of stress. What is interesting though is the spread between credit (I’ve looked at the Moody’s Baa Corporate bond yield) over the US ten-year treasury has increased from 2.12% in 2014 to currently stand at 2.91%. A break of 3% in the spread would suggest increased worries and could start to really be noticed by traders as during other years there has been an inverse directional correlation between this spread and the MSCI World index.

Emerging markets have also been underperforming, although this is not new. If we look at the ratio of the MSCI World to the MSCI Emerging market index, we can see this has increased from 1.07x to 1.90x since 2010 and is at the highest level since 2005. This shows a huge underperformance from developed markets and this should continue to be the case over the coming six months.

So, all-in-all, most of the news flow across Asia has been negative today and focused on China and global growth prospects. Commodities are absolutely under pressure, but if we look at the a number of the key forward looking indicators that suggest a sell-off across all sectors and a rush into safe-havens they are not flashing red yet.